More change

Share this article

Tony Bacon considers the major challenges faced by pension scheme members, their advisers and employers after recent radical Budgets

Key Points

What is the issue?

Freedom and choice, death tax reform and changes to allowances are transforming taxation of pensions

What does it mean to me?

Tax professionals need to be aware of these changes because they may have significant unexpected consequences and opportunities

What can I take away?

There is likely to be greater demand for tax advice on pensions

Pensions tax is undergoing a generational transformation after recent radical Budgets. With it come challenges for scheme members, their advisers and employers.

Defined contribution ‘freedom and choice’

The freedom to cash out defined contribution (DC) assets after age 55, subject to paying marginal rate income tax, is a huge change to the UK pension system. There are big tax issues involved as more individuals use drawdown. In advising on whether, how much or when to draw down from a pension scheme under the new flexibilities, it is important to think holistically and take into account the member’s other assets. Tax band planning opportunities – and risks – abound.

Together with concurrent death tax reforms, conventional wisdom is being turned on its head. Most unused DC funds, including in drawdown, can now be paid tax-free on death before age 75; on death after age 75 they are subject to the recipient’s marginal income tax rate that is perhaps much lower than the original saver’s. And it is now possible for DC pension funds to be inherited by anyone.

So the old rule of thumb was ‘use your pension for income (because you have to) and treat your house as a family asset (because you like living in it, but recognise that inheritance tax is an increasing risk, given rising property prices)’. The new rules might become ‘use your house for income (thereby reducing the likelihood it suffers inheritance tax) and treat your pension as a family asset (because you can and because it may be free of all tax if you do so)’.

Members with defined benefit (DB) pension rights may be tempted to transfer benefits to DC schemes to access the new flexibilities, a huge advice challenge in itself. A tax adviser would note that the reshape may well entail more lifetime allowance charge – but there may still be reasons to proceed.

Summer Budget moves the goalposts again

The July Budget brought three more important changes. Two of these come into force on 6 April 2016, having immediate impact.

Lifetime allowance reduces again

The lifetime allowance (LTA) will reduce from £1.25 million to £1 million from 6 April 2016 (increasing with CPI from 2018).

Pension savings are tested against the LTA (usually when put into payment) and extra tax is chargeable to the extent that the LTA is exceeded. Broadly, for an individual normally subject to 40% income tax in retirement, in effect 55% tax is charged instead, on the benefits in excess of the LTA.

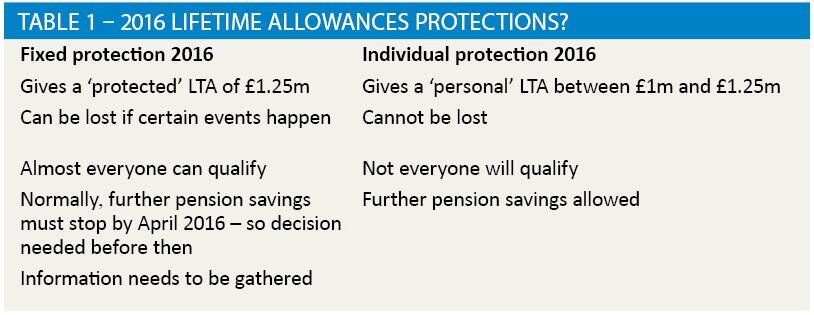

If no mitigating action is taken the tax bill can be significant: an individual with large pension savings could face additional tax of up to about £60,000. Thankfully, there will be protections available to members who have already built up large pension savings to avoid retrospective taxation. The government has confirmed they will be similar to the protections offered with the 2014 LTA drop – so we assume the main features will be as set out in Table 1.

Unlike the 2014 protections, there will not be a deadline for applying for these – at the time of writing we wait to hear the process. But 6 April 2016 is still a key deadline for decisions and actions, especially around stopping pension saving.

With the LTA reduced to £1 million it is unsafe to assume that only high earners are affected. Individuals on middle incomes with long service in a DB scheme might now have the problem of planning around the LA.

Tapered annual allowance

Pension savings totalling more than the £40,000 annual allowance (AA) will incur an extra tax charge payable upfront. Pension savings include the value HMRC placed on a pension earned in a DB scheme, and any DC contributions made by the member or their employer. Broadly, the charge is income tax at the member’s marginal rate. Because pensions are subject to income tax when paid, the savings above the AA are subject to double taxation. Unused AA for the previous three years can be carried forward.

An income-based taper, supposedly to finance the new inheritance tax reliefs, is to be applied to the AA so that those with adjusted income of more than £210,000 a year have an AA of only £10,000. See Table 2.

This test to determine the available allowance in a tax year is not as simple as it appears. The first step is to identify threshold income. This is all income assessable to income tax minus relievable pension contributions made by the member and any charitable payroll giving. If threshold income for the tax year does not exceed £110,000, no further action is required and the member’s AA for the tax year is £40,000. If threshold income does exceed £110,000, adjusted income must be assessed to identify the AA to be applied. In essence, adjusted income is the threshold income with any pension savings, whether paid for by employer or employee, added on.

Most people may know in advance their salary for their tax year, but many will have no idea about potentially large unpredictable elements like bonuses and outside earnings such as investment returns, rental income and taxable income from pensions. Such elements can complicate the planning in maximising the use of a tax year’s AA.

The outcomes are not always intuitive, as Table 3 illustrates. Individuals with similar pay and pension provision can have different AAs.

At present we know little about how HMRC intend to operate the regime in practice. But we do know that employers and schemes will have some decisions to make, such as whether or when to provide an alternative to employer pension contributions and how much help to offer (or advice to pay for) to understand and plan for the tax.

Individuals still accruing DB benefits may decide to take the new additional AA charge on the chin – not least because the charge is lower for DB than its headline rate suggests. Benefit accrual might be worth considerably more than the £16:£1 a year value used by HMRC to value DB to assess the charge. And using a ‘scheme pays’ facility helps. Under this, the scheme pays the tax charge up front to HMRC, reducing the member’s retirement benefit to pay for it. This will ease cash flow for the member – there is no need to pay tax up front – and if the scheme claws back the tax from benefits that would be subject to income tax when they are eventually paid, that’s less tax to settle later.

And some immediate change to make this work…

Until the Budget, pension accrual and savings were tested against the AA usually over a 12-month period called the ‘pension input period’ (PIP), which could be the tax year. Not now. To facilitate the tapered AA measure, all PIPs will be aligned to tax years from 2016/17.

To get there, 2015/16 has complex transitional arrangements. For many, this may herald an opportunity for higher pension savings in 2015/16 (or carried forward), but the calculation is complex and is rarely as much as the £80,000 described in some headlines. Advisers in this space, especially if considering the DB provisions, are advised to get out the wet towel.

The changes in the summer Budget may signal the end of the road for pensions for high earners. Our research indicates an increasing trend to offer cash rather than pensions at senior levels.

Consulation for more change

On top of this, the Chancellor announced a root and branch review of the principles of pension taxation. He floated the idea of moving from exempt contributions, exempt investment income and capital gains of the pension institution, so everything may change again soon.