Statutory residence test: establishing ties to the UK

Share this article

Determining whether an individual is UK tax resident in a particular year can be more complicated that you might expect.

Key Points

What is the issue?

Whilst the statutory residence test does provide clarity for many taxpayers, there are still areas where the rules are not clear cut.

What does it mean to me?

A series of tests – automatic overseas tests, automatic UK tests and sufficient ties tests – are used to determine whether an individual is UK tax resident for a particular year.

What can I take away?

A number of complexities, inconsistencies and uncertainties can make this a challenging issue.

The statutory residence test was introduced in April 2013 by the Finance Act 2013. When it was announced at the 2011 Spring Budget, it was stated that it would ‘provide greater certainty for taxpayers’. However, whilst the statutory residence test does provide clarity for many taxpayers, there are still areas where the rules are not clear cut. HMRC’s guidance is at: tinyurl.com/5dzrdyzx.

An overview of the statutory residence test

The statutory residence test is a series of tests which must be applied in a strict order for each tax year. Firstly, an individual must assess whether they meet any of the automatic overseas tests (see below). If this is the case, then they are not UK tax resident for the relevant tax year.

If the individual does not meet any of the automatic overseas tests, they must assess whether they meet any of the automatic UK tests. If they do, then they are UK tax resident for the relevant tax year. If the individual does not meet any of the automatic tests, then they must apply the sufficient ties test. This considers both their days present in the UK and the ties they have to the UK.

If an individual is UK resident for a tax year, they may also be able to consider if they will qualify for split year treatment. Split year treatment may apply in the year that an individual moves to or leaves the UK. If the individual meets the necessary criteria, the tax year will be split into a UK part and an overseas part. The individual will then be taxed as though they were non-UK resident during the overseas part of the year, for the purposes of some (but not all) tax provisions.

Automatic overseas tests

The automatic overseas tests are as follows:

- The individual was UK resident in one or more of the previous three tax years and spends fewer than 16 days in the UK.

- The individual was not UK resident in any of the previous three tax years and spends fewer than 46 days in the UK.

- The individual works full time overseas, with limited visits to the UK. There are a number of criteria that need to be considered in establishing whether an individual meets this test, including a calculation of whether they have worked sufficient hours overseas.

There are further tests that apply where an individual dies in a tax year which are not covered here.

Automatic UK tests

The automatic UK tests are as follows:

- The individual spends 183 days or more in the UK.

- The individual has their only home in the UK. An individual has a home in the UK for these purposes if they have a home for a period of at least 91 consecutive days (of which 30 or more fall within the relevant tax year) and they actually used the home for at least 30 days in the tax year. An individual will not have a home overseas for these purposes if they either have no home overseas, or they have a home but spend fewer than 30 days there in the relevant tax year.

- The individual works full time in the UK. This test varies from the full-time overseas work test as there is no limit on time spent overseas. Moreover, it will apply to a tax year if the individual works full time in the UK for a 365 day period, any part of which falls in the relevant tax year.

As for the automatic overseas tests, there is also a test which applies where an individual dies in the tax year.

Sufficient ties test

In establishing whether an individual is UK resident or not under the sufficient ties test, it is necessary to establish the days they have spent in the UK and their ties to the UK.

The days an individual is present in the UK for these purposes is calculated as follows:

- Take the number of days on which the individual is present in the UK at midnight during the tax year.

- Deduct any days on which the individual is only present in the UK due to transiting through the UK.

- Deduct any days on which the individual is only present in the UK due to exceptional circumstances (limited to 60 days).

- Add any days where the individual is deemed to be in the UK. Broadly, this applies to some individuals who have more than 30 days on which they were present in the UK during the day but not at midnight.

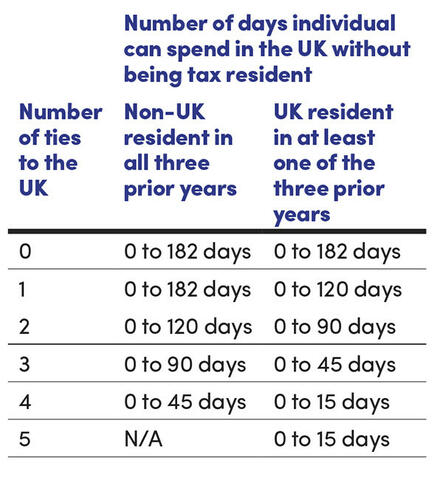

The ties which need to be considered are as follows:

- Family tie: An individual has this tie if their spouse, civil partner, cohabiting partner or minor child is UK resident for the tax year. There are certain exemptions where minor children are only in the UK for full-time education or where the individual does not spend sufficient time with a minor child.

- Accommodation tie: An individual has this tie if they have accommodation available to them for a period of at least 91 days, at least one day of which falls in the relevant tax year, and they spend at least one night there. The home of a close relative can also be considered for the purposes of the accommodation tie, but only if the individual spends a total of 16 nights or more there in a given tax year.

- Work tie: An individual has this tie if there are 40 days or more on which the individual does more than three hours’ work in the UK.

- 90 day tie: An individual has this tie if they spent more than 90 days in the UK during at least one of the two previous tax years.

- Country tie: This tie only applies to individuals who have been UK resident in one of the three previous tax years. An individual has this tie if the country in which they spend the greatest number of days in the tax year is the UK. For these purposes, days are counted where the individual is present at midnight.

Whether an individual was UK resident in one of the three previous tax years will impact how many days an individual can spend in the UK without being UK tax resident. The number of days an individual can spend in the UK without being tax resident are as follows:

Issues with the statutory residence test

Complexities and inconsistencies

Whilst the statutory residence test does provide certainty for most taxpayers in respect of their residence status, the rules are complex. Moreover, there are a number of areas where similar but differing terms and tests are used. The complexities include:

Accommodation v home: The term accommodation is used for the purposes of the sufficient ties test (namely, the accommodation tie). The term home is used for the purposes of the second automatic UK test and some of the split year cases. A property could qualify as an individual’s home without giving the accommodation tie; for example, because it was not available for a period of 91 days. Similarly, an individual may have an accommodation tie without having a home if they have the use of their employer’s property.

Full-time work v work tie: As already mentioned, the tests for determining full-time work overseas and in the UK differ. In addition, the test for whether an individual works full-time overseas limits them to 30 days work in the UK. On the other hand, the test for whether an individual has the work tie is whether they work in the UK on 40 days.

Day counting: An individual will have different day counts for different purposes. For example, an individual may count a day as a workday (because they work more than three hours in the UK) but it is not a day of presence (because they left before midnight). Moreover, whilst days spent in the UK under exceptional circumstances and transiting may be excluded for calculating an individual’s days in the UK for the sufficient ties test, these days are not excluded for establishing whether they have the country tie or the work tie/full-time work overseas. It can therefore be necessary for an individual to keep multiple running totals of UK days.

Record keeping: It is important for a taxpayer to keep sufficient records both to enable them or their advisors to determine their residency position, and also to provide evidence to HMRC in case of an enquiry. In respect of days spent in the UK, documents such as boarding passes and passport stamps may be sufficient. For matters such as work days, the position may be harder to prove, especially if trying to prove a negative (i.e. that an individual did not work more than three hours on a given day).

Uncertainties

In addition to areas where the legislation is complex to apply, there are areas where there is a lack of certainty.

Home: Whilst the legislation does define ‘home’ for the purposes of the statutory residence test, there is uncertainty regarding when a property would be considered a home. For example, the legislation states that a property which is ‘nothing more than a holiday home’ will not qualify (Finance Act 2013 Sch 45 para 25(3)). However, the formulation of the legislation necessitates that an individual’s second (or third of fourth) home could qualify. Whilst some cases will be clear cut, there will be others where the position is not clear.

Exceptional circumstances: When counting the number of days an individual has been present in the UK, it is possible to exclude up to 60 days if they were only present in the UK because of exceptional circumstances and they leave the UK as soon as those circumstances permit. The legislation gives examples of ‘national or local emergencies’ and ‘a sudden or life-threatening illness of injury’; however, these are examples and are not therefore an exhaustive list.

There has been one case on exceptional circumstances (A Taxpayer v HMRC [2023] UKUT 182 (TCC)), which has been heard by both the First-tier Tribunal and the Upper Tribunal. (The taxpayer won initially, with HMRC succeeding on appeal.) Whilst this case gives some guidelines for how to approach exceptional circumstances, the judgment was inevitably very specific to the facts of the particular case and therefore there remains uncertainly in this area.

See ‘Family misfortunes: Exceptional circumstances rule’ by Keith Gordon for details of A Taxpayer v HMRC.