Scottish taxes: the progress of continuing devolution

Share this article

We consider the range of tax powers devolved to Scotland, the 2024/25 Scottish Budget proposals, and the progress of continuing devolution of taxes.

Key Points

What is the issue?

This article outlines the range of tax powers devolved to Scotland, the 2024/25 Scottish Budget proposals, the wider funding package of which Scottish taxation is a part, the progress with the devolution of taxes and recommendations put forward to build a better tax system in Scotland.

What does it mean to me?

‘Scottish taxes’ can be grouped under three broad categories, reflecting the varying degrees of control that the Scottish Parliament has over each: fully devolved, partially devolved and assigned taxes.

What can I take away?

Scottish income tax is now well established, as are the land and buildings transaction tax and the Scottish landfill tax. However, other Scottish taxes are at varying stages of implementation, including aggregates tax, air departure tax, VAT and local taxes.

This article outlines the range of tax powers devolved to Scotland, the 2024/25 Scottish Budget proposals, the wider funding package of which Scottish taxation is a part, progress (or otherwise) with the devolution of taxes that are not yet implemented, and recommendations that CIOT and ICAS have recently put forward to build a better tax system in Scotland.

Background

It is nearly ten years since the independence referendum of September 2014 led to the creation of the Smith Commission, which proposed the devolution of additional powers to the Scottish Parliament (see tinyurl.com/5dfx98uh). The Commission made a number of fiscal recommendations aimed atstrengthening the financial responsibility of the Scottish Parliament. These were enacted in the Scotland Act 2016, building on the tax powers devolved by the Scotland Acts of 1998 and 2012.

‘Scottish taxes’ can be grouped under three broad categories, reflecting the varying degrees of control that the Scottish Parliament has over each.

1. Fully devolved taxes

Fully devolved taxes are where responsibility for the tax rests exclusively with the Scottish Parliament, such as taxes on land transactions, landfill, aggregates and air passengers (although the latter two have yet to be made fully operational).

The Scottish Parliament also sets the rules for local authorities to collect two local taxes, council tax and non‑domestic (business) rates. It can legislate for new local taxes, as is currently happening with plans for a transient visitor (tourist) levy.

2. Partially devolved taxes

Partially devolved taxes are where responsibility is shared with the UK Parliament. This refers to Scottish income tax, where the UK is responsible for setting the tax base, defining taxable income and the administration and collection of income tax.

The Scottish Parliament can set income tax rates and bands beyond the personal allowance for Scottish income taxpayers and has since 2017. Scottish income tax rates apply to non-savings, non-dividend income (which is an interesting way to describe earnings, pensions and property income). ‘Scottish taxpayers’ are based on a test of residence.

3. Assigned taxes

Assigned taxes are where legislation and administration remain at the UK level but where a portion of tax receipts are allocated to the Scottish budget; for example, as proposed with VAT.

The ‘Scottish taxes’ are complicated and not always clearly understood, although the aim is to bring greater financial accountability. Lord Smith said in 2014 that: ‘A challenge facing both Parliaments is the relatively weak understanding of the current devolution settlement. This is not surprising, given what is a complex balance of powers. With the enhancement of these powers, improved understanding is all the more critical to sustaining the trust and engagement of the public.’

The CIOT continues to call for better public awareness in relation to these tax powers so that taxpayers can better understand where responsibility and accountability rests.

Some of the devolved taxes have yet to be implemented, whilst others are well established. Two of the fully devolved taxes – the land and buildings transaction tax and the Scottish landfill tax – were legislated for in the earlier Scotland Act of 2012 and implemented with effect from 1 April 2015.

The Scottish Budget on 19 December 2023 (see tinyurl.com/32c2hr6a) played safe with the rates for these taxes. The land and buildings transaction tax rates remain the same as in the current tax year (2023/24), while Scottish landfill tax rates are to be revised so that they maintain consistency with planned UK landfill tax increases.

A more contentious aspect of the land and buildings transaction tax regime is the tax charged when a person owns more than one residential property – the additional dwelling supplement. This is charged at 6% of the whole transaction price for properties costing more than £40,000.

Scottish income tax

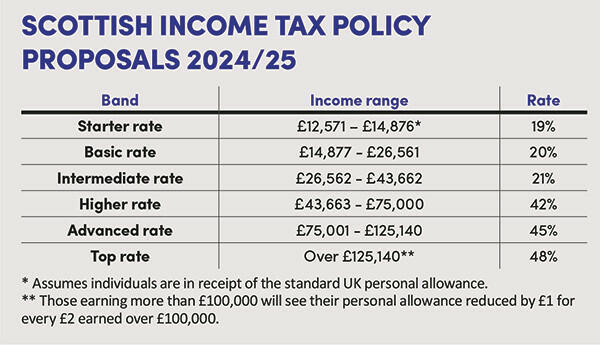

The highest profile announcements in the December 2023 Budget concerned Scottish income tax, where the Scottish government further increased the top rate of tax and introduced a new ‘advanced’ rate of tax. See Scottish income tax policy proposals 2024/25.

The proposals for a sixth ‘advanced’ rate of income tax were widely trailed, the proposal having first gained traction during the SNP leadership contest of early 2023. The Scottish government also announced that the starter and basic rate bands would increase by inflation.

As a result of these changes, the CIOT noted the following points in its Budget commentary (see tinyurl.com/zw83k6tj):

- Scottish income taxpayers start to pay more income tax compared with the rest of the UK with an income over £28,867.

- Scots with earnings under £28,867 will pay up to £23.06 less tax annually than those in the rest of the UK.

- Introducing a 45% rate of income tax on income between £75,000 and £125,140 will see Scots in this band pay up to £1,871.13 more than in 2023/24; and up to £5,231.81 more than someone on the same salary in other parts of the UK in 2024/25.

- Scots with income between the Scottish and UK higher rate thresholds will continue to pay a higher marginal rate of tax on this slice of income, compared to the rest of the UK, because lower rates of national insurance are tied to the UK higher rate threshold.

These comparisons will change if the UK Budget on 6 March 2024 revises UK income tax rates. The Scottish government has suggested that it will not change its income tax plans in the event of UK changes. However, if it were to do so, it would have a limited timeframe to implement these changes.

The mechanics of setting Scottish income tax rates (see tinyurl.com/37unt7tx) are different from those at Westminster. This is because under Scotland Act 1998 s 80C(6), the Scottish rate resolution which enacts the government’s tax plans must be passed before the start of the fiscal year to which it refers.

It also sits within the Scottish parliamentary Budget Bill process. The Bill goes through three stages of scrutiny in the Scottish Parliament; and the Parliament’s Standing Orders require the motion for the rate resolution to be moved and agreed to before the commencement of Stage 3 proceedings for the Bill. Regardless of the politics, the processes make it difficult to make late amendments to the Scottish rates of income tax.

It remains to be seen what may happen following the UK Budget on 6 March 2024 because, inevitably, a key measure of Scottish income tax rates is a comparison with the neighbours. Concerns have been expressed in some quarters about increasing divergence in tax payable between Scotland and the rest of the UK.

The Scottish Fiscal Commission has noted that the new income tax rate of 45% for those earning above £75,000, along with increasing the top rate by 1%, are estimated to raise a total of £82 million in 2024/25. This figure includes an adjustment for an assumed behavioural response, without which revenues would be £118 million higher.

Tax is only part of the funding package

The most significant element of funding for the Scottish government still comes from the block grant, which is based on the Barnett Formula. Other less visible elements also have a significant effect on the Scottish Budget; in particular, the impact of the block grant adjustments both in the way they work and their timing.

These form part of the fiscal framework (see tinyurl.com/mrxres9v) – the intergovernmental agreement – that underpins the mechanics of devolved funding, which was renegotiated in August 2023. Block grant adjustments detract from the notion of accountability because they lack visibility, and they can be difficult to understand.

While the recently renegotiated fiscal framework has extended the Scottish government’s ability to borrow, this power remains limited and is designed to assist with managing the impact of income tax reconciliations (see tinyurl.com/jjuvxnfh), rather than as a facility to support government spending. The Scottish government must have a balanced budget each year.

Future ‘Scottish’ taxes

Scottish income tax is now well established, as are the land and buildings transaction tax and the Scottish landfill tax. However, other Scottish taxes are at varying stages of implementation.

Aggregates tax

The Aggregates Tax and Devolved Taxes Administration (Scotland) Bill was introduced to the Scottish Parliament in November 2023 and makes provision for a devolved replacement for UK aggregates levy, to be known as the Scottish aggregates tax. Once enacted, the tax is expected to be introduced from 1 April 2026 and will be fully devolved, with its administration overseen by Revenue Scotland.

The Scottish aggregates tax is unique amongst devolved taxes in that there will be some interaction with its UK counterpart on cross-border supplies and could thus affect businesses throughout the UK.

Air departure tax

The Air Departure Tax (Scotland) Act 2017 is not yet operational. Until a solution can be found, UK-wide air passenger duty rates continue to apply in Scotland.

VAT and the assignment of a proportion of ‘Scottish VAT’

The Scotland Act 1998 (inserted in 2016) allows for the first 10p of standard rate VAT and the first 2.5p of reduced rate VAT raised in Scotland to be assigned directly to the Scottish Budget. However, problems remain with the lack of a suitable model for identifying VAT attributable to Scotland, the lack of policy autonomy that would be afforded to the Scottish government from a policy of ‘assignment’, and the introduction of additional risks to the Scottish Budget.

The Chair of the Scottish Parliament’s Finance and Public Administration Committee, which held a roundtable session on this in November 2023 (see tinyurl.com/2edjsku4), summed up with the question: ‘How long can you flog a dead horse? There is no enthusiasm certainly for assignment anyway.’ Progress updates have been promised, but it remains to be seen whether the policy will proceed.

Local taxes

Local taxes offer a mix of substantial sums from council tax and non-domestic rates, and lesser sums from sources such as a workplace parking levy (enacted in the Transport (Scotland) Act 2019) or a ‘tourist tax’ (The Visitor Levy (Scotland) Bill having been introduced to the Parliament in May 2023). The latter two each provide a framework for levying a tax, allowing any local authority that wishes to then be able to implement the tax in their area.

A more contentious and longstanding issue relates to council tax, with calls from many parties in Parliament that the tax should be reformed or, at the very least, that the valuations on which it is based (which date back to 1991) be updated.

The Scottish government’s 2021 cooperation agreement with the Scottish Greens included a commitment to look at options for reform. However, the surprise announcement at the SNP conference in October 2023 that council tax would be frozen in 2024/25 (since confirmed in the Scottish Budget) cast further doubt on the issue of reform. There have been suggestions that a timetable for change will be announced in the early part of 2024 but, at the time of writing, reform remains in the long grass.

Other proposals that the Scottish government says it is examining and which were referenced in the Budget include:

- a building safety levy to fund the Scottish government’s Cladding Remediation Programme (currently subject to consultation);

- a cruise ship levy;

- a carbon emissions land tax;

- the reintroduction of a non-domestic rates public health supplement for large retailers; and

- an infrastructure levy.

Much has been accomplished

Since the Smith Commission delivered devolved tax proposals to the Scottish Parliament, much has been accomplished. There is now a Scottish government directorate for tax, which has sought to open up tax policy making to a process of consultation and engagement, setting out a Framework for Tax (see tinyurl.com/2jddkhyd), and working with stakeholders on the development of legislation (for instance, with its recent work on aggregates tax).

The decision to establish a Tax Advisory Group last summer was done with the intention of developing longer-term strategic thinking around tax policy (see tinyurl.com/ynm6kuac). The Scottish Parliament has also passed several tax Acts and has established new institutions such as:

- Revenue Scotland to collect the fully devolved taxes;

- the Tax Chamber in the First-tier Tribunal for Scotland to hear cases involving the fully devolved taxes; and

- the Scottish Fiscal Commission to produce Scotland’s official, independent economic and fiscal forecasts.

The machinery of government has also adapted to tax devolution, setting up operating agreements (the fiscal framework) between the UK and Scottish governments, and agreements between HMRC and the Scottish government to enable the collection of Scottish income tax.

Building a better tax system

Although much has been accomplished, there are some areas that could be further improved. In December 2023, the CIOT and ICAS published ‘Building a better tax system: progress report’ (see tinyurl.com/mnufe2jn), setting out recommendations for the remainder of the 2021-26 Scottish Parliament. These include the following.

Strengthening decision making

The Scottish Parliament and Scottish government should work together to review whether the current processes for scrutinising tax legislation are as good as they can be. This should include consideration of the merits of a Scottish Finance Bill. The goal of this work should be to ensure that devolved tax legislation can be appropriately considered, and that technical changes and anomalies can be identified and addressed in a timely manner, ideally through primary rather than secondary legislation.

The first report called for the reconvening of the Devolved Taxes Legislation Working Group to assist in this work. This recommendation remains outstanding. The issues that the group was set up to consider remain, such as a lack of parliamentary time for tax scrutiny, the need for legislation to be regularly reviewed and kept up to date, and the ability to consult with outside experts.

Making the case for new taxes

There should be a consistent approach to tax policy making, with all proposals subject to consultation and engagement with relevant stakeholders. This can help to ensure that tax policy is developed in a consistent and strategic manner, taking into consideration interactions with the wider Scottish and UK tax systems. Effective stakeholder engagement will also help to ensure that taxes operate as intended, with any operational issues identified and addressed.

The Scottish and UK governments should use the Smith Commission’s tenth anniversary in 2024 to review the package of powers delivered to Holyrood. Efforts to overcome the challenges that have prevented the introduction of some of these taxes should be intensified. If the difficulties cannot be resolved for good reasons, a statement to that effect should be made to provide certainty and transparency to decision makers.

Improving public understanding

More effort is needed to raise awareness of how Scotland’s tax system works. Taxpayers need to be able to understand their rights and responsibilities – especially low-income taxpayers, who may be unable to afford professional advice.

In summary

Much has been done to strengthen the Scottish Parliament’s responsibilities over tax but there is scope for improvement. If further taxes are to be devolved or assigned, there need to be robust and consistent processes underpinning them.

Questions remain about the suitability of the legislative processes for making and amending tax law and a lack of general understanding of Scottish taxes continues to be a cause for concern. But a willingness to consult and engage with stakeholders, including the tax profession, means we can have confidence that our expertise and influence can be contributed.