SME and RDEC R&D schemes: getting ready to merge

Share this article

With plans announced to merge the SME and RDEC R&D schemes from April 2024, we consider the draft legislation released so far and the potential design problems.

Key Points

What is the issue?

The January 2023 consultation on merging the SME and RDEC R&D schemes makes clear that simplification and improving the competitiveness of the scheme are key objectives.

What does it mean to me?

Relief for ‘R&D intensive’ companies will remain higher than the current SME scheme and, as things stand, this means it is likely to be carved out from the merged scheme.

What can I take away?

The concept of the UK having a single above-the-line R&D tax relief is attractive because of the clarity and prominence in the accounts that it brings.

Following a consultation in 2021 (on wider research and development relief reforms) and more specifically in January 2023 on merging the current schemes, the government published updated proposals and draft legislation on 18 July 2023. Although the July policy document describes this as a ‘potential merger’, the government has been working towards this for several years and it seems fairly certain to be achieved.

Why is this happening? Let’s be in no doubt that ensuring ‘taxpayers’ money is spent as effectively as possible to support innovation’ is an important consideration. However, the January 2023 consultation makes it clear that simplification and improving ‘the competitiveness of the R&D expenditure credit (RDEC) scheme’ are also key objectives.

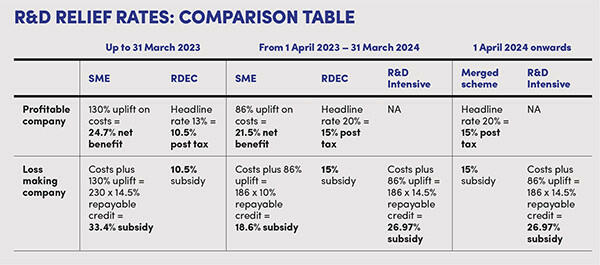

From the earliest stages of this reform process, businesses were concerned that merging the schemes was simply a pretext for reducing the rate of relief under the SME scheme. However, the government chose to address this issue head on by reducing the headline rates of relief under the SME scheme and raising the rates of relief under RDEC. Claiming that it has ‘broadly aligned the generosity of the two schemes’ (see the Comparison Table on page xx), the government now feels it can press ahead with merging the schemes from April 2024.

Of course, as with all tax legislation, there is a caveat. Relief for ‘R&D intensive’ companies will remain higher than the current SME scheme and, as things stand, this means it is likely to be carved out from the merged scheme. How this can be squared with the simplification objective remains to be seen: I will consider some of the practical problems that could arise from this approach below.

I should make clear from the outset that there is no suggestion that the core definition of what constitutes R&D for tax purposes (under the Department for Science, Innovation and Technology (DSIT) guidelines) will change for the merged scheme: claimants will still need to prove that their project sought to achieve an advance in science or technology.

RDEC plus

From the earliest stages, it has been clear that the combined scheme would principally be based on the current RDEC rules, and the current rate of relief will apply to all claimants. This should help to raise the prominence of the R&D function within a business by recognising the R&D incentive in a company’s pre-tax income – the ‘above the line credit’. It will also make it easier for larger businesses to make the transition, but SMEs will need to start planning for the change and another drop in tax relief soon.

While it is positive that the above the line credit will make the impact of R&D relief more obvious in company accounts, it is rather disappointing that the seven step process for calculating RDEC relief (currently Corporation Tax Act 2009 s 104N) is to be retained. One wonders how smaller SMEs will manage to apply this accurately in practice, as it can already cause complexities for large businesses with significant accounting resources.

However, in other areas legislators are taking the ‘best bits’ from the SME scheme to simplify the merged scheme rules. For example, both the current schemes include rules that limit the amount of relief that can be claimed when a company is loss-making, but the SME scheme rules are the more generous of the two. Broadly, it caps the refund that a loss-making company can claim to £20,000 plus three times its PAYE and NICs liability for the period of the claim. There are also specific exemptions from it for companies investing heavily in developing their own intellectual property. It is proposed that the merged scheme will adopt the SME scheme loss cap rules – these tick the boxes on both simplicity and competitiveness grounds.

Subcontracting R&D work

Here there is another positive development for large companies already claiming the RDEC. At present, companies claiming under RDEC can only claim for the costs of outsourcing their R&D when the work is subcontracted to a limited number of qualifying bodies (e.g. universities and other not for profit organisations) or to individuals. This would expand significantly under the merged scheme, which it is suggested would adopt the current SME rules allowing costs for most outsourced R&D to be claimed – apart from overseas costs (see below). However, the current 65% restriction on outsourced costs that can be claimed by SMEs would continue.

Of course, where project work is subcontracted to a third party, there will always be the question of who claims the R&D relief. Under the SME rules, it is normally the principal, so importing these rules wholesale into the merged scheme (as the draft legislation currently does) would have considerable consequences for certain parts of the UK’s R&D base – especially contract research organisations operating in the UK.

From engagement with HMRC, I understand that legislators are concerned about this issue and are investigating ways to draft the legislation to allow commercial flexibility over which party can claim the R&D relief in subcontracting situations, whilst ensuring that relief cannot be claimed by both parties. So hopefully we can look forward to further proposals in this area as the legislative process continues.

What does seem to be finalised already is that the merged scheme will also reflect HMRC’s recent concern over the costs claimed for externally provided workers. Such costs will only be claimable if they relate to UK workers and where the worker is part of (and paid through) a PAYE scheme. This means that costs for outsourcing work to self-employed individuals or those working through a personal service company could not be claimed under the merged scheme – building in an anti-avoidance measure for contract workers.

Of course, the government has already proposed a ban on claiming for all overseas outsourcing costs (apart from a few limited exceptions) and, after a one-year delay, this is also now due to take effect for costs incurred on or after 1 April 2024. This ban would be a feature of the new merged scheme, although the exceptions would also apply.

Subsidised R&D

To quote the current Corporate Intangibles Research and Development Manual (CIRD89760): ‘There is no provision preventing subsidised expenditure from qualifying for R&D Expenditure Credit’, but there are restrictions under the SME scheme.

In recent years, HMRC has pursued a number of tax cases where it claimed that the cost of the R&D work was effectively subsidised and so cannot be claimed under the SME scheme. For example, in Hadee Engineering Co and others v HMRC [2022] UKUT 84, HMRC successfully claimed that R&D work carried out to develop a product for a customer was effectively subsidised by that customer.

This trend would continue within the merged scheme, as the proposed rules would not allow an R&D claim to be made where any form of subsidy or grant is received in respect of the R&D project. The proposed new s 1042C would impose this block on large companies for the first time.

However, sharp-eyed readers of the draft legislation will have noticed that this new section is shown in square brackets. It is my understanding that this is because legislators are considering ways to make this part of the proposals redundant. There has always been a friction between receiving a grant and claiming R&D relief on a project, so on the grounds of simplicity and competitiveness that would be a very positive development.

R&D intensive companies

At the Spring Budget, the Chancellor made a commitment to preserve a higher rate of R&D relief for ‘R&D intensive’ companies. Draft legislation to implement this higher rate was introduced alongside the proposals for the merged scheme (see the table R&D relief rates: comparison table).

Why not simply include the R&D intensive relief as an option within the merged scheme? I understand that HMRC is trying to align component elements of the rules of the R&D intensive scheme and the merged scheme as far as possible, but it has cost concerns about including the R&D intensive relief directly within the merged scheme.

What is R&D intensive?

The draft legislation defines R&D intensive companies as those whose qualifying R&D expenditure constitutes at least 40% of their total expenditure. Total expenditure for this purpose will be calculated from the total expenses figure in the profit and loss account, adjusted by adding any amount of expenditure used under Corporation Tax Act 2009 s 1308 and by subtracting any amount not deductible for corporation tax purposes. This threshold is unlikely to be met by many companies. I’d expect only a small number of technology start-ups and university spin-out businesses to qualify.

The difficulty with this definition is that it will offer a financial incentive for companies to manage their accounting policies to ensure that their R&D spend exceeds 40% of total expenditure. Perhaps considerable amounts of complex anti-avoidance legislation could be created to prevent this, but we must hope the risk is simply designed out.

While it has potential difficulties in its own right, it is the interaction of this new relief with the merged scheme that could present the most practical problems.

In this year, out the next?

As I have already explained, the relief for R&D intensive companies will be much higher than for companies claiming under the merged scheme. But what if your R&D costs for differing years genuinely vary between say 33% and 45% of your total costs? The company will have to switch between the intensive scheme and the merged scheme with significant impacts on their cashflow.

Worse still, the R&D intensive scheme will operate its relief in the same way as the current SME scheme – refunds to the company. So for a year when a company does not quite reach the 40% threshold, not only will it get less tax relief, but it will also have to show the relief in its accounts in a totally different way. This may have consequences far beyond cashflow – with potential knock-on effects for shareholders’ agreements, borrowing covenants, bonus schemes, etc.

Adding some form of averaging clause to the R&D intensive scheme to protect companies whose total R&D costs slip from 42% to 39% from one year to another may reduce this risk. However, there will always be some who fall outside these and have to face the consequences of switching schemes. Therefore, I hope that the government can find some form of compromise so that the higher rates of relief for R&D intensive companies can be included within the merged scheme before it is launched to avoid this practical problem.

Looking ahead

Having worked on R&D claims for many years, the concept of the UK having a single above-the-line R&D tax relief is attractive because of the clarity and prominence in the accounts that it brings. Legislators have made a strong start in designing a merged scheme but much is still to be decided and finessed to achieve their simplicity and competitiveness objectives. We must hope that these two aims are not sacrificed for a blinkered view of ‘cost effectiveness’ when the final design is approved by Parliament.