Stock in trade

Share this article

Carrie Hendrickson considers the challenges involved with trading goods with the EU post-Brexit

Key Points

What is the issue?

VAT and Customs duty rules differ depending on whether UK businesses trade goods with the EU or third countries. After the UK leaves the European Union, there is a possibility that the current rules for trading with third countries could apply to trading with the EU as well.

What does this mean to me?

UK businesses should be aware of these differences and consider the potential impact any changes may have on the way they trade with the EU in the future.

What can I take away?

Customs duty is irrecoverable and is currently only levied when goods are imported from third countries. If Customs duty is imposed on goods sourced from the EU post-Brexit, this will be an absolute cost to UK traders. Businesses should start planning ahead to consider how the will deal with the challenge and how any potential costs could be mitigated.

UK businesses that trade goods with businesses in other EU Member States presently benefit from certain VAT accounting simplifications for ‘intra-community supplies’, along with the elimination of Customs duties on goods that are in free circulation. This is due to the free movement of goods afforded to EU businesses trading within the Single Market. However, there are key differences that apply where goods are traded with businesses established in ‘third countries’ i.e. businesses that are outside the EU.

Although there is currently much uncertainty regarding the future status of the UK’s trading relationship with the EU post-Brexit, one natural assumption is that, once the UK leaves the EU, all goods entering and leaving the UK will be regarded as arriving from or going to third countries. If this is what transpires, this is an opportune time for UK businesses that trade goods with the EU to start planning ahead by considering the potential impact of applying the existing rules for trading with third countries.

Acquisitions vs imports

In the indirect tax field, goods received by businesses in the UK from other EU Member States are regarded as ‘acquisitions’, whilst goods entering the UK from third countries are regarded as ‘imports’. In addition to the different terminology used to describe these movements of goods into the UK, there are also different VAT and Customs duty implications.

Acquisitions from the EU

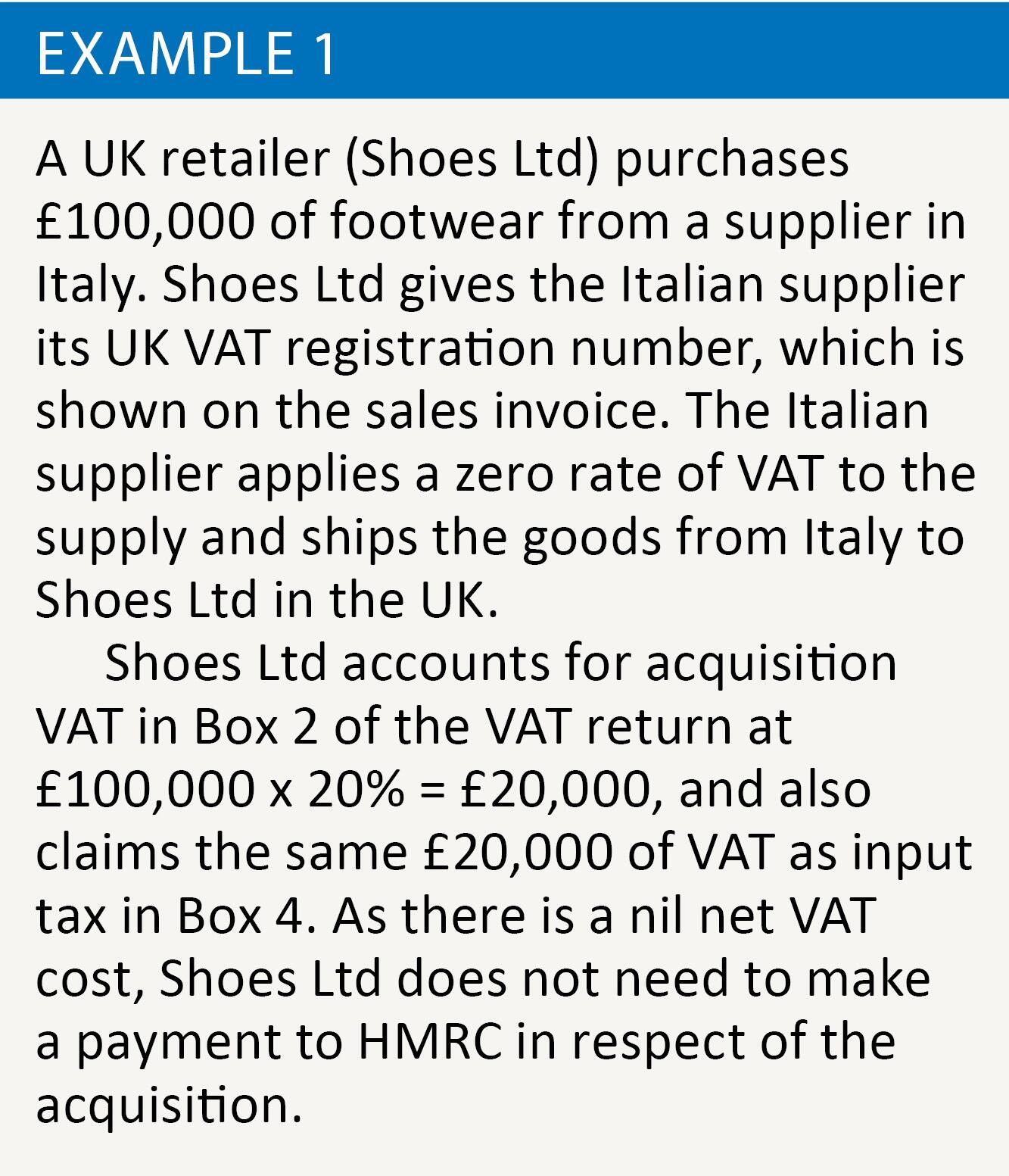

When a UK VAT-registered business makes an acquisition of goods from a supplier based in a different Member State, the dispatching supplier applies a zero rate of VAT to the sale. HMRC require the UK trader to self-account for acquisition VAT, and there is generally no negative cash flow implication for the acquiring business. In order to apply a zero rate of VAT to this intra-community movement of goods, the EU supplier is required to show the customer’s UK VAT registration number on the sales invoice and obtain evidence that the goods have left the particular EU Member State. If the supplier cannot do this, VAT must be charged at the rate that would be applicable to a supply of the goods in the Member State of dispatch.

In order to self-account for acquisition VAT, the UK recipient calculates VAT on the Sterling value of the goods at the relevant UK VAT rate that would be applicable if they were purchased in the UK, i.e. 0%, 5% or 20%. This acquisition VAT is accounted for as output tax in Box 2 of the VAT return, and can be claimed as input tax in Box 4. Intrastat Supplementary Declarations would also have to be submitted by a UK business where the value of all the goods it acquires from EU suppliers in a calendar year exceeds the £1.5m arrivals threshold. See example 1.

Customs

Since the acquisition transaction constitutes a free movement of goods between EU Member States within the Customs Union, there is no Customs duty consideration and no Customs declaration is required when the goods either leave the dispatching Member State or enter the UK. Therefore, in its simplest form, the process of a UK business receiving goods from EU suppliers is very straightforward when compared to third country trade, with the EU’s principle of free movement of goods facilitating intra-community trade.

Imports from third countries

The process is more onerous for businesses importing and exporting goods into and out of the UK from and to third countries. This is due to the administrative burden, as well as the physical and technical restrictions that are in place when trading outside the Single Market.

When a UK business purchases goods that arrive directly from suppliers in third countries, import VAT is charged and payable once the goods enter the UK. This import VAT liability becomes a cash flow cost to the importing business. Customs duties are also due in most circumstances, with the applicable duty rate driven by the tariff classification of the goods. Assuming that the UK will adopt a ‘hard’ Brexit (i.e. it will leave both the EU Single Market and the Customs Union), it is important for UK businesses to become familiar with and understand both the VAT and Customs duty implications of importing goods.

Import VAT

Similar to acquisitions, import VAT is also calculated at the VAT rate that would be applicable if the goods were purchased in the UK. However, the way in which import VAT is accounted for differs to the self-accounting that businesses carry out for acquisition VAT. Import VAT is calculated on the Customs value of the goods, plus any duties that are payable, as well as incidental costs incurred from transporting the goods to the first destination in the UK that are not already included within the Customs value.

Once the imported goods are declared to HMRC, the import VAT and Customs duty must be paid before the goods can be released into free circulation. To assist with cash flow, businesses can obtain authorisation from HMRC to use a duty deferment scheme, such as a Customs Comprehensive Guarantee (CCG). This involves having a guarantee from an approved financial institution to cover the import VAT and Customs duty liabilities, and enables payment to be deferred until the 15th day of the following month.

Traders that hold a CCG can employ measures to reduce the guarantee amount, which in turn reduces the capital tied up in guarantees. To this effect, UK businesses may seek authorisation from HMRC to use Simplified Import VAT Accounting (SIVA), which removes the requirement to provide a financial guarantee to cover the import VAT element of the CCG. By reducing the deferment guarantee level, SIVA helps businesses to save on compliance costs when importing goods.

A UK VAT-registered business must also currently obtain an Economic Operator Registration and Identification (EORI) number in order to trade goods outside the EU. This EORI number is required for HMRC to issue an Import VAT Certificate (form C79), which is used as official evidence to recover the import VAT as input tax. As the EORI system is an EU scheme, this is likely to be replaced by a UK-only system once the UK leaves the EU.

Customs duty

Any Customs duty paid on the importation of goods from third countries is irrecoverable (that is, unlike import VAT, it cannot be reclaimed) and is, therefore, an absolute cost that affects the profits of a business. If the future receipt of goods in the UK from EU suppliers follows the present treatment of imports from third country suppliers, there will be an immediate financial cost to UK businesses where Customs duties become payable. Businesses will also have to consider the impact of the increased time and administrative costs involved in complying with the formalities for clearing imported goods.

When a business imports goods into the UK, the goods have to be declared to HMRC at the point of entry. Clearing imported goods primarily involves completing a Customs declaration known as a Single Administrative Document (SAD), or the UK version of this form known as a C88. This declaration features a number of items, including those used for determining the amount of duty payable, such as the country of origin, commodity code, Customs value, and any Customs procedures being applied. The SAD or C88 is submitted electronically to the Customs Handling of Import and Export Freight (CHIEF) system.

Completing the Customs entry is a very important part of the import process and can be difficult for businesses to get right. For example, there are six general interpretative rules (GIRs) used for determining how imported goods are classified, which identifies what duty rate is applicable on importation. There are also six valuation methods, which businesses need to understand and consider in order to ensure that they apply the correct Customs value on which the duty is calculated.

Due to these complexities, most businesses choose to use agents such as freight forwarders to complete Customs entries on their behalf. However, it is key to note that in the majority of cases where an agent makes the import declaration, the importing business remains responsible for the particulars of the declaration, and liable for any duties payable.

After Brexit, Customs compliance will be a hidden cost that is additional to the actual duty liability that could become payable by a UK trader. Failure to ensure that the business remains compliant increases the likelihood of penalties being assessed where import entries are completed inaccurately. HMRC also have the ability to recover any under-declared duty retrospectively for three years, for instance, where a lower duty rate was used due to incorrectly classifying the imported goods.

Businesses need to ensure they have robust internal Customs processes and controls in place in order to deal with the complexities of importing goods into the UK. This may involve businesses investing in people and IT systems in order to manage their operations and compliance requirements appropriately. Additionally, importers with existing internal resource to manage Customs compliance will need to consider upscaling to cope with any increase in Customs formalities.

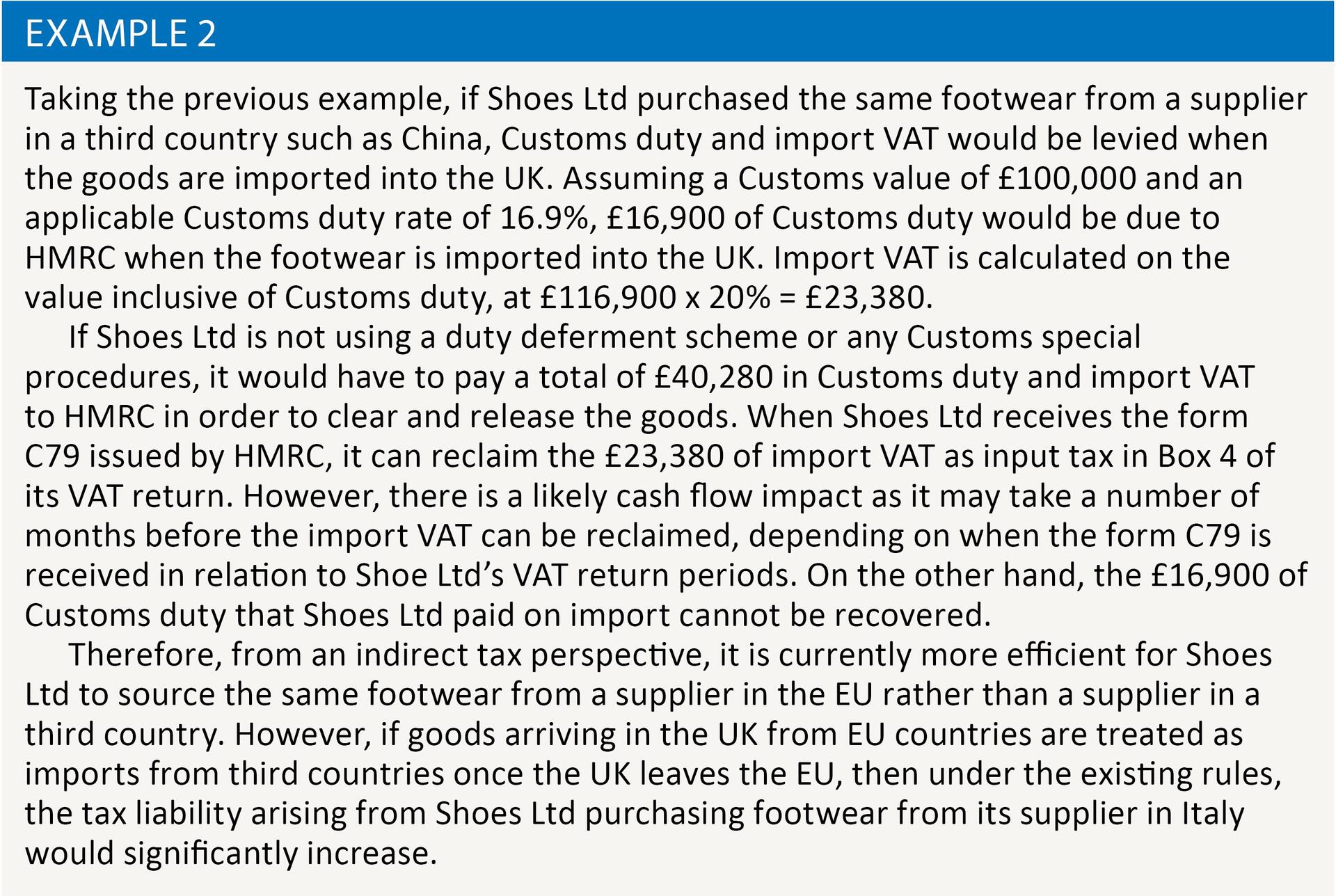

Customs special procedures may also be employed by businesses, which would reduce the duty liability. Examples include Customs Warehousing, which allows no duty to be paid on goods that are subsequently exported; Inward Processing which enables goods to be imported, processed in the UK and then exported duty free; and End Use relief which allows goods meeting a prescribed end use to be imported free of duty. UK businesses that are planning for ways to deal with the potentially negative impact that Brexit may have on trading with the EU should consider whether there are any suitable special procedures that would mitigate irrecoverable costs that could be imposed. See example 2.

Sales to the EU

It would also be useful for traders to review the position for sales of goods from the UK to businesses in the EU in the absence of the free movement of goods. If the sale and transport of goods from the UK to an EU business becomes an export to a third country, then it follows that the EU customer would be required to treat the purchase as an import rather than an acquisition.

From this perspective, there could potentially be shipment delays due to the additional administration of completing export declarations when the goods leave the UK, as well as import VAT and Customs duty costs that may be incurred by the consignee when the goods are cleared in the EU. This could result in an increase in the overall cost of the goods to EU businesses that trade with UK suppliers.

Conclusion

Although the exact terms under which the UK will trade with the remaining EU Member States post-Brexit are not yet known, businesses should nevertheless be aware of the potential VAT and Customs duty consequences, should the benefits of the UK being a member of the Single Market be withdrawn. Affected traders might consider scenario planning as a means of understanding the impact of any additional costs on their ability to remain competitive, as well as ensuring they are agile enough to react to possible changes in their supply chains.