The right path

Share this article

Stephanie Parker and Robert Pullen consider the challenges presented by clients wishing to reduce their IHT exposure by making gifts

Key Points

What is the issue?

The vast majority of clients wish to reduce their inheritance tax exposure but making large gifts can present a variety of tax and other challenges.

What does it mean to me?

Clients need to be aware of the different ways they can structure their gifts, the potential tax consequences of future events and how any resulting tax liabilities will be funded.

What can I take away?

There is no single strategy that will suit all, but trusts should always be considered when gifting. Even with an upfront inheritance tax charge significant savings can still be made in the right circumstances.

Making gifts is a simple way to reduce a taxable estate and mitigate an otherwise inevitable inheritance tax bill. Although the major changes to the tax treatment of trusts in Finance Act 2006 curtailed trust-based planning to a certain extent, there are still situations when gifting via a trust could be a viable option.

The most appropriate gifting strategy for an individual will depend on a number of factors. The type of asset, the value, the recipient’s situation and the donor’s health will all need to be considered and should influence the form the gift takes if potential tax exposures are to be minimised. Considered below is a particular situation which could be approached in a number of ways with differing results.

Case scenario

Margaret owns a rental property worth £900,000. Margaret inherited the property from her Aunt many years ago and the base cost is £150,000. Margaret does not need the income from the property and she wishes to use the property to benefit her grandchildren.

Options

Option 1: gifts out of income

Margaret continues to own the property but uses the net income after tax to contribute to the school fees. She leaves the property to the grandchildren in her will.

- Margaret continues to pay income tax on the rental income received at her marginal rates of income tax.

- The lifetime gifts to the grandchildren will be exempt from inheritance tax under s21 IHTA 1984 provided the gifts are covered by excess income and follow a regular pattern.

- The value of the property will be subject to inheritance tax on Margaret’s death. This could be up to £600,000 based on current values if the bequest is made free of tax as grossing up would be required.

- The grandchildren inherit the property with a base cost equal to their share of the probate value of the property.

- After inheriting the property, the grandchildren may be subject to the additional 3% rate of Stamp Duty Land Tax if they purchase another property whilst still owning a share of the let property, subject to the special treatment for inherited properties.

Option 2: bare trust

Margaret transfers the property into a bare trust for the benefit of her grandchildren. The income is used to pay for their school fees.

- Margaret faces a charge to capital gains tax on the deemed gain arising on the gift of the property. The gain chargeable is £750,000 (although a discount on current market value may be appropriate as Margaret is gifting part shares of the property) and the tax due at 28% is £210,000 (ignoring annual exemptions). Margaret would have the option to pay this tax in instalments over 10 years, with interest, s281 TCGA 1992.

- If Margaret dies within seven years of making the gift, the transfer will become chargeable to inheritance tax and the recipients will face a tax charge of up to 40% of the value at the date of the gift, subject to tapering relief and any available nil rate band.

- The grandchildren will be assessable on their share of the rental income which hopefully falls within their own income tax personal allowances.

- If the property is sold, the grandchildren will be subject to capital gains tax on their share of the property. The grandchildren can utilise their annual exemptions and they may be subject to lower rates of capital gains tax.

- The grandchildren will be subject to the additional 3% rate of Stamp Duty Land Tax if they purchase another property whilst still owning a share of the let property.

- There could be significant control issues as the children reach the age of majority with the grandchildren having different views to each other and the bare trustees.

- Margaret must decide who is to benefit now and their share will be fixed. Future grandchildren would not be able to benefit from the gift.

Option 3: gift into trust

Margaret transfers the property into a discretionary trust and the rental income is used to pay school fees.

- A settlement of the property into a discretionary trust will incur an upfront inheritance tax charge. This tax charge, if paid by the trustees, can be paid in instalments over ten years, subject to interest, under s227 IHTA 1984. If the trust does not have liquid funds, Margaret could make further gifts to the trust out of her income to fund the payment of the inheritance tax by instalments by the trustees.

- The trustees will be subject to inheritance tax charges at ten year anniversaries and when capital distributions are made.

- Margaret can elect to holdover the capital gain crystallising on the gift under s260 TCGA 1992. This means that Margaret can avoid the large capital gains tax bill and tax is deferred until the trustees sell the property.

- The trustees will be subject to income tax at the highest rates, but if distributions are regularly made to the beneficiaries, the beneficiaries can claim tax repayments to boost the income available for their school fees.

- If the property is sold by the trustees, capital gains tax will be payable at the highest rate. However, the trustees have the ability to holdover gains on transfers of assets out of the trust so the property could be transferred to the beneficiaries prior to sale in order to make use of each of their annual exemptions and lower tax rates.

- Margaret can retain control of the property by remaining a trustee with at least one other. The class of beneficiaries can be drawn to include existing and future grandchildren and future generations if desired. The benefits provided to any individual beneficiary remain at the discretion of the trustees and no individual has a fixed interest or entitlement to the trust income and capital during the trust period.

- Income can be accumulated by the trustees to provide capital to fund the inheritance tax arising on the transfer.

10 year planning

To fully evaluate the impact of the different options, consider the following scenario.

- The property yields £50,000 rental income, after expenses, for each of the next ten years.

- Margaret is a higher rate taxpayer.

- Margaret’s five grandchildren have no other income or gains in each of the next ten years.

- The property is sold in 2027 by the grandchildren for £1.1 million.

- Margaret (or her estate) bears all of the inheritance tax.

- CGT Annual exemption in 2027 is £11,500.

- Basic rate tax band in 2027 is £40,000.

- Margaret has already utilised her nil rate band.

Option 1: gifts out of income

Margaret gifts the net income after tax of £30,000 to the grandchildren each year. The property is left equally between her five grandchildren on her death. Table 1 shows the impact of tax if she dies in 2018 when the property is still worth £900,000, in four years in 2021 when the property is worth £1 million and in ten years in 2027 when the property is worth £1.1 million.

Option 2: Bare trust

Margaret declares a bare trust over the property in favour of her five grandchildren absolutely in equal shares. See table 2.

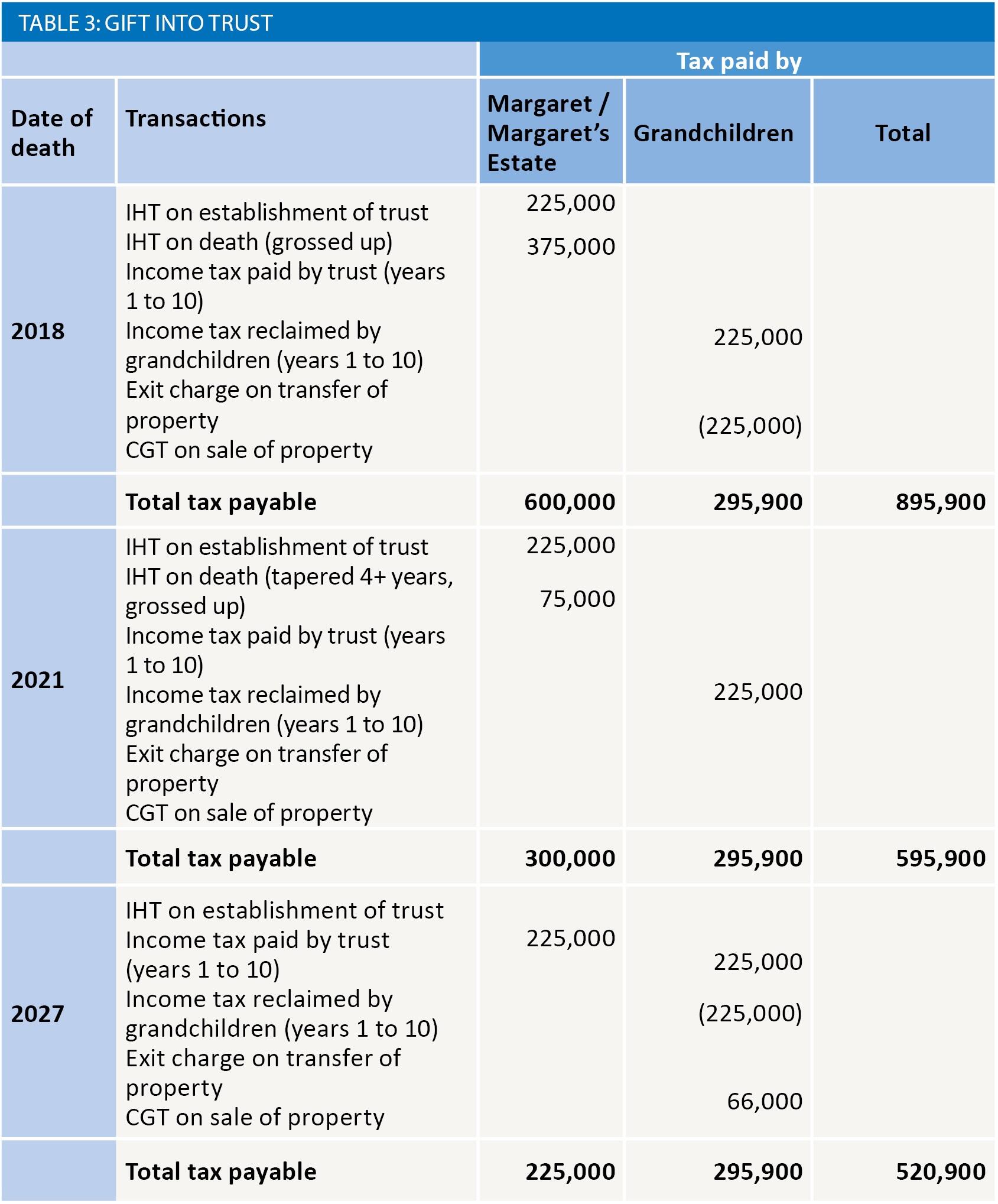

Option 3: Gift into trust

Margaret transfers the property into a discretionary trust for her existing and any future grandchildren and pays the IHT on the transfer. She and the trustees claim holdover relief on the gain arising on the transfer to the trust. The trustees distribute the property to the beneficiaries shortly before the sale in 2027 and again claim holdover relief under s260 TCGA 1992. See table 3.

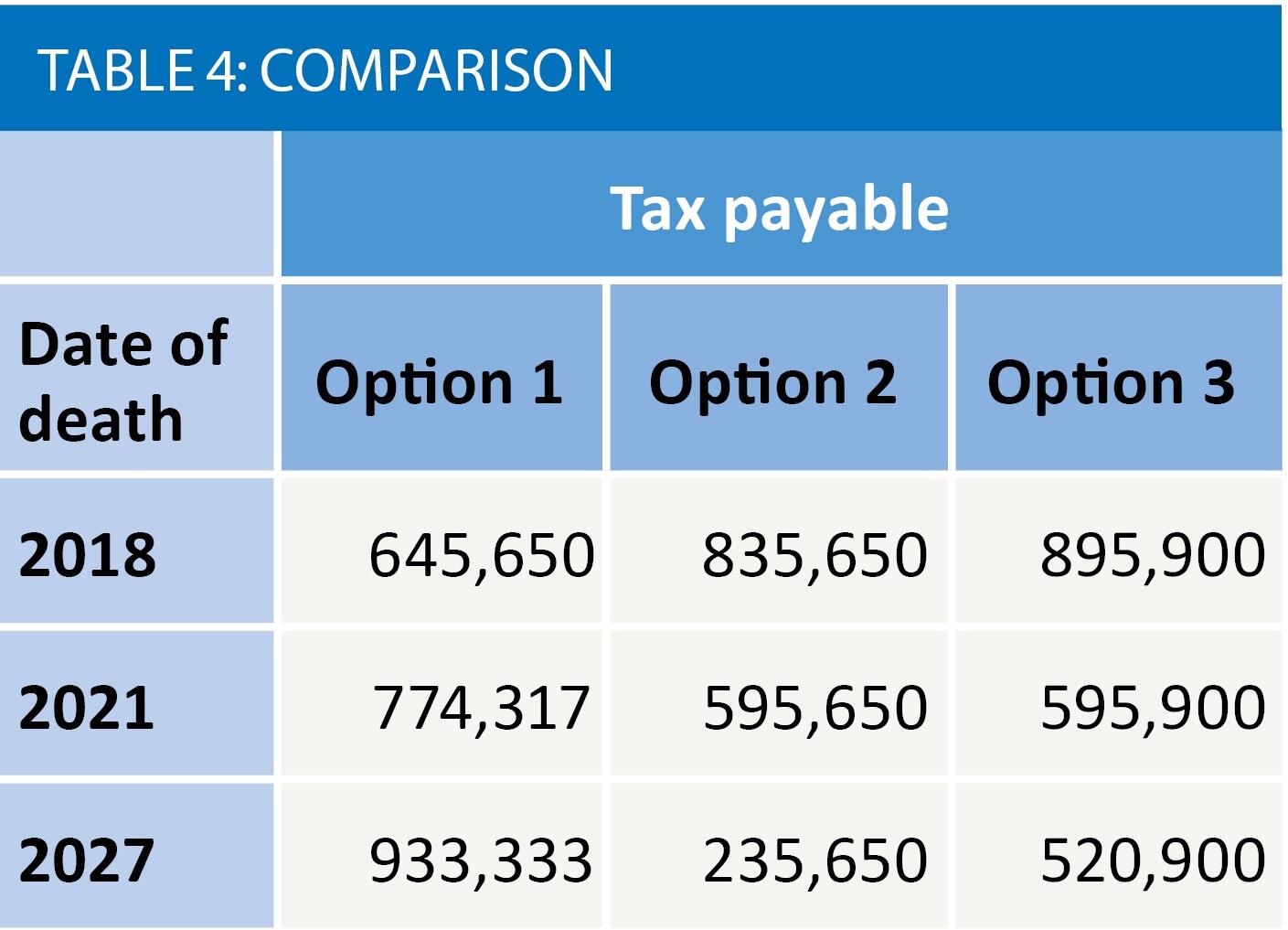

Comparison of tax payable

As can be seen from the following summary, the total tax payable differs widely depending upon the particular circumstances.

Although option 2 can provide a simple and tax efficient route, many families will not be comfortable with the lack of control and the non-tax problems it may bring. Option 3 creates a more beneficial outcome over option 1 once the donor has survived more than three years and tapering relief becomes available. Further, if the full nil rate band is available, option 3 can be even more tax efficient. Further tax savings can also be made if the trustees bear the tax rather than Margaret. With these possibilities lifetime settlements should never be ruled out as an option and can provide a practical solution to estate planning conundrums.