Combining employee ownership trusts with share schemes: a complicated compound

Share this article

If you wish to reward the management team in an employee ownership trust with share schemes such as enterprise management incentive options, what are the traps to avoid?

Key Points

What is the issue?

A common question when establishing an employee ownership trust is how to reward, incentivise and retain the management team. Share schemes, such as enterprise management incentive options and growth shares, are an obvious answer.

What does it mean to me?

There are several traps for the unwary as a result of the drafting of the employee ownership trust legislation under the Taxation of Chargeable Gains Act 1992.

What can I take away?

Employee incentivisation must be carefully considered in designing an employee ownership scheme structure and ensuring that the structure is flexible enough to allow such schemes in the future.

More and more is being written about employee ownership trusts and the tax incentives available when establishing them (see ‘Employee ownership trusts’, Tax Adviser, April 2023), not to mention the intended commercial benefits such as rewarding and retaining staff.

Individuals who are seeking an exit may be keen to utilise these structures for a tax-free exit, whilst realising a full market value for their shares. However, the benefits to employees are arguably less significant, mainly being the £3,600 per annum income tax-free bonus and, perhaps, the ability to pay staff higher salaries as no shareholders are requiring a return on capital in the form of dividends.

Thus, a particular concern for the exiting shareholders may be retaining the key management team, particularly as they are often crucial to ensuring that the business continues to flourish and therefore meet the terms of the employee ownership trust’s deferred consideration requirements. However, for the management team, a £3,600 income tax-free bonus is unlikely to be a significant incentive given their existing remuneration level.

A common question when establishing the structure of an employee ownership trust is therefore: ‘How do I further reward, incentivise and retain the management team?’

Share schemes, such as enterprise management incentive options and growth shares, are an obvious answer. However, there are several traps for the unwary as a result of the drafting of the employee ownership trust legislation (see Taxation of Chargeable Gains Act (TCGA) 1992 ss 236H – 236U).

It is also important to note that a straightforward gift of shares to an employee is unlikely to be possible in an employee-owned company due to the equality requirement of TCGA 1992 s 236J. This requires that shares in the trusts must be applied for the ‘benefit of all the eligible employees on the same terms’. Clearly, gifting shares to a single employee would contravene this provision, resulting in a disqualifying event.

This article does not intend to detail the employee ownership trust, enterprise management incentive or growth share rules but rather highlight the specific areas to consider when combining share schemes with an employee-owned company.

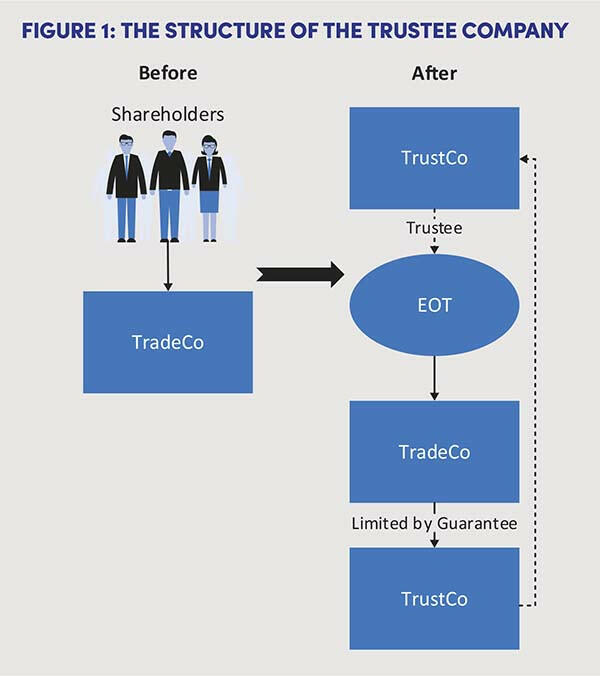

The structure of the trustee company

To provide protection for the trustees, it is common to establish a trustee company of which the trustees will be directors. Furthermore, this company is often established as a subsidiary within the group (see Figure 1: The structure of the trustee company).

This structure creates a circularisation of ownership: the trust company is the trustee of the employee ownership trust, which owns the trading company, which in turn then has the trust company as a subsidiary. With checks and balances inherent within the structure and trustees who have detailed knowledge of the business, the company can be efficiently and cost-effectively managed without the need for an independent owner.

It is often proposed that a company limited by guarantee is the sole corporate trustee; however, this is where our first issue arises.

For enterprise management incentive purposes, a qualifying company is one that only has qualifying subsidiaries (Income Tax (Earnings and Pensions) Act (ITEPA) 2003 Sch 5 Part 3 para 8). The conditions of being a qualifying subsidiary include, among other things, the subsidiary being a ‘51% subsidiary’ (ITEPA 2003 Sch 5 Part 3 para 11).

This 51% subsidiary test applies to shareholders. Where the trustee company is a company limited by guarantee, it will not be a qualifying subsidiary by virtue of having no shares in issue. The result is that the trading company will fail to be a qualifying company for enterprise management incentive purposes and consequently enterprise management incentive share options cannot be issued.

There are two remedies to this problem. The first is to ensure that the trustee company limited by guarantee is held outside the group. Of course, this results in a loss of the circular ownership structure and the requirement for an independent owner.

Alternatively, ensure that the trustee company is a company limited by share capital. This may therefore be held within the group without the company failing the 51% subsidiary test.

Where an employee ownership trust structure is already in place and further employee incentivisation is desired, if the trustee company is limited by guarantee within the group, two solutions may be available:

- Issue growth shares as an alternative to enterprise management incentive options as there are no such qualifying conditions.

- Restructure the group to remove the trustee company. This should be a relatively straightforward solution on the basis that the trustee company is unlikely to have any real value. However, there are likely to be administrative costs involved in undertaking the process.

Either way, considering these issues on the implementation of the employee ownership trust, regardless of whether enterprise management incentive options are immediately envisaged, will save potential issues in the future.

The effect on the limited participation fraction

A second issue to be aware of concerning employee incentivisation within an employee-owned company concerns the limited participation fraction which is outlined within the employee ownership trust legislation at TCGA 1992 s 236N, as follows:

The numerator also includes individuals who are both connected to the participator mentioned above and also an employee or office holder. Where this fraction exceeds two-fifths, the requirement is failed.

Participators for this purpose follow the definition provided by the Corporation Tax Act (CTA) 2010 s 454. However, TCGA 1992 s 236N(6) requires a minimum of 5% for the purposes of the employee ownership trust legislation. The exact wording of this subsection is:

‘The participators in C who are referred to in subsections (2) and (5) do not include any participator who:

a) is not beneficially entitled to, or to rights entitling the participator to acquire, 5% or more of, or of any class of the shares comprised in C’s share capital; and

b) on a winding-up of C would not be entitled to 5% or more of its assets.’

Are option holders participators?

There are two important phrases in (a) above.

The first is ‘or to rights entitling the participator to acquire’. This brings share options into consideration; for example, an enterprise management incentive option enabling the managing director of the company to acquire 20% of the ordinary shares in the company will be treated as a participator for the purposes of part (a) above.

This is consistent with the definition of a participator which states that a participator includes ‘a person who possesses or is entitled to acquire, share capital or voting rights in the company’ (CTA 2010 s 454(2)(a)). Again, being entitled to acquire share capital may include share options.

The second is ‘or of any class of the shares’. This means that the share (or option) holder only needs to hold 5% of a particular share class and not the entire share capital to be caught by s 236N(6)(a).

The effect of this wording is that even two members of the management team holding growth shares in a separate class will hold 50% of that class, meaning they fall within the definition of a 5% participator.

Interestingly, both points are specifically included in s 236N(6)(a) and not s 236N(6)(b), meaning option holders may not have any right to 5% of the company’s assets on a winding up unless, or until, the options are exercised.

Exit only options

However, we must also consider the scenario where enterprise management incentive options are granted that are ‘exit only options’; for example, where the enterprise management incentive options entitle the individual, in the event of a sale or winding up, to 5% of the share capital and subsequently to 5% of the sale/liquidation proceeds.

Consequently, there may be a case where exit-only options could very well fall within the definition of a participator under s 236N(6).

Growth shares and the participator fraction

In the case of growth shares which are granted at (or shortly after) the time of sale to the employee ownership trust, assuming the rights of the growth shares only entitle the holder to a certain percentage of capital value in excess of the capital value at the date of issue, growth shares will not cause the holder to be a participator for employee ownership trust purposes immediately.

Summary

As a result of this, it is quite possible that neither enterprise management incentive share options nor growth shares will cause an immediate issue with the limited participation fraction. Also, given that the exiting shareholders’ capital gains tax relief will only be clawed back if the conditions are failed at any time up to the end of the tax year following disposal, this will rarely be their problem.

It is, however, an important point for the trustees to be aware of, as the failing of the limited participation fraction at any point following the end of the tax year following disposal will result in a deemed disposal and reacquisition by the trustees.

The mechanics of capital gains tax relief of the vendors is that of a no gain no loss disposal, meaning that the trustees inherit the base cost of the vendors, often a nominal value. A disqualifying event triggered by the exercise of share options, or growth shares falling within the above definitions, is therefore likely to cause a significant capital gains tax liability for the trustees.

Either way, employee incentivisation must be carefully considered in designing an employee ownership scheme structure and ensuring that the structure is flexible enough to allow such schemes in the future. It will also be important for the trustees to be fully briefed and understand under what circumstances a disqualifying event may be triggered.

The intentions of the employee ownership trust legislation are to encourage employee ownership. However, incentivising key management of an employee-owned company within the employee ownership trust legislation itself (e.g. £3,600 income tax-free bonuses) is unlikely to present a major benefit to them. Therefore, how the two schemes interact should perhaps be reviewed in more detail. Relaxations of enterprise management initiative qualifying conditions for employee-owned companies should be considered, much like the business asset disposal relief regime provides relaxations for enterprise management incentive shareholdings.