Electric Vehicles – the tax conundrum

Share this article

David Chandler discusses the Electric Vehicle revolution and how taxes on vehicles may have to change

You could be forgiven for thinking everybody is already driving an Electric Vehicle (EV) in 2022. Everywhere you look there are adverts for EVs, all the new models being released seem to be EVs, charging stations are opening up all over the country (the newest electric forecourt is due to open in April 2022 in Norwich East!) and if you’re like me, you’re noticing more cars without exhausts!

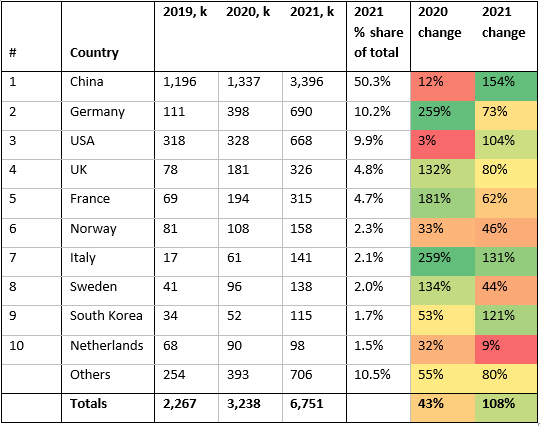

However, as at today, EVs are nowhere near being mainstream in the UK. Whilst we are making good progress – we are currently 4th on the global list of EV sales behind China, Germany and the USA – ‘only’ 412 thousand cars on the road are EVs. Given there are circa 31.7million cars in the UK alone, we have still got a long way to go. Each year approximately 2.3million new cars are sold in the UK (with a large dent in the last few years due to external forces such as Covid, chip shortages, sinking transport vessels and the like – last year it was only 1.6mn). However, we are expecting car sales to return to pre Covid levels at some point. Clearly we still have a long way to go before replacing all new sales of petrol/ diesel vehicles with some form of EV-based vehicle. The table below shows the car sales for EVs and petrol-hybrid electric vehicles (PHEVs) for the last 3 years (red is small increase, green large increase year on year).

Regardless of the numbers, clearly the vast majority of us will be driving EVs at some point in the next 10 years. With all this fundamental change about to happen, what does this mean for the exchequer?

To answer that we probably need to take a look at what happens now.

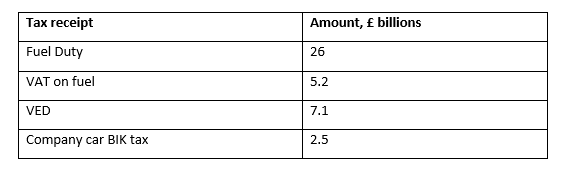

Currently, the exchequer ‘tax-take’ in respect of cars is somewhere in the region of £40billion of tax receipts (depending on which tax years you look at), this is broken down as follows:

As more people move to an EV, all the above taxes are going to be impacted. This is an issue that other countries have gone through, or are going through, for example Norway. They are held up as a shining example of how to use Tax Policy to drive behaviour through using discounts and grants to encourage take up. Very recently however, Norway have started to reduce their EV incentives after providing them for 15 years, and we, the UK, have only just started our EV journey.

In terms of the specific tax receipts, fuel duty is an interesting one because that is the tax that every Budget for the last 12 years has been frozen (rather than increasing with inflation), so that is already being slowly eroded.

If less petrol/diesel is purchased then that is great for the environment, however purely from a taxation point of view, that fuel duty will then plummet. Within the £26bn, a significant proportion is from heavy goods vehicles (HGVs) (someone once estimated that it is roughly 50%, but that’s a difficult number to actually prove with any accuracy). Electric or hydrogen fuel cells may take longer to impact HGVs, especially those undertaking longer journeys.

The VAT on the fuel is clearly driven from the sale of fuel itself but reported separately to fuel duty. The Vehicle Excise Duty (VED) currently is very advantageous towards EVs and company car benefit-in-kind (BIK) tax for an EV is only 2% of list price, the vast majority of the £2.5billion comes from the diesel and petrol company cars. Therefore, the quicker we move to EVs, the quicker circa £25billion (half the fuel duty, VAT, VED and car tax) could simply be lost income for HMRC. That’s a big number, and one that probably can’t simply be met by tweaking other taxes. Obviously there will be other exchequer revenue as a consequence of the move to EVs, but any increase in VAT isn’t likely to be substantial because the cost of EVs is expected to be similar to that of petrol/diesel counterparts in the next few years. Also, the VAT on electricity isn’t likely to plug the gap because VAT on domestic fuel is currently 5% (and in today’s energy climate personally I can’t see the VAT on energy being increased any time soon).

So, what might HMRC do about it?

There are a number of different options, some of which have political connotations to them so need to be weighed up as to whether the Government can afford to bring them in. However, the main aspects that have and are being considered are as follows:

- Road pricing

- Increase in company BIK car tax rates

- A more holistic view of taxation

Road pricing

The talk of the introduction of road pricing is to encourage drivers to take alternative routes or to drive during off-peak times, helping lower the congestion in certain areas. There have been recent talks of introducing a new scheme which can help fill in the potential gap in the budget through two suggested road pricing arrangements.

The first is the ‘pay-as-drive’ scheme where drivers are taxed based on their distance travelled. The rate applied per mile can vary depending on when the person is driving, that is peak times will have a higher charge, the area they are driving in and the type of vehicle.

Another proposed scheme is the ‘road-miles’ scheme where drivers are not taxed on a set number of miles, for example first 4,000 miles are free per annum, but anything above this is taxed at a cost per mile.

Obviously these are just 2 options being discussed and the Government are still in the analysis phase to see if it is something they can do, want to do and practically how they would implement such a fundamental change to the car taxation system.

According to a survey completed by Fleet News, the reception on these schemes has been split for drivers with 45% of respondents being in favour, whilst 36% being against this, and the rest presumably are the few who get public transport so they don’t care.

The technology is partially in place for road charging and so this doesn’t appear to be a major hurdle. Road pricing seems to be more an issue from a political side of the debate, and whether the Government can bring it in. The general consensus in the market seems like there is little alternative so it seems that it will be a question of WHEN it comes in (and how) rather than IF.

Increase in company car BIK tax rates

For many years, company cars have been subject to tax somewhere between 15% and 37% of list price. The Government has brought in the lowest rates in a generation in order to encourage take up through companies; from 6 April 2022 taxation on an EV is based on 2% of list price.

Whilst the Government have announced that this 2% rate will remain until 2025 (which is great news to have certainty for 3 years), there is an expectation within the industry that this low rate of tax will not last. What rate the tax on an EV will be increased to, or how quickly it will increase is unknown, but history shows us increases can be quick and high (from 2017/18 to 2019/20 an EV went from 9% to 13% to 16% in 2 years before the Government decided EVs were the future and they reduced this to 0% in 2020/21).

In addition to the benefit in kind staying low, through the use of legislation the Government have encouraged the use of salary sacrifice for EVs, meaning non-entitled company car drivers can benefit from huge financial incentives to sacrifice gross salary and in return receive a company car subject to tax at 2%.

Every car is different, and the impact varies across tax rates, but from modelling HRUX has undertaken, the financial incentive from salary sacrifice into an EV starts to become marginal when the benefit rate approaches 20% (this does depend on tax rate, if a company share the NIC, do they have early termination insurance?) so the tax rate has got to increase substantially before this benefit becomes expensive. From a HMRC perspective, if everybody switched to an EV overnight, that £2.5bn exchequer revenue drops to a £0.4bn receipt. For the tax/NIC receipts to get back up to the £2.5bn level, either a lot more company cars need to be provided, or (and?!) the tax rate needs to increase substantially from the 2% level.

A more holistic view of taxation

The Government look at the tax receipts into the exchequer as a whole – somewhere between £700bn and £800bn comes in from tax revenues (2021/22 forecast is approximately £732bn). This £25bn, whilst a huge number on its own, suddenly doesn’t look so huge when compared to the income when looking at total tax take, or total PAYE income from all employment (£350bn from tax and NIC).

The Government may choose to take a more high-level view – the taxes from increased jobs created through new industry, new cars, improved technology, and charging stations. Whilst the Institute for Fiscal Studies (IFS) may struggle to correlate tax increases in one area due to decisions in others, it’s the challenge that the Government have as they look to create and update their tax policy.

Summary

We can see that the EV incentives introduced so far have helped improve the EV take-up in the UK dramatically. However, as this increases, so does the need for consideration on the taxation of cars generally. Currently, nothing is off the table, but the Government are obviously thinking hard about what to do. The reality may be that they do a little bit of everything – congestion zones are being created in major cities already, maybe small road charging projects will be created at first?

Alongside this, increases in company car taxes post 2025 (hopefully small, or at least slow and announced with due consideration!) and VED increases (that is removing the current incentives for EV take up) might go some way to bridging the tax gap being created.

Although, with governments that have already introduced 21 new taxes since 2000, there might be another yet undiscovered tax to come…. No one knows for certain what will happen, all we know is that something will need to be done as we move to an EV future.