Further evolution

Share this article

Rob Durrant-Walker considers the changes to note and action for both ‘old’ and ‘new’ patent box regimes

Key Points

What is the issue?

‘New’ regime claims have an R&D threshold to pass, and there is more onerous record keeping even for ‘old’ regime entrants.

What does it mean for me?

Your clients can still benefit from a 10% rate of corporation tax on qualifying profits on patented products or processes.

What can I take away?

Don’t overlook the potential value to your clients, and consider the time limits closely to capture all relief for the patent pending period.

Are you prepared for the Patent Box regime changes?

Patent Box potentially applies to any company with a qualifying patent. There are changes to note and action for both ‘old’ and ‘new’ regimes.

Qualification gives a company a reduced rate of corporation tax on its relevant profits arising from the patented income, and this is claimed on the company’s CT600 return as an additional deduction to arrive at an effective lower tax rate. As well as products themselves coming under a patent, it is possible for a process to be patented too, such as part of a manufacturer’s production process. In the latter case the ‘profit’ element arising from the production process can be quantified as the value of a notional royalty payment.

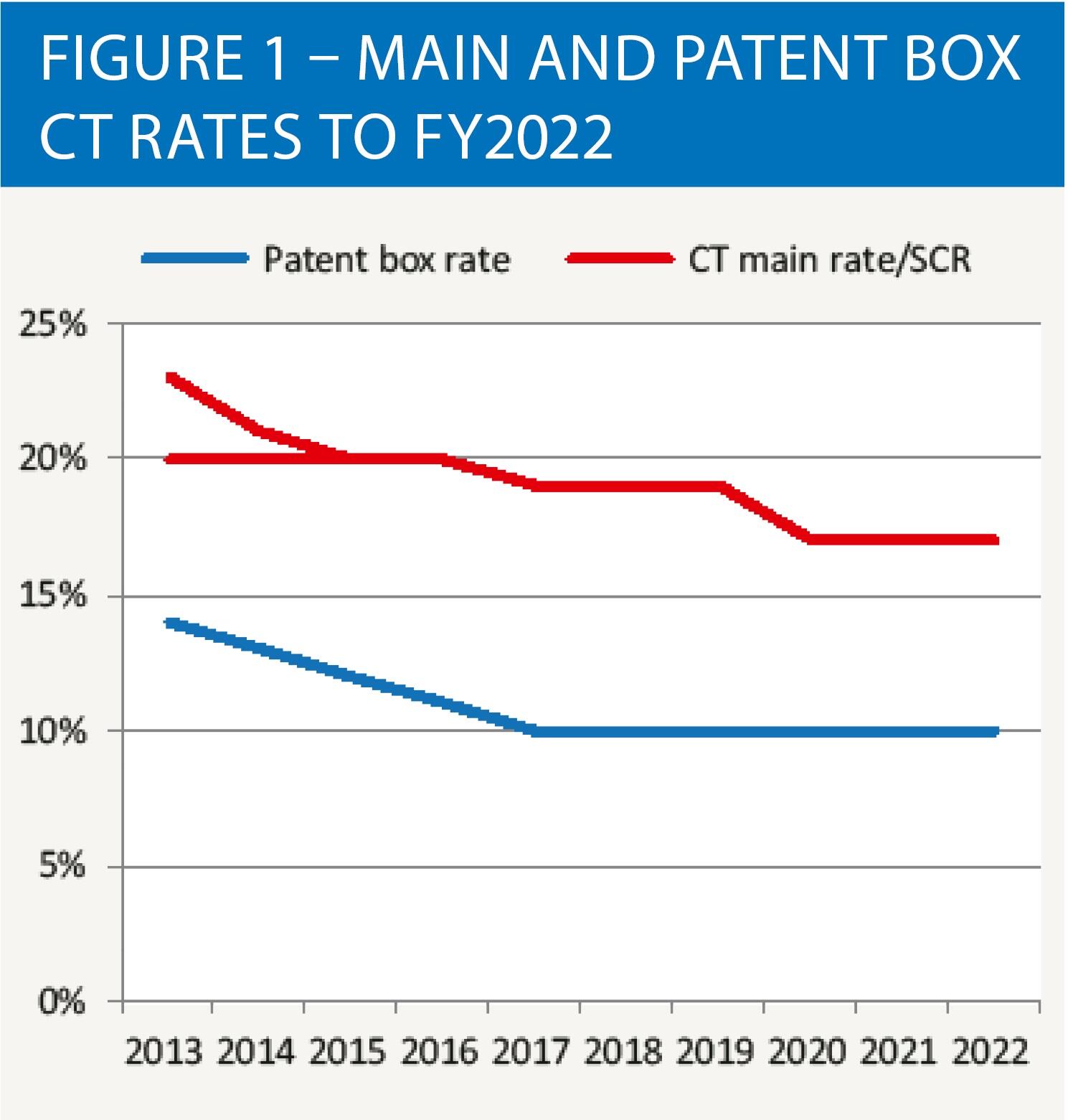

Patent Box commenced in April 2013, and the reduced rate of corporation tax which the regime offers is being gradually phased in towards the headline rate of 10% from April 2017. Figure 1 compares the Patent Box rate against the main rate and - up to the alignment of CT rates – the small companies’ rate of corporation tax.

Patent Box arrived during the previous Coalition government, but its inception is down to Gordon Brown’s tenure in the Treasury in the previous Labour government. The policy rationale was that UK plc lags far behind some of its key competitors – USA, Germany and Japan in particular – in patents registered per head of population. That’s not to say that the UK isn’t inventive, far from it. But, the UK has often lagged behind its competitors in the commercial exploitation of its inventiveness and it is that aspect which successive governments intend to help rectify with Patent Box.

Unlike Research & Development tax relief where the basic concept of qualification can be quite subjective – being based on an interpretation of what the advancement, relative state of knowledge, and development uncertainties are – Patent Box is largely black and white. In essence Have Patent = Qualify. As will be seen later on, even that relatively certainty though will become linked to R&D qualification in the ‘new’ Patent Box regime.

Some of the UK’s international competition also offer beneficial tax regimes for IP, and Patent Box was also an attempt to level the playing field with them. In fact the international competition felt that the UK has produced an overly benign regime, and this has led to changes to the UK Patent Box regime this summer. Although there were notable changes to the regime on 1 July 2016, Patent Box is alive and well and will continue for the foreseeable future. You should not overlook the benefit to your client of a 10% corporation tax rate on qualifying profits. Even though the differential with the main rate will have fallen to just 7% by 2019, it remains a substantial saving if the qualifying profits are high enough.

This article is about the changed Patent Box regime including its amendment by FB 2016 (clause 63 and Schedule 9, version 12 July 2016), and though Royal Assent is not expected until September the intended changes have been much signposted and are not expected to materially change now through the remaining Parliamentary process.

The changes to the existing regime – which internationally was deemed to be too beneficial in the UK – have been driven by the OECD, and not the EU, and therefore there is no obvious impact from Brexit.

Time management of elections

A key feature for advisers is going to be effective management of election time limits to capture relief for the patent pending period across both old and new regimes. No claim for relief can be made until the patent is granted – opting in at the right time allows the company to bring profits from the patent pending period into relief once the patent is granted.

For the old regime if there is at least a patent pending by 30 June 2016 on which to form the basis of an election, then opting into the old system will be beneficial in many cases. An election to ‘buy in’ to the old system until 2021 brings the benefits that claims in that period do not require a link to R&D, and it may maximise the claim amount to 2021 if there may otherwise have been a Patent Box/R&D nexus based restriction. However, unless there is a clear expectation that patented profits will have expired before 2021 and the benefit will lapse, then opting in won’t reduce the record keeping requirement as even for the old regime grandfathered claims from 2021 will still need to be made with reference to relevant R&D expenses from 1 July 2016.

An election does not necessarily need to have been made by 30 June 2016 and some advisers may be under a misapprehension that they have missed the deadline. HMRC’s ‘Patent Box: interim guidance on regime change’ at CIRD200160 is quite clear in respect of the timescale for the CTA 2010 s 357G election around the 1 July 2016 change to opt into the old system. HMRC say that ‘nor is there any requirement, if a company is not already elected in, to make an election by 30 June 2016 to ensure current assets are grandfathered. The two year time limit to make an election will still apply. For example as long as an accounting period straddles 30 June 2016 so part of it falls before that date any qualifying assets held on that date will be grandfathered as long as an election is made within two years of the end of the accounting period. For example: a company with an AP ending 31 December 2016 has until 31 December 2018 to make an election’.

Bearing in mind the potentially long timescales in some cases for a patent to reach grant from initial application, then even under the new regime it is important not to overlook the benefit of timely elections to capture any qualifying profits. Patent Box relief can only be applied once the patent has been granted, but does still apply to profits in previous accounting periods where the patent was pending and where a valid election is in place for that earlier period. Section 357CQ(7) allows such profits within the patent pending period of up to six years prior to then be relieved in the period of grant. It does not entail amending previous year’s corporation tax returns and HMRC’s example at CIRD220540 shows how the profits in the previous patent pending periods reduce the tax in the year of grant.

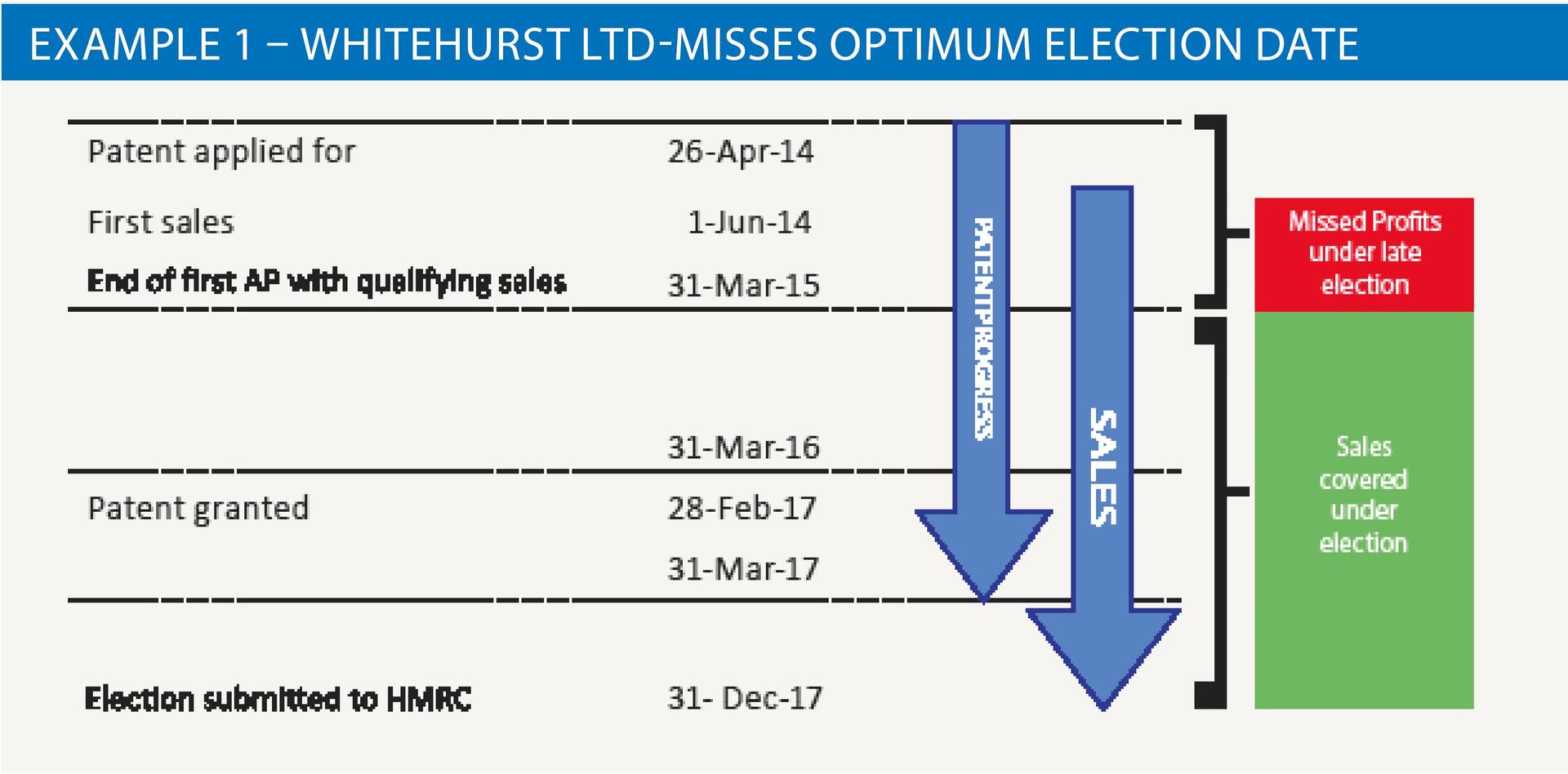

The usual two-year time limit applies from the end of the accounting period to elect in to the regime. In example 1 Whitehurst applies for a patent on 26 April 2014, with grant being made on 28 February 2017. Whitehurst’s advisor submits the Patent Box election to HMRC in December 2017 after learning from his client that the patent was granted. However, the December 2017 election is over two years after the year ended 31 March 2015 and that year is out of time limits when the adviser made the election. Whitehurst misses out on valuable tax savings relating to the period ended 31 March 2015 when sales had first started, as the company should have elected in by 31 March 2017 to bring in relief for the patent pending period profits.

A final word of warning though on the possibility of electing in too early – a Patent Box loss will need to be set off against Patent Box profits, so electing in too early can reduce the benefits. After all, profits in the early stages of exploiting IP can be elusive.

Link with R&D and record keeping

Post 30 June 2016, for Patent Box to be available there must be a link to qualifying R&D activity on the IP in the company. The usual R&D concepts and terminology apply. R&D is the proxy for the OECD’s ‘substantial activity’ requirement that the claimant company must have had in the development of the IP. The word ‘nexus’ is commonly used for the link, though it is not used within the legislation. The Patent Box-R&D nexus is through new s357BLA being the ‘R&D fraction’. For Patent Box this then is initially a gateway test that the development could have qualified for R&D. There is not even a requirement to make an R&D claim though of course the benefits of an R&D claim should also be considered.

The R&D fraction can only result in an unchanged or reduced Patent Box claim. There is a potential restriction where there is expenditure on acquiring the IP and/or subcontracted R&D to connected third parties – but the R&D fraction contains a helpful 30% uplift to in-house or unconnected third party R&D expenses which will counteract the drag from the non-qualifying expenses in many cases.

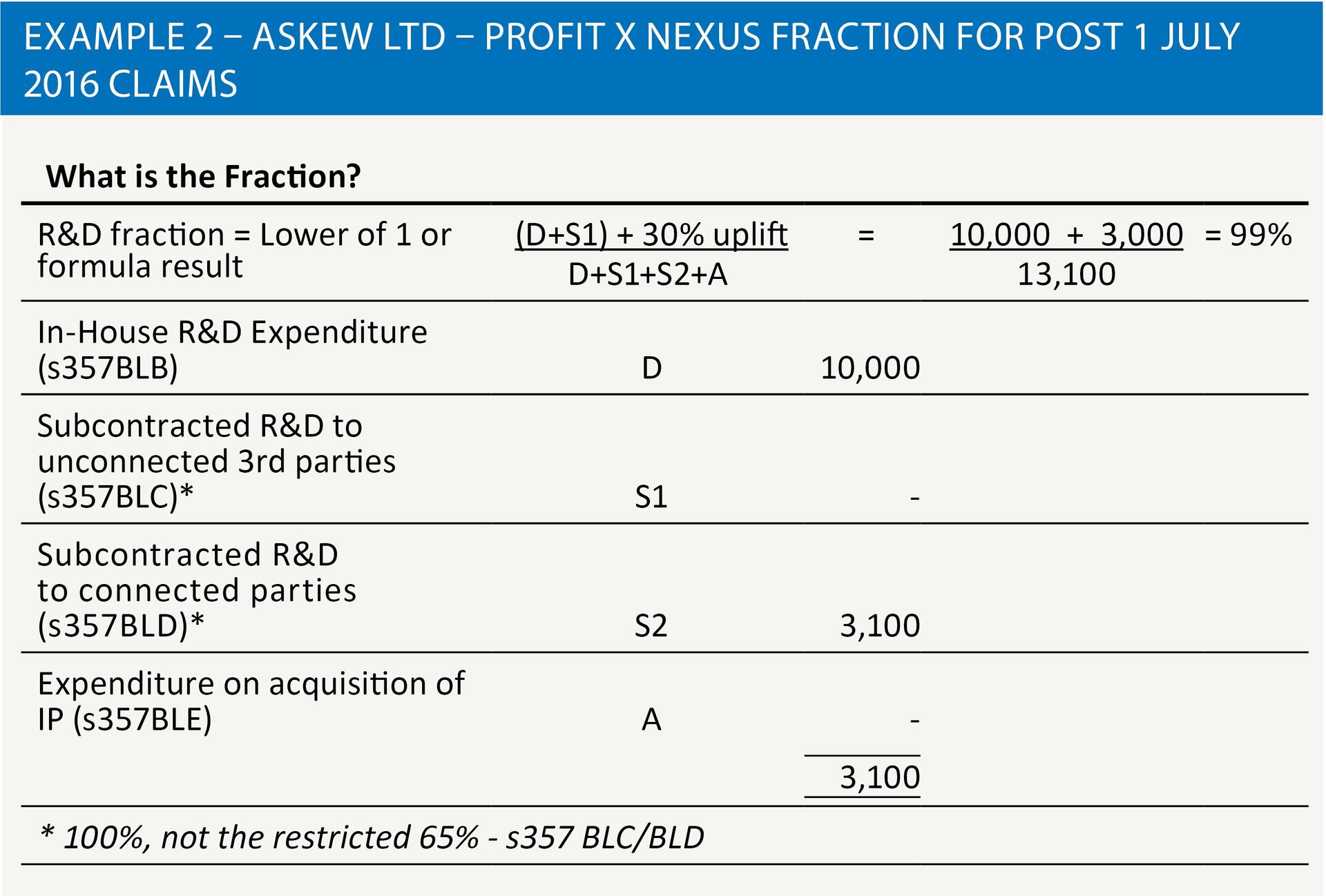

In example 2 for Askew Ltd, 23% of its relevant expenditure within the R&D fraction was subcontracted R&D to connected parties which prima facie would reduce its qualifying Patent Box claim. However, as its in-house expenditure gets the 30% uplift within the R&D fraction then the calculation in this case only restricts the qualifying Patent Box profit by 1%, to 99%.

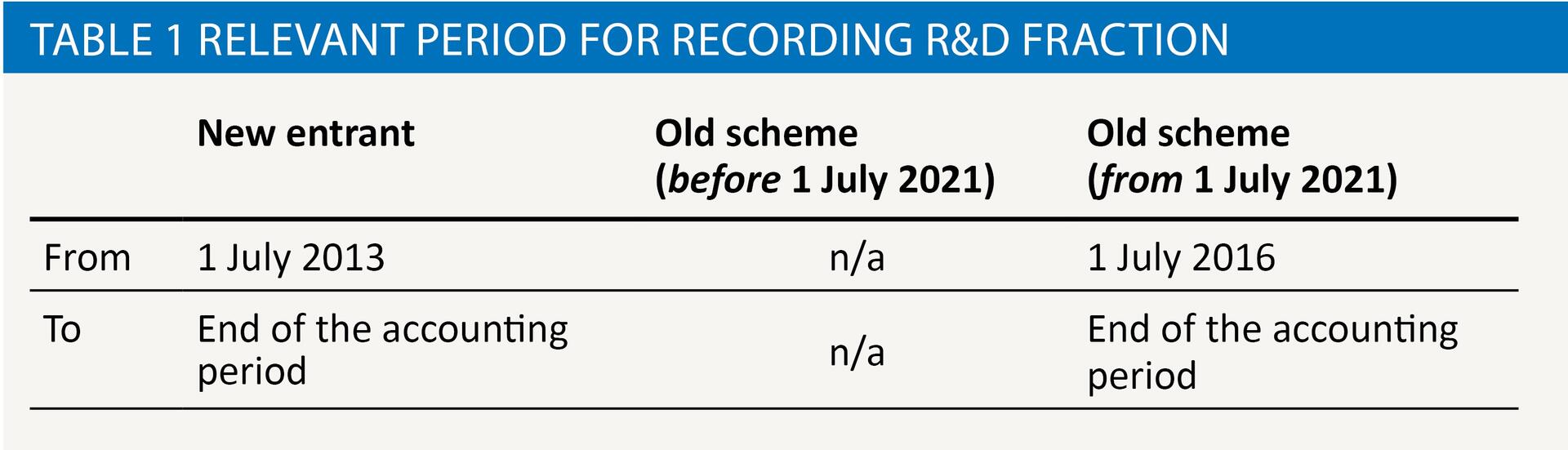

A record keeping commitment that needs to come with measuring the R&D fraction is to measure the cumulative impact of relevant expenditure on the R&D fraction over the relevant period. The cumulative period will always run up to the end of the current accounting period, but the start date will vary depending on whether the company starts under the old or new scheme. The relevant period for expenditure which is to be taken into account within each of s 357BLB – BLE is shown in table 1.

In addition, s 357BLF(2) allows the company to elect to use a start date for its R&D fraction up to 20 years before the last day of the current accounting period, even if it extends the relevant period to before 1 July 2013. An election would be beneficial if it produces a better R&D fraction, with the caveat that the company must have the analysis for those earlier periods to an appropriate level of detail.

Under the grandfathering provisions, old scheme members do not need to adjust for the R&D fraction until 2021. But they must nevertheless still keep a record of relevant expenditure from 1 July 2016 onwards as it will form part of their cumulative R&D fraction from 1 July 2021. It is quite possible that with multiple patents a company may have old and new regime IP.

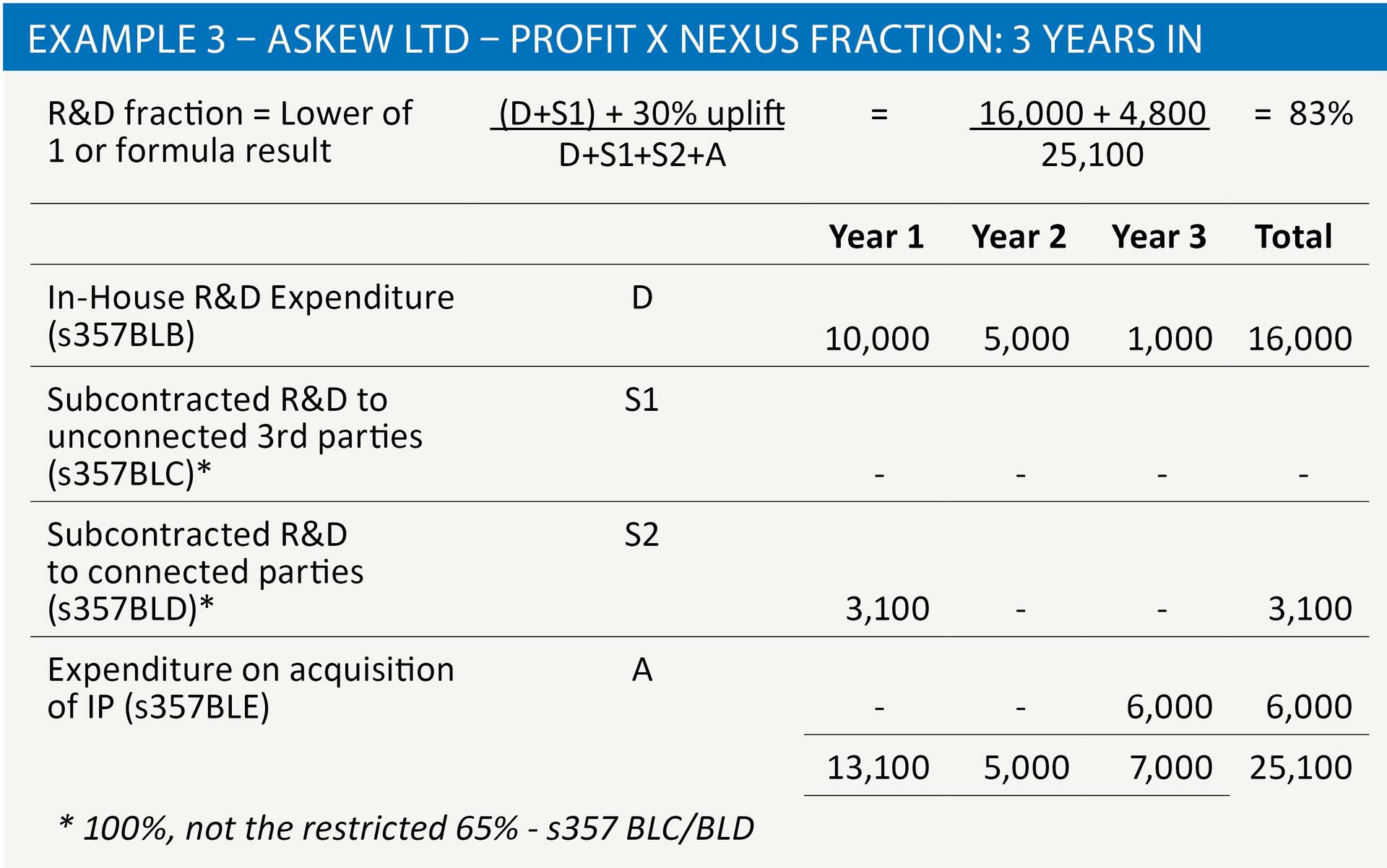

Example 3 shows the effect on Askew’s R&D fraction of relevant cumulative costs after three accounting periods. Askew has further R&D costs in years two and three, but £6,000 of that is IP acquisition cost and that has the effect of reducing the Nexus fraction to 83%. Previous years are not re-calculated, and the Nexus fraction of 83% is applied to the Patent Box calculation for that year’s accounting period only.

Now as it happens Askew has a number of patents. Potentially there may be a different Nexus fraction for each patent and Askew must track the relevant costs for each patent as far as reasonably possible. The same patent may give rise to a number of different products in the same product family. Client advice must be to keep pace with the principle that expenditure should be tracked cumulatively across time and across products in order to make claims more robust.

For ‘old’ regime members, the Nexus fraction will not affect them until June 2021. But their Nexus fraction from then will be based on the cumulative figures up to that point, so there is still action for old regime members to take to implement systems on their current accounting information from 1 July 2016.

Streaming, and group organisation of IP/R&D

Under the new regime, the option over which method of calculating the qualifying Patent Box profit (or ‘RIPI’) is gone and ‘streaming’ is mandatory. Each patented item (which for that matter can include a patented process in the production method with a notional royalty value) has a separate stream, with its own specific costs to be allocated to it.

The R&D fraction means that UK groups which split their IP ownership from their continuing R&D development on the same product family elsewhere in the group will find such a structure now works against them because of the impact of the ‘connected party’ rule of s357BLD, and so the structure should receive a careful review.

Conclusion

It is fair to mention that the commercial protection afforded by a patent is in the view of some SMEs counter-intuitive and many take the view that enforcing their rights over IP through a patent is at the same time volunteering dangerously to put their knowledge more conspicuously ‘out there’ in the first place.

The July 2016 Patent Box changes don’t make the regime any more beneficial – but the phasing in of the original regime by April 2017 now makes the full tantalising 10% rate a few months away.

The first release of Official Statistics on the Patent Box Relief will be published on 14 September 2016 for the 2013/14 tax year, and we will get a first taste of the initial take up, amounts claimed, and the number of claimant companies and a breakdown by company size and industry sector.