Intra-group transactions: the principles of transfer pricing

Share this article

We examine the principles of transfer pricing and the basis upon which the taxable profits of multinational enterprises are determined.

Key Points

What is the issue?

Multinational enterprises are able to sell goods and provide services from one company to another within the same group. To facilitate the provision of these goods and services among members of the same group, the companies set up transfer prices.

What does it mean for me?

Different tax authorities seek to ensure that the amount of taxable profit of a company in their jurisdiction represents the appropriate amount of profit and that multinational enterprises do not transfer profit to low tax jurisdictions to minimise their tax liability.

What can I take away?

Most tax authorities require transfer prices between associated enterprises to be equivalent to what the prices would have been in the open market and in similar circumstances were the companies not related; i.e. arm’s length price.

International trade, technological advancement and integration of national economies have enabled the growth of cross border operations, with companies forming groups and setting up structures in different countries. These groups of companies, multinational enterprises (MNEs), vary in size and operate cross-border using structures such as incorporating subsidiaries, operating through branches, joint ventures or partnerships. MNEs are able to sell goods and provide services from one company within the group or regional centre to another company within the same group.

A substantial volume of global trade consists of international transfers of goods, services, capital (money) and intangible assets among members of the same group (i.e. intra-group transactions). There is evidence that intra-group trade arguably accounts for more than 30% of all international transactions (see The UN Manual on Transfer Pricing for Developing Countries at tinyurl.com/6dhmwe4p).

What is transfer pricing?

To facilitate the provision of these goods and services among members of the same group, companies typically set up transfer prices. Transfer price is the price charged for goods and services between members of the same group (also referred to as related parties or associated companies/enterprises). Transfer price is also used to refer to the price that a business or division within a company charges for goods or services provided to another within the same company.

Companies are related or associated with each other directly or indirectly if one company controls the other, or both are controlled by the same person or persons. What constitutes direct and indirect control is defined in each country’s tax laws; generally, however, direct control is where a company determines how the affairs of another company are conducted because of the shareholding, voting rights or any powers within the articles of association or other document regulating the company. Indirect control exists where rights and powers are held by another company or person connected to the company in question.

As you will see, transfer pricing is important as the need to set such prices is a normal aspect of how MNEs must operate, whether different companies are transacting with one another, or transfers are being made between divisions in the same company.

Transfer prices may also be used to evaluate the performance of divisions and companies. Divisions within a company and group companies within an MNE will generally have separate profit centres and transfer prices can help to determine individual profitability. For example, a business manager, say in the manufacturing division in a company requiring components for use in production, will wish to buy the components at the best price to maximise the division’s profitability. Similarly, the sales manager in the same group will wish to sell its components at the best price possible.

For decades, international tax rules have required that group members use arm’s length transfer prices – the price at which a third party would buy or sell the relevant goods or services. Without this requirement, groups could manipulate where their profits were recorded and thus taxed.

Why is there focus on transfer pricing?

Transfer pricing is thus a legal requirement in almost all countries and jurisdictions. Without this requirement, MNEs could achieve outcomes which are not consistent with their economic substance; e.g. shifting profits to a low/no tax country or jurisdiction.

Example: Manufacturing Group

A manufacturing group has a parent company in the UK with two 100% owned subsidiaries, Manufacturing Co in China and Sales Co in Ireland.

Manufacturing Co manufactures the product which it sells to Sales Co. The transfer price between the two companies is paid by Sales Co. Sales Co then sells the product worldwide to third party customers at market price.

Manufacturing Co in China has a tax rate of 25% and Sales Co in Ireland has a tax rate of 12.5%. The transfer price between Manufacturing Co and Sales Co affects the profits left in each country and in turn the effective tax rate for the Group. If Manufacturing Co sells to Sales Co at an unrealistically low price, more profits could be taxed in Ireland at a lower rate.

To address and prevent MNEs shifting profits, the arm’s length principle is established as the agreed approach for an appropriate transfer price. This is typically set out in the domestic legislation of most countries and in their double tax treaties.

Guidance to determine the appropriate transfer price

Guidance on the determination of the appropriate transfer price originates from the tax treaties. Countries and jurisdictions bound by the tax treaty agreements are referred to as ‘states’.

Tax treaties are agreements between two states designed to protect against the risk of double taxation, provide certainty of treatment for cross-border trade and prevent discrimination. Most tax treaties largely conform to the OECD Model Tax Convention on Income and on Capital (OECD Model); some instead use the United Nations Model Double Taxation Convention between Developed and Developing Countries (UN Model) as their base. The Model Conventions are intended to facilitate the negotiation of bilateral tax treaties. Guidance and explanatory notes attached to the Model convention help with interpretation, as well as setting out specific reservations from individual countries. A few countries have their own Model; the United States is the best example.

The UN Model is consistent with the OECD Model, except that the UN Model favours greater taxing rights to the host country of investment; i.e. the country where the income is sourced compared to the residence country of the investor.

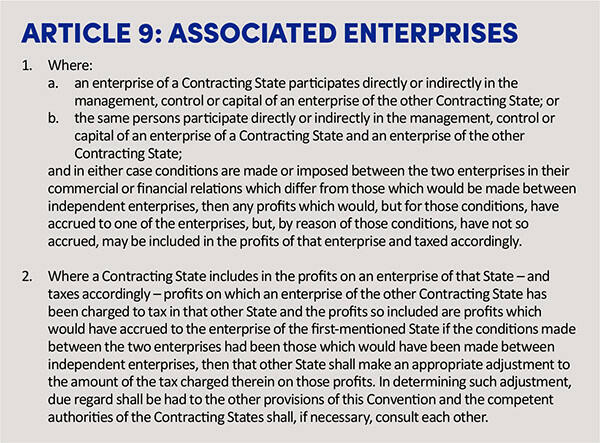

The appropriate transfer price is price based on the arm’s length principle, which represents the internationally agreed methodology of how transfer prices for MNEs intra-group transactions should be applied. The arm’s length principle covers all types of intra-group transactions, including (but not limited to): goods, services, intangible properties, financial transactions and business restructurings. (A country’s tax legislation will specify the types of transactions for which transfer pricing and the arm’s length principle applies.) The arm’s length principle is expressed in Article 9 of the OECD Model. There are other articles embodying the arm’s length principles and these are Articles 7, 11 and 12 of the OECD Model (and 12A of the UN Model, which is especially relevant to services).

Including an Associated Enterprise clause in a double tax treaty is important, as jurisdictions could disagree on how much should be taxed in each location. In our example, both China and Ireland have an interest in the profits taxed in each country. The double tax treaty should regulate that, as well as including a clause on resolving disputes. Without effective dispute resolution, multinational groups could face effective double taxation.

See Article 9 of the OECD Model below. Paragraph 1 establishes when there is a special relationship between two enterprises. In such a case, transactions between the enterprises not consistent with what would be observed between independent parties (i.e. not arm’s length) may be adjusted (increased) to reflect profits which should arise at arm’s length. Paragraph 2 provides for a corresponding adjustment by the other country where an adjustment has been made to the profits of the enterprise in a country to reflect an arm’s length situation, to avoid economic double taxation.

The conditions for the application of this article are set out in the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations (OECD Guidelines). There is also a United Nations Practical Manual on Transfer Pricing for Developing Countries (UN Manual). The UN Manual builds on the OECD Guidelines and is drafted to assist developing countries in applying the arm’s length principle. The OECD Transfer Pricing Guidelines are the most commonly used and are periodically revised – with the biggest recent change taking place after the outcome of the base erosion and profit shifting (BEPS) project.

Transfer pricing methods

The OECD guidelines set out transfer pricing methods which provide ways to set transfer prices that are arm’s length, or test the transfer price already in place, as to whether this is arm’s length. The way this works is that a transfer pricing method is identified as the most appropriate method; and that method is then the mechanism by which the prices or results of the transactions between related parties are compared to those of third parties in comparable situation. In many cases, there is no direct third-party comparison, so alternative approaches are needed to find an appropriate method.

Prior to identifying the most appropriate transfer pricing method, a functional analysis needs to be performed to accurately understand:

- the transaction;

- the functions which parties to the transaction perform with respect to the transaction;

- the economically significant risks that may arise on the transaction;

- which parties bear the risks and how the risks are managed; and

- the assets owned or used by the parties for the transaction.

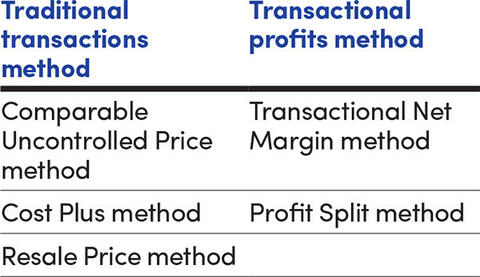

There are five OECD recognised transfer pricing methods, divided into two categories as shown below.

Transfer pricing methods

In addition to these five methods, the UN Manual includes a ‘Sixth method’ (or ‘Commodity rule’).

The traditional methods are referred to in this way as the methods in the category rely on actual transactions, and directly compare the terms and conditions in the related party transaction(s) with those of third parties in comparable transactions.

The transactional methods, on the other hand, are less direct than the traditional method and rely on profit levels to determine arm’s length prices, measuring the net operating profits of related party transaction(s) and comparing this to that of independent companies engaged in similar or comparable transactions.

Each of the methods is briefly discussed in turn below.

Comparable Uncontrolled Price method

The Comparable Uncontrolled Price method compares the price charged for goods or services in a related party transaction to that charged in a comparable third party transaction in comparable circumstances (i.e. market price). This may be to compare the related party transaction to its transaction with third parties in comparable circumstances (internal Comparable Uncontrolled Price) or a comparison of two (or more) third party transactions which are comparable to the related party transaction (external Comparable Uncontrolled Price).

Resale Price method

The Resale Price method, also referred to as resale minus, is used in sales and distribution transactions. The method considers the price an item is ‘resold’ in a transaction when determining an arm’s length price. The method establishes an arm’s length gross margin from an entity’s sales to third parties, and then uses the gross margin to determine the arm’s length price in the entity’s transaction with its related parties. (Gross profit is net sales less cost of goods sold. Gross margin is gross profit divided by net sales (expressed in percentage).)

Cost Plus method

The Cost Plus method analyses a controlled transaction taking place between two entities; usually, a supplier of property or services and the related party purchaser. An arm’s length price is then determined by reference to an arm’s length gross mark-up (or the average of a range of arm’s length gross mark-up) earned on the direct and indirect costs in the related party transaction. (Mark-up is the gross profit / cost of goods sold.)

Transactional Net Margin method

The Transactional Net Margin method assesses the arm’s length nature of a related party transaction by determining the net profit of the transaction relative to an appropriate base (e.g. cost, sales or assets), and comparing this to those of independent parties performing similar transactions. The ratio of net profit to an appropriate base is known as profit level indicator. There are several profit level indicators that can be used to apply the Transactional Net Margin method, making it appropriate to use for a wide range of transactions. Some of the profit indicators provided in the OECD guidelines are:

- net profit weighted to sales / operating margin;

- net profit weighted to costs / markup on total cost / total cost markup;

- net profit weighted to assets / return on assets; and

- the Berry Ratio, being gross profit divided by operating expenses.

The Profit Split method

The Profit Split Method is arguably the most complex of the five OECD transfer pricing methods. This method first identifies the profits of related parties from a controlled transaction and splits the profits between the parties to arrive at the profits each party would have made in an arm’s length situation. The profits are split based on the value of the contributions of each party.

The ‘Commodity rule’

The Commodity rule has some similarity with the Comparable Uncontrolled Price method, and some countries use this method as an imperfect application of that method. It is used for commodities transactions and relies on the quoted prices on the commodities market to price commodity transactions between related parties.

Transfer pricing documentation

The application of the transfer pricing methods and determination of the transfer prices are to be described in a transfer pricing documentation. The BEPS project included specific new requirements for transfer pricing documentation, now in the OECD guidelines, which set out a three‑tiered standardised approach to transfer pricing documentation:

- Masterfile: This provides high-level information on an MNE group, including an overview of the group’s business, the global allocation of income and economic activity and the transfer pricing policies.

- Local File: This supplements the Masterfile and is a detailed transfer pricing documentation specific to each country, setting out details of the material related party transactions.

- Country by Country Report: This requires specific information (such as revenue, profit before income tax, income tax paid and accrued, and number of employees) to be provided by MNEs with annual consolidated group revenue of €750 million, to allow tax authorities to perform risk assessments on the MNE group. This report is normally sent to the tax authority in the headquarter location, which in turn forwards it to other tax authorities where the countries are party to Multilateral Competent Authority Agreement on Exchange of Country by Country Report, a Tax Information Exchange Agreement or other suitable bilateral tax treaty.

Mutual agreement procedure

Although the OECD guidelines and UN Manual describe the methods and approaches to determining arm’s length prices, disagreements do occur between tax authorities and MNEs (taxpayer) over the most appropriate transfer pricing method or, in fact, the arm’s length price. These disputes may lead to double taxation.

In order to resolve these disputes and to reduce double taxation, tax treaties contain an article, the Mutual Agreement Procedure, to address and resolve disputes between tax authorities. The Mutual Agreement Procedure is also used where the tax outcomes to a person or entity from the actions of tax administration will result in taxation not in accordance with the provisions of the tax treaty.

Conclusion

The transfer price important for both companies and tax authorities. Transfer prices determine the taxable profits of MNEs in different tax jurisdictions and are required to compliant with tax laws.

The arm’s length principle is the accepted approach to establish an acceptable transfer price between different companies and divisions within a multinational group. Intragroup transactions are compared to transactions between independent companies in comparable circumstances to determine acceptable transfer prices. Thus, the open market comprising independent companies is the benchmark for assessing the acceptability of the transfer prices.

Double tax treaties set out the ground rules for determining arm’s length prices and they also include vital dispute resolution approaches. The OECD Transfer Pricing Guidelines (or the UN Manual for developing countries) set out the approaches to be adopted by MNEs and tax authorities. The BEPS Inclusive Framework of approaches to transfer pricing, documentation and dispute resolution has set the future ground rules.

Further reading

The OECD Model Tax Convention: tinyurl.com/3cav5a8v

The OECD Transfer Pricing Guidelines: tinyurl.com/5sk9bm4s

The UN Model Tax Convention: tinyurl.com/59f6seb6

The UN Transfer Pricing Guidelines: tinyurl.com/6dhmwe4p