Back to basics: The process of exiting a private equity investment

Share this article

The process of exiting a private equity investment can involve some important tax issues that should be addressed as early as possible.

Key Points

What is the issue?

The process of exit positioning – readying an investment for exit while balancing competing exit strategies – is a critical stage in a private equity investment’s life cycle.

What does it mean to me?

Whilst investment cycles can vary, a fund may start to consider an exit around the third or fourth year of holding an investment. This could involve an outright exit, an initial public offering or a dividend recapitalisation.

What can I take away?

Investors in private equity funds are encouraged to consider the potential implications of exiting their investments well ahead in the fund investment cycle.

This article discusses certain tax considerations arising at the exit stage of an investment undertaken by a private equity fund on behalf of their investors. The process of exit positioning – readying an investment for exit while balancing competing exit strategies – is a critical stage in a private equity investment’s life cycle.

The final stage of an investment cycle may present limited options in planning the most efficient tax outcome on exit by the fund. It is imperative that the tax implications of exit are considered as early as practicable in the investment cycle.

This article assumes a basic understanding of UK corporation tax principles, and is based on a pattern where the investment and investor are based in the same jurisdiction; i.e. in the UK.

Overview of a typical private equity acquisition investment

In a typical private equity investment scenario, investors may be investing through funds that are treated as transparent for tax purposes (e.g. in the UK, this could be an English limited partnership). In this case, the fund would act ultimately as a conduit (and where required, as the withholding agent) when exit occurs for the tax cost of the divestment for its various investors (the limited partners).

However, in jurisdictions where funds are or may elect to be treated as opaque, the tax cost of the divestment would be realised within the fund itself. For example, a US limited liability company may be treated as opaque for UK investors, whereas US investors in the same vehicle may treat the same company as transparent (unless a US ‘check-the-box’ election is made in the alternative). (It is noted that this classification for tax purposes is not definitive. In Anson v HMRC, the Supreme Court considered evidence regarding Delaware law in terms of which members in an LLC automatically became entitled to their share of the profits allocated to them, rather than receiving a transfer of profits previously vested in the company.)

The discussion below proceeds on the basis of a transparent fund.

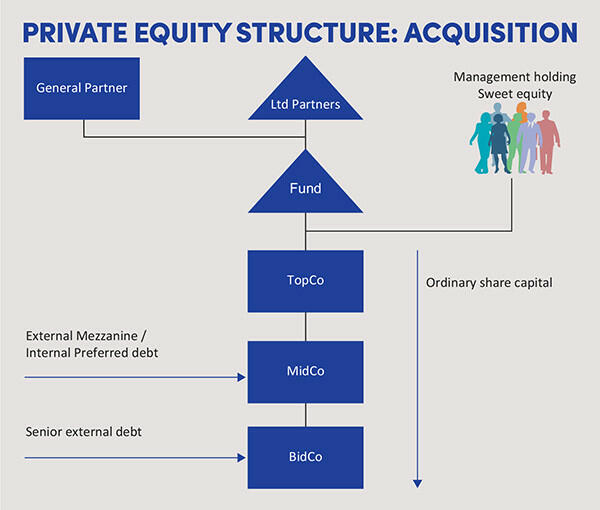

In private equity transactions, a leveraged buyout is a standard acquisition mechanism used by funds to manage the financial exposure towards the committed capital provided by investors to the fund vehicle at the time of acquiring the ‘Target’.

As shown in the diagram Private equity structure: acquisition, a stack of three holding companies (TopCo, MidCo and BidCo) are incorporated by the fund using a mix of debt and equity instruments to make the acquisition. Where external debt is sought, it is typically obtained at the level of the BidCo, while any subordinated instruments may be issued at the level of the MidCo. At the level of TopCo, the ordinary share capital is issued to shareholders, including existing and new management who may be incentivised through sweet equity arrangements.

Considerations for existing management

Where management owns shares in the existing Target structure, a rollover mechanism is generally employed (where available) to allow management to reinvest. A rollover can be undertaken while partially crystalising any value sought upfront. Alternatively, where the sale proceeds received by management are fully reinvested in the new structure, this should mitigate the risk of dry tax charges arising for the management investors.

In certain situations, it may be more suitable for management to invest at the level of BidCo; for example, where the fund intends to incorporate a platform vehicle within the holding stack to hold several more portfolio acquisitions, to be made in future as part of an investment mandate.

Management may choose to invest in their capacity as individuals, or through their own corporate vehicles, especially for UK purposes where a cumulative shareholding of at least 10% is offered to management as part of the acquisition deal. This could enable management’s investment vehicle to benefit from the substantial shareholding exemption (SSE) (discussed in further detail below).

Alternative options available at exit

Whilst investment cycles can vary (depending on different investment considerations), a fund may start to consider an exit around the third or fourth year of holding an investment. The usual manner of exit revolves around the following options, as discussed in further detail below:

- Outright exit: A sale to an external third party, at the level of TopCo or BidCo

- Full or partial exit: This could occur by way of an initial public offering in capital markets

- Realisation of value, without exit: A dividend recapitalisation

1. Sale to an external third party

This exit route is the least complex and generally permits the most flexibility in achieving an efficient exit.

As a starting point, the outright sale of a UK tax-resident investment to an external third party can be expected to result in capital gains or loss treatment for the seller (vendor), and (absent specific exemptions) stamp duty at a rate of 0.5% on the value of the consideration for an acquirer.

In relation to the seller, the UK’s SSE may be able to provide some relief (Taxation of Chargeable Gains Act (TGCA) 1992 Sch 7AC). The SSE has three main requirements:

- The investing company must have held a substantial shareholding in the company invested in; i.e. at least 10% of ordinary share capital, beneficial entitlement to profits available for distribution and assets available for distribution upon a winding up of the business.

- The investing company must have held a substantial shareholding throughout a 12 month period beginning not more than six years before the day on which the disposal takes place.

- The investee company must also be a ‘qualifying company’; i.e. a trading company or the holding company of a trading group or a trading subgroup throughout the period beginning with the start of the latest 12 month period of the substantial shareholding requirement being met, and ending with the time of disposal.

In relation to the investors in a fund, the SSE applies to each investor on their interest in the substantial shareholding in the investee (i.e. the Target). The SSE is, however, only available to the corporate entities subject to UK corporation tax, which have invested through the fund or (in the case of management) where management’s investment vehicle is a corporate vehicle.

Management investing in their capacity as individuals may be able to make use of business asset disposal relief, subject to the £1 million lifetime limit. Broadly, business asset disposal relief is available to company directors and employees who dispose of their shares or securities in the personal trading company (i.e. the Target) that they work for; and company directors and employees who acquired shares in the Target under an enterprise management incentive option scheme. The conditions for business asset disposal relief will need to be assessed at the time of disposal.

It should also be considered at which level management has invested (i.e. at TopCo or BidCo level), as this will ultimately determine at which level exit should occur for all investors.

A sale to an external party generally provides greater control and flexibility over the sales process for the fund.

2. An initial public offering

An initial public offering, where terms are mainly predetermined by external forces such as security laws, exchange rules and underwriters, typically results in a more strenuous, complex and therefore costly exit process. Ultimately, the decision should take into account other strategic and market factors which could favour an initial public offering exit.

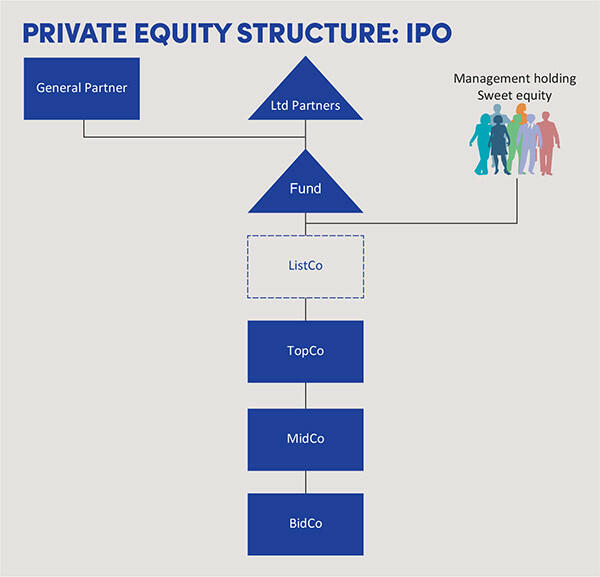

An exit via an initial public offering will typically involve using a new corporate vehicle within the investment holding stack; i.e. a new ListCo (as shown in the diagram Private equity structure: initial public offering). Using a new ListCo provides a ‘clean’ corporate vehicle to undertake the initial public offering, with no corporate history, thereby removing the risk of carrying legacy historical matters for new investors.

ListCo will initially be incorporated by the fund into the holding stack as a sister company, sitting alongside TopCo. Thereafter, the shares of TopCo can be transferred by the fund, management and/or co-investors, in exchange for additional shares in ListCo via a share for share exchange.

A share for share exchange can be undertaken in accordance with TGCA 1992 s 135, and applies in three scenarios:

- A shareholding of at least 25% will be exchanged as a result of the transaction, such that ListCo holds at least 25% in TopCo.

- A general offer is made to shareholders of TopCo holding any class of shares and through such exchange, existing shareholders in TopCo will achieve the result that ListCo controls TopCo.

- Where ListCo holds the greater part of the voting power of TopCo as a consequence of the exchange.

For the shareholder in TopCo, the share for share relief allows TopCo and ListCo to be treated as one and the same company, conducting a reorganisation of its shares. While more stringent requirements apply, share for share relief is also available in relation to stamp taxes (Finance Act 1986 s 77).

Similar to the relief provided through the SSE as discussed above, the share for share rules will apply to the investors in the fund, in relation to their interest in the shares of TopCo as held by the fund. Whether the requirements of any of the three share for share scenarios will be met will additionally need to be considered in light of the transparent/opaque entities investing in TopCo, and subsequently ListCo, through the fund or through other vehicles.

The outcome of the share for share step is for the investors to be holding shares in ListCo, which will then list and at which point the investors will then dispose of their shares. As a result of the sale of part of the shares in ListCo to the public, a partial disposal event will occur at the time of listing, crystallising the value extracted by the fund. Consequently, capital gains tax treatment will follow for the taxpayer investors in the fund in relation to this portion of their investment.

The SSE will once again be of relevance to provide any relief in this regard. While the SSE provides relief for the taxation of any chargeable gains made, it denies tax relief for capital losses which would otherwise have been available for offset against current year and future capital gains in line with the loss relief rules.

In relation to investors who previously incurred capital gains tax and stamp duty under the share for share exchange, provided that the shares in ListCo are disposed of soon after such pre-transaction step, any gains or losses generated at the time of listing should be nominal.

3. A dividend recapitalisation

This ‘exit’ alternative involves the realisation by the fund and management investors of the value in the investment through the receipt of dividends, which may need to be financed, depending on the cash position of the entity. While value is ultimately extracted from the investment under this approach, this alternative does not involve a disposal of the underlying share investment from a legal perspective.

To effect the dividend payment to shareholders, the Target could: (i) use cash reserves on hand; (ii) fund the dividend using (additional) debt; or (iii) use a combination of both methods.

Where the Target is subject to UK corporation tax, the deductibility of interest expense in the hands of the Target should be considered in light of the UK’s interest deductibility rules, such as the corporate interest restriction rules.

Conclusion

Investors in private equity funds are encouraged to consider the potential implications of exiting their investments well ahead of time in the fund investment cycle. The potential tax implications arising on exit for investors can be more readily understood and prepared for, the earlier such planning takes place.