A challenging exercise

Share this article

Seb Purbrick and Simon Mahon consider the new provisions which enable resident non doms to remit some funds to the UK that are not taxable

Key Points

What is the issue?

Certain UK resident, non UK domiciled (RND) individuals will have their tax status changed fundamentally from 6 April 2017. Individuals resident in the UK for 15 out of the past 20 tax years will be subject to income and capital gains tax on a worldwide basis. New provisions will allow offshore assets to be ‘rebased’ on 5 April 2017 and the segregation of untaxed unremitted income, capital gains and clean non-taxable capital (subject to certain conditions), enabling RNDs to remit some funds to the UK in a more favourable manner than was possible pre 6 April 2017. It is this latter issue that we consider in detail.

What does it mean to me?

RNDs will now be faced with a much more complex set of circumstances when they consider how to manage their tax affairs and remittances of funds into the UK. Advisers with RND clients will need to be familiar with the law and work closely with taxpayers and their banking professionals to guide them through the process.

What can I take away?

This is an opportunity for all RNDs who have filed on the remittance basis to assess their offshore bank account set-up and rearrange their tax affairs to make their remittance strategy tax efficient.

Many readers will be familiar with the long standing principle of taxing RNDs on offshore income and gains only when these income/gains are remitted to the UK, known as the ‘remittance basis’ of taxation. In 2008 major reform was undertaken through the introduction of sections 809A to 809Z10 into Income Tax Act 2007. This included the £30,000 remittance basis charge (RBC) applied to RNDs wishing to claim the remittance basis in their eighth year of UK tax residency (seven of nine years test) and in later years the RBC was increased for 12 of 14 years (£60,000) and 17 of 20 years (£90,000).

From 6 April 2017, those who are resident in the UK for 15 of the prior 20 years are deemed UK domiciled for the purposes of income tax, capital gains tax and inheritance tax. The effect of these deemed domicile rules is to tax such long term RNDs on worldwide income and gains as they arise; there is no ability to claim the remittance basis. Inheritance tax will be levied on an individual’s worldwide estate, as was previously the case where RNDs were UK resident for 17 of the prior 20 years.

The taxation of RNDs has undergone significant changes in recent years. This has been driven largely by the desire of successive governments to aggressively tackle tax avoidance and evasion. In addition, HNWIs and RNDs in particular remain in focus in certain sections of the media.

Another significant change is that individuals born in the UK with a UK domicile of origin, who have been living overseas and have acquired a domicile of choice in another jurisdiction, will be considered UK domiciled if they return to live in the UK.

In order to help long term residents move from the remittance basis to worldwide taxation, two provisions have been introduced:

- Individuals that have paid the remittance basis charge in any year to 5 April 2017 and that are becoming deemed domiciled on 6 April 2017 (no later) will be able to rebase certain foreign assets to their 5 April 2017 value, meaning the appreciation of the asset to 5 April 2017 value will not be charged to capital gains tax at later disposal.

- All remittance basis users will be able to cleanse mixed funds in the two year period to 5 April 2019. This enables a bank account containing untaxed unremitted income, capital gains and clean non-taxable capital to be segregated through moving the constituent parts to separate accounts. It will then be possible to remit funds from the new accounts to the UK in the most favorable manor.

In this article we will focus on the opportunity to cleanse mixed funds.

Cleansing of mixed funds: an opportunity not to be missed

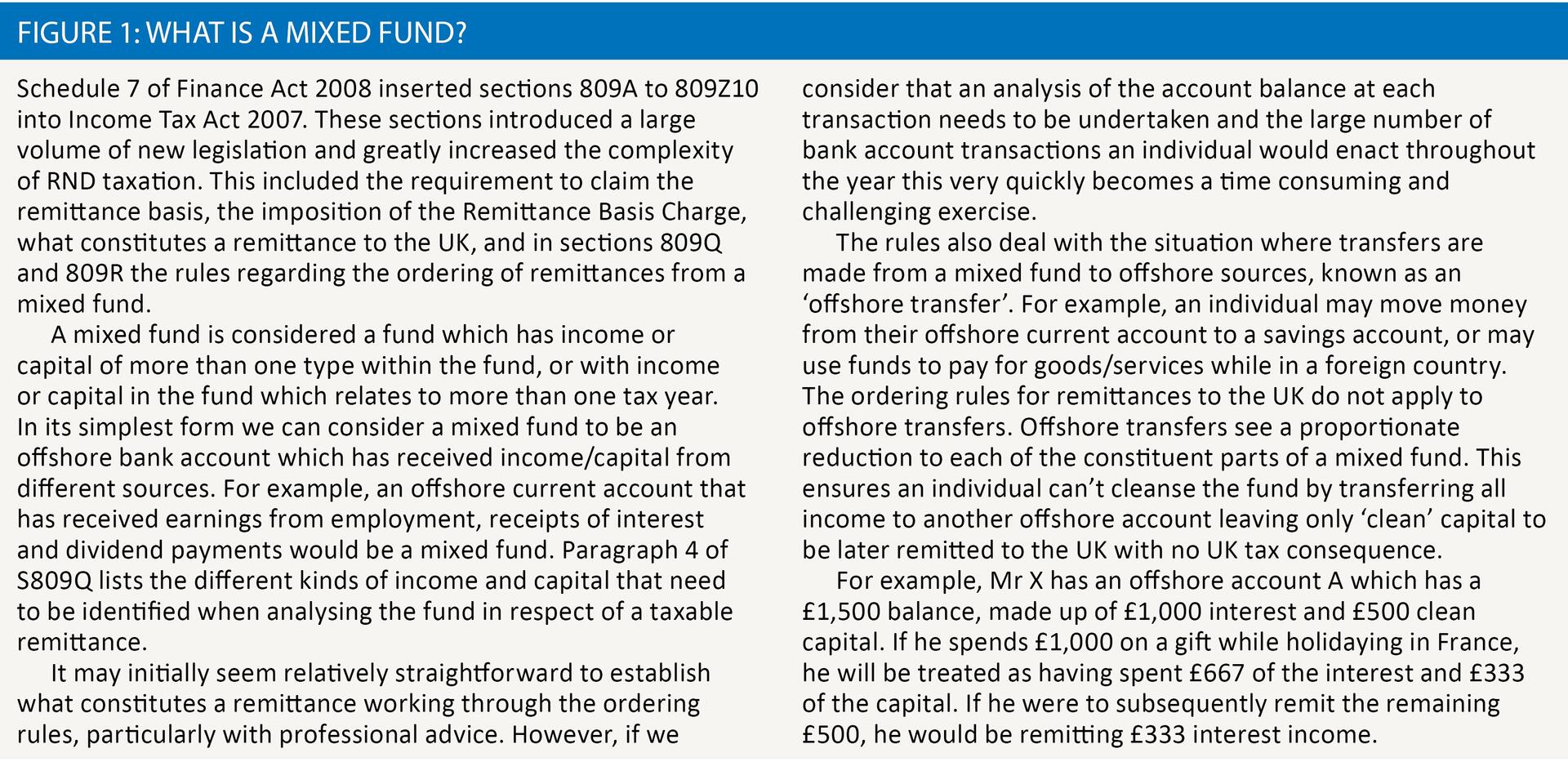

A set of ordering rules were legislated for in sections 809Q and 809R, which enable a taxpayer to determine the nature of the remittance when a remittance is carried out from a mixed fund (see figure 1 for the definition of a mixed fund).

Given the complexity of the ordering rules and the fact the ordering is penal from a tax perspective, the cleansing of mixed funds is a welcome opportunity available to remittance basis users. As it is available to all remittance basis users, not only those becoming deemed domicile, it should be considered by anyone with any mixed funds.

Taxpayers will need to work closely with their tax adviser and private bankers in order to trace back transactions and set up new accounts to receive amounts from cleansed accounts. Persons deemed domiciled at 6 April 2017 will also need a bank account structure to receive income etc post April 2017 which shouldn’t be mixed with pre-6 April 2017 funds.

Figure 2 provides an example of account cleansing.

Practical challenges

The first step for any taxpayer will be to carry out analysis of their mixed fund. This will be challenging at times as it is not uncommon for taxpayers to have offshore income/gains within a mixed fund dating back many years. HMRC have stated an individual must be able to identify the income/capital/gain within the fund to benefit from the rules.

In addition, where they have not done so already, it will be important to set up a bank account structure with different accounts for income, capital gains and clean capital as a minimum. Taxpayers will need to understand the purpose of each account and be diligent in not tainting an account with an incorrect source of funds.

The illustration in figure 2 is a simplistic example of account cleansing. Matters can become fairly complex when considering different type of investments, different currencies and the other aspects of their tax affairs.

For instance, investments may be held within a partnership structure; for US citizen RNDs it is common to invest funds through a Limited Partnership. The individual will receive an annual K-1 statement (the US equivalent of a UK Partnership Return) from the partnership which states the trading income, interest, dividends, gains, foreign exchanges rate gains, available deductions etc.

The K-1 will have been prepared to US tax principles, not UK. In addition, under gain recognition rules, the partnership will allocate gains to the partner which may not have crystalised. Were the partner to exit the partnership and realise the capital balance into an account, being able to determine the type of income/capital/gain held within the capital balance and reconciling with any amounts previously distributed can be an extremely detailed and challenging exercise.

This is one example of the complexity that can arise but there will be many more as clients and advisers encounter different scenarios.

Other points of note

The remittance basis of taxation has been available long before sections 809B, 809D and 809E of ITA 2007 was written, which gave rise to the question of whether it would be possible to cleanse funds arising prior to 2007/08?

This question was raised within the consultation period and in response the Chancellor advised in the Spring Budget 2017 announcement that mixed funds from 2007/08 and earlier years will be able to benefit from account cleansing. However, the legislation in the Finance Bill issued 20 March has not been updated to allow for this through statute, so we await confirmation of this through further updates. At the time of writing this has not been received.

Whilst very welcome, it was somewhat surprising this opportunity has been made available to all RNDs and not just those becoming deemed domicile on 6 April 2017, in contrast to the rebasing provisions which are far more restricted. Is this implicit acceptance by HMRC of the unnecessary complexity of the remittance ordering rules?

As noted previously, an individual born in the UK with a UK domicile of origin cannot benefit from mixed fund cleansing opportunity, but an individual born outside of the UK with a UK domicile of origin may well be able to benefit. It is unclear why the government has taken this approach and it seems that persons born outside of the UK to UK domiciled parents are in an extremely advantageous position.

Conclusion

The complex world of non domiciled taxation continues, however, RNDs have some respite through an unexpected opportunity which should not be missed. Consultation with professional advisers and private bankers will be key to utilising the opportunity.