The coronavirus job retention scheme – mistakes and corrections – are underclaims just as important as overclaims?

Share this article

Susan Ball and Carolyn Brown discuss the coronavirus job retention scheme (CJRS) and some of the key issues associated with reviewing employer claims and correcting mistakes, including considering the tax charges and penalties that may apply where claims have gone wrong.

On 20 March 2020, the CJRS was introduced, providing a support grant for all employers that could not maintain their workforce because their operations were affected by coronavirus (COVID-19). The scheme allowed employers to furlough their employees from 1 March 2020 where they were on a UK payroll initially as at 28 February 2020. Who could have predicted back then that the scheme would be in place for more than a year?

Employers that claimed in the early days after the initial guidance came out, worked out their own version of how reference pay calculations should be done, particularly for variable pay employees, where the 2019/20 average pay needs to be considered, as the guidance was less than clear. Those employers may not have revised the reference pay calculations each month or been aware of changes to and extensions of the HMRC guidance which, over the course of the year has ultimately made HMRC’s view on how the calculations should be done much clearer.

HMRC CEO Jim Harra told MPs that the department had made an assumption for the purposes of planning that the error and fraud rate for the CJRS scheme could be between 5 per cent and 10 per cent. So HMRC is expecting that employers may have made mistakes.

Many employers have started to review claims, since the introduction of the specific CJRS penalty legislation, and as time has allowed. This has identified numerous examples of unintended errors, resulting in claims that either overstate or understate the amount of CJRS grant they are entitled to. It seems the risk of penalties has also prompted some employers to pay back the grants received to avoid any worry, although business hasn’t been as bad as expected for others.

Broadly, what are the major developments in the CJRS since March 2020?

In summary, we have had:

CJRS Version 1 - 1 March to 30 June 2020. Full furlough for a minimum 21 days

- The maximum grant value is 80 per cent of a furloughed employee’s wages (the reference pay, as defined in the legislation) up to a cap of £2,500 per person per month plus employer’s National Insurance contributions (ER NICs) and employer’s auto enrolment minimum pension contributions on those wages.

CJRS Version 2 – 1 July to 31 October 2020. Flexible furlough allowed if employee was eligible/claimed for under CJRS Version 1, subject to the maximum number of employees in a CJRS Version 1 claim.

- 1 July to 31 July - as for CJRS Version 1 above but only for furloughed hours.

- 1 August to 31 August - the maximum grant for furloughed hours is 80 per cent of a furloughed employee’s wages (the reference pay, as defined in the legislation) up to a cap of £2,500 per person per month.

- 1 September 2020 to 30 September 2020 - as for 1 August to 31 August, but the Government grant was 70 per cent and the employer had to fund 10 per cent of furloughed employees’ wages (as defined in the legislation) during furlough periods.

- 1 to 31 October 2020 - the Government grant was 60 per cent and the employer had to fund 20 per cent.

- The employer was required in August, September and October to continue to contribute ER NICs and employer’s pension contributions.

CJRS Version 3 - 1 November to 30 April 2021. Flexible furlough allowed and employees can be claimed for even if not previously claimed under CJRS Versions 1 and 2.

- The maximum grant value is 80 per cent of a furloughed employee’s wages (the reference pay, as defined in the legislation) up to a cap of £2,500 per person per month.

What is HMRC doing to check claims?

In the Treasury select committee hearing on 7 December 2020, there were some rather interesting statistics on the coronavirus support schemes. Approximately £12m of claims relating to the CJRS had been rejected by HMRC, which had also undertaken further reviews into 140,000 submissions prior to approving payment by the time of the hearing. HMRC's view is this approach has rejected most suspect claims, believing that the level of criminal activity for the CJRS is low, at between 0 per cent and 0.6 per cent.

As this demonstrates, HMRC is investigating claims, and several arrests for fraud have been made at the time of writing. HMRC has also written to large numbers of employers to invite them to correct any claims which, based on the data HMRC holds, may be incorrect. We understand the next step, where employers have not responded to these letters, is further investigation by HMRC.

What should employers be doing?

We would urge employers that have potentially made errors, or that have not reviewed their claims yet, to take action as soon as possible. Where errors have been made, we would advise employers to consider what actions need to be taken to rectify them.

HMRC’s compliance work is aimed to identify and address incorrect claims, particularly those arising from deliberate non-compliance and criminal behaviour. HMRC have stated they will not be actively looking for innocent errors in their compliance approach, however where employers find mistakes, they must put them right.

HMRC can now require employers to provide information regarding incorrect claims and, where appropriate, can hold directors personally liable as if it were tax, pursuant to s100 and Schedule 13 Finance Act (FA) 2020, where the business is no longer solvent. Where businesses have received wrongly claimed CJRS payments, those payments are taxable at a rate of 100 per cent, allowing HMRC to recover the payment through tax pursuant to Schedule 16 FA 2020.

Schedule 16 FA 2020 also imposes a burden on employers, in a similar manner to the Bribery Act 2010, to notify HMRC of any amounts that have been wrongly claimed to avoid penalties.

A 90-day ‘correction window’ was included for employers to make such notification. The correction window is prescribed as the latest of:

- 90 days from the receipt of the grant;

- 90 days from circumstances changing, meaning the employer is no longer entitled to retain the grant; or

- 20 October 2020.

Each employer that has received a CJRS grant payment now has the positive duty to notify any wrongly received amount and self-assess that amount in their tax return. Any failure to notify wrongly received amounts by the above deadline could be subject to penalty (in addition to the tax charge) under Schedule 41 FA 2008.

Where an employer does not meet the above notification deadline and where they knew that they were not entitled to receive grant monies at the date income tax first became chargeable, any penalty under Schedule 41 FA 2008 may be imposed on the basis that such wrongdoing was ‘deliberate and concealed’, meaning a maximum potential penalty of 100 per cent of the amount improperly claimed.

For the most serious cases, criminal prosecutions are likely and there are a number of (statutory and common law) offences that may be relevant, including the strict liability corporate criminal offences under the Criminal Finances Act 2017.

So, if an employer receives an HMRC letter requesting a reply by a set date, it should be taken seriously, and work should be undertaken to review claims and reply to HMRC by the set date.

It should be noted that for entities to which it applies, CJRS grant claims fall within the senior accounting officer (SAO) regime and hence can lead to personal liabilities on SAOs of employers that are not compliant.

Also, be aware that HMRC may not be the only interested party, an organisation’s auditors are likely to want to make sure CJRS claims are materially correct as well.

Errors will often tend to fall in the following broad categories.

- Administrative errors occurring when inputting details of a claim.

- Errors made when calculating the amount of grant available to claim, particularly in light of the challenges in applying complex rules.

- Incorrectly including claims for employees for whom the employer is not eligible to claim.

Further information about assessments and penalties is in HMRC's compliance factsheet CC/FS48.

Are underclaims and overclaims of CJRS grants equally important?

In short, they can be. The focus of HMRC activity and much of the reporting on the CJRS has been on overclaims so let’s cover that first.

If an employer has made an error in a claim that has resulted in an overclaimed amount of grant, they must pay it back to HMRC. This can be reflected in the employer’s next claim and the amount paid in respect of that claim can be adjusted accordingly.

If an employer takes this approach, they do not need to do anything further with regard to the amount overclaimed because it will be rectified in the next CJRS grant payment from HMRC. However, a record of the adjustment must be kept for six years.

Where an employer is not making any further CJRS grant claims or the overclaim is too large to recover from the next claim, they will need to contact HMRC to notify it of the issue and request a payment reference to pay the money back. This should ideally be done before the end of the penalty free window but, if not, as soon as it is possible after the issue comes to light.

Surely grant underclaims are not a problem then? Unfortunately, technically that’s not correct. The legislation is drafted in such a way that an underclaim is, from a practical perspective, as serious as an overclaim. This is because it potentially makes the whole claim for the employee concerned invalid and that cannot be easily resolved in the employer’s next claim.

We have seen examples of employers that have incorrectly calculated an employee’s reference pay which could jeopardise each and every claim for that employee using that reference pay calculation. On discussing these examples with HMRC, it has been confirmed that where the employer followed the HMRC guidance available at the time of the claim there may be no repayment required and no tax charge or penalty. For example, employees who had significant overtime could have been designated as fixed pay employees until 7 August when the guidance changed. However, when the further guidance came out in relation to such employees, the employer should have reconsidered the position and this might have resulted in those employees being assessed to be variable pay employees for the purposes of further CJRS grant claims. In such cases, we understand HMRC would not propose taking action in relation to the earlier period. However, it does leave the employer potentially exposed to tax and penalties if they didn’t review the calculations for those employees in light of the updated guidance and come to the right decision for claims made from 7 August 2020 onwards.

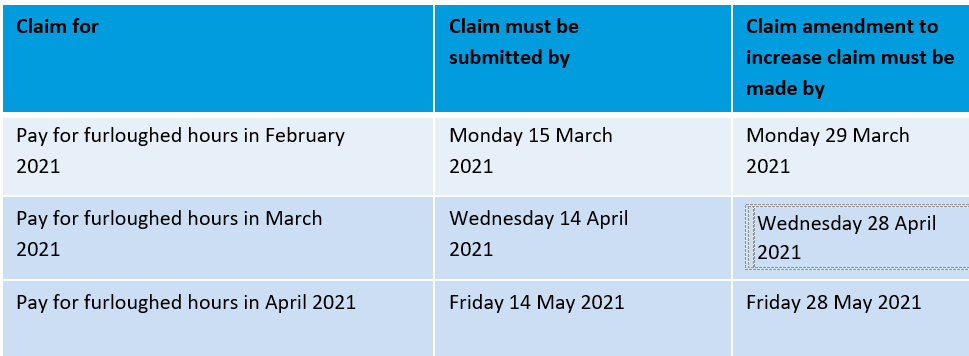

Unfortunately, underclaims under CJRS Version 1 and CJRS Version 2 are not able to be rectified via HMRC by claiming more grant monies. Only errors in claims made under CJRS Version 3, if they are notified within the tight correction window (see table below), can be corrected by claiming more grant.

Should employers notify HMRC and explain the issue and/or document the approach taken? Should they increase amounts paid over to employees to ensure they receive the amounts they should have received had the grant claims been calculated correctly? Both are options to consider.

If an employer has contracted in a furlough agreement to pay an agreed level of pay but the furlough pay rate does not match the agreement, the employer may be subject to an employee claim for unlawful deduction from wages or a contractual claim for wages. The latter can be made for up to six years. The same will apply if the furlough agreement fails to secure agreement in writing from the employee to a salary reduction, even if it falls within the scope of the CJRS rules.

Common mistakes

- Common mistakes we have seen in calculating CJRS claims include:

- incorrect day counts or use of working days rather than calendar days;

- reference pay including discretionary payments;

- reference pay not including non-discretionary payments (as defined);

- reference pay not including contractual overtime or employees designated as fixed pay but with significant overtime and no reassessment after the guidance changed on 7 August;

- use of 2019/20 average pay details only or an incorrect method used to calculate the average pay for variable pay employees;

- incorrect use of pre-salary sacrifice remuneration figures;

- employees only furloughed for holiday periods;

- problems with calculating the correct pension payments eligible for claims;

- not restricting NICs calculations where required;

- misunderstanding of what employees were able to do when on furlough; and

- invalid earlier furlough days/periods preventing a later valid claim under CJRS Version 2.

Can CJRS claim mistakes lead to other issues?

Yes, potentially - for example, there may be employment legal issues and, in relation to salary sacrifice, potential for unlawful deductions. Where the salary sacrifice relates to pensions contributions, there is also potential for incorrect pensions payments leading to underfunded pension schemes. The availability of the grant under the CJRS does not change an employer’s usual pension contribution payment obligations or processes.

When calculating the pension contribution due for a furloughed worker who has agreed a salary sacrifice arrangement for pension contributions, any contractual obligations the employer has entered into, and the obligations in the pension scheme rules, continue to apply as normal.

However, as all of the grant claimed must be paid to a furloughed worker in the form of money (between March 2020 and June 2020) and the furloughed worker must be paid the lower of 80 per cent of their wages or £2,500 per month or the pro-rated equivalent if the member of staff is working part-time (from 1 July 2020), this may mean that, where a salary sacrifice arrangement is in place for pensions, an employer will need to amend their payroll processes to calculate the pension contribution to be paid to the pension scheme under the pension scheme rules.

The pensions regulator has provided detailed guidance at

COVID-19 technical guidance for large employers | The Pensions Regulator

What guidance should employers have used to make a claim?

We understand HMRC expects employers to have followed its guidance and have picked up on the many changes made since it was first published. More than 200 changes have been made to the guidance since the scheme was introduced in March 2020. If the factual basis of a claim is correct and it has been calculated in accordance with HMRC’s guidance, then the claim is, in all likelihood, correct.

However, there are some issues where the guidance is not or has not been clear. In these cases, it seems HMRC expected employers to take professional advice or to consider the appropriate legislation in the relevant Treasury Direction that applied at the time.

From our discussions with HMRC, it is clear that employers were expected to check the HMRC guidance each time they made a claim, to consider if it had changed and what action should be taken in view of the sums of money involved. HMRC also expected claimants to make sure they kept an audit trail of key decisions or problem areas to demonstrate the decisions taken, with copies taken of the version of the guidance version relied upon for the calculations.

If, on reviewing claims, an employer spots an error but believes the HMRC guidance in issue at the time was followed, we would recommend they write to HMRC detailing the position and present their case. This would serve as notification of an error, but HMRC may agree that in the circumstances a correction is not needed.

Employers that used the HMRC tool to calculate grant claims should also review the position to make sure the correct information was input when preparing claims - although HMRC should not challenge the calculation itself, errors may have been made, for example in what is or is not included in reference pay, which may impact several claims.

HMRC has made it clear that its priority is to support customers, while addressing deliberate non-compliance and criminal attacks, so we would expect HMRC to be reasonable where innocent errors are found and brought to its attention.

As a tax adviser what should I be careful of?

CIOT has issued guidance for members on the approach to be taken in various different scenarios.

This guidance is intended to provide assistance in relation to the steps to take if you become aware of errors in coronavirus job retention scheme (CJRS) claims. Whilst this guidance specifically addresses CJRS claims, the fundamental principles and requirements set out in the professional conducts in relation to taxation (PCRT) issued by the professional bodies also apply to other coronavirus support administered by HMRC or other authorities, such as claims under the self-employment income support scheme (SEISS).

CIOT’s guidance was reviewed by HMRC in January 2021 and addresses what are believed likely to be the most common scenarios.

In accordance with the PCRT, advisers have an obligation to not be associated with any tax returns it believes to be incorrect. It is therefore essential that the necessary work is undertaken to identify appropriate adjustments to recognise any necessary tax charges in accordance with Schedule 16, Finance Act 2020 in a client’s tax return prior to submission.

What should employers do now?

Employers are advised to carry out a review to make sure that they have complied with the CJRS rules applicable at the time of each claim and to double check, ideally within the correction window to preclude penalties or other sanction, but in any event as soon as possible, that they have not made any errors when submitting their claims.

It is advisable also for employers to make sure they have paid employees correctly, not only for periods of furlough but also when working. There are added complications of course when dealing with flexible furlough.