Substantial shareholding exemptions: unusual pitfalls

Share this article

How to avoid falling foul of the more nuanced areas of substantial shareholding exemption.

Key Points

What is the issue?

It can sometimes be assumed that the substantial shareholdings exemption is available even in cases where this may not be the case.

What does it mean to me?

When assessing the availability of the substantial shareholdings exemption, joint venture arrangements and preferential instruments can cause uncertainty as to the availability of this exemption.

What can I take away?

Care should be taken to ensure that the specific facts and circumstances of each structure are carefully considered before making an assessment as to whether the exemption is available.

In the context of M&A transactions, the ability to benefit from the UK substantial shareholding exemption on gains derived from the sale of shares (or interests in shares) is commonly relied on and, in fact, is sometimes assumed to be available without formal analysis.

Recent changes to UK tax law have either:

- removed the requirement to assess the application of this position in certain circumstances (namely, the introduction of the UK qualifying asset holding company regime); or

- added additional routes by which the requirements can be met (through the qualifying institutional investor sub-set of rules).

However, this has not removed the requirement for careful analysis to be carried out to avoid falling foul of the more nuanced areas of the legislation.

Overview of the substantial shareholding exemption

The substantial shareholding exemption applies to exempt a qualifying gain (or loss) arising to a company (the ‘investing company’) on a disposal of shares (or interest in shares) in another company (the ‘company invested in’).

There are two primary tests that need to be met in order to benefit from the substantial shareholding exemption:

- The investing company must have held a ‘substantial shareholding’ in the company invested in throughout a 12 month period beginning not more than six years from the date on which the disposal takes place.

- The company invested in must have been a ‘qualifying company’ throughout the period beginning from the start of the 12 month period referenced above and continue until the date of the disposal (and immediately after in the case of a disposal to a person connected with the investing company).

In the case of investing companies that are owned 25% or more by qualifying institutional investors, there are additional ways to meet the substantial shareholding requirement, through the qualifying institutional investor sub-set of rules.

A detailed explanation of the requirements that need to be met in order to benefit from the substantial shareholding exemption is outside the scope of this article. Guidance can be found in Capital Gains Manual CG53000P to complement the relevant legislation (Taxation of Chargeable Gains Act 1992 Schedule 7AC, referred to throughout unless stated otherwise).

Joint venture companies

Typically, in the case of M&A transactions, the ‘company invested in’ is a holding company (rather than a trading/operating entity), such that Part 3 requires an assessment of whether it is the ‘holding company of a trading group/subgroup’ (i.e. looking down through the structure to the underlying operating business). In evaluating the holding structure, it is important to consider whether there are joint venture arrangements that could impact the Part 3 ‘qualifying company’ status of the company invested in in (see Capital Gains Tax Manual CG53114).

A company is a ‘joint venture company’ if it is not a member of the same group as the company whose status is being determined, and:

- it is a trading company or the holding company of a trading group/subgroup; and

- five or fewer persons hold 75% or more of its ordinary share capital. For this purpose, all members of a group are treated as a single person.

In the case of joint venture companies, when determining the trading company status of a company (Company A), the holding of shares in the joint venture company by Company A shall be disregarded (provided that holding is at least 10%, taking account of shares held by Company A’s group members). Company A shall instead be treated as carrying on an appropriate portion of the activities of the joint venture company; or, where the joint venture company is a holding company, the activities of that company and its 51% subsidiaries.

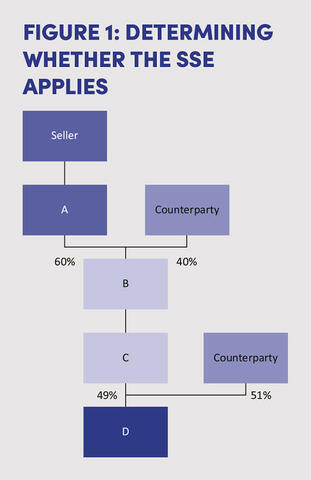

As set out in Figure 1: Determining whether the SSE applies, Seller is looking to dispose of its shares in Company A. It needs to determine whether the substantial shareholding exemption is available in respect of any gains arising on disposal. All companies in this example are holding companies, except for Company D (the trading entity).

As Company B is a joint venture company, Company A shall be treated as carrying on the activities of Company B (of which there are no trading activities, only holding company activities) and its 51% subsidiaries when evaluating whether the ‘Part 3: Company invested in’ test is met.

- Company C is a 51% subsidiary of Company B but is a holding company, such that it has no trading activities of its own.

- Company D is a trading company but is not a 51% subsidiary of B (indirectly).

Given the above, when considering whether Company A is a trading company or a holding company of a trading group/subgroup, arguments can be made that the activities of Company D would not be included (when taking a ‘top-down’ view starting at the seller), resulting in the ‘Part 3: Company invested in’ test not being met. Given the lack of guidance or prescriptive legislation in this regard, taking a ‘bottom-up’ approach (i.e. considering the trading entity in the first instance) may give rise to a more positive interpretation of these rules.

It is not uncommon for joint venture arrangements to exist at multiple levels in a structure. Joint venture arrangements are also often bespoke with complicated commercial objectives. Specific analysis should therefore be undertaken when assessing the impact of such arrangements on the availability of the substantial shareholding exemption, based on the specific facts of a case. A non-statutory clearance from HMRC may be advisable.

Capital structures involving preference shares and shareholder loans

When considering whether the investing company has a substantial shareholding in the company invested in, an assessment needs to be made as to how profits available for distribution to equity holders (including on a winding up) will be allocated, unless the alternative qualifying institutional investor test is being applied. (For reference, an ‘equity holder’ is any person who holds ordinary shares in the company or is a loan creditor of the company in relation to a loan other than a normal commercial loan.)

If no such profits are available, the test is instead carried out on a deemed £100 profit amount (Corporation Tax Act 2010 s 165).

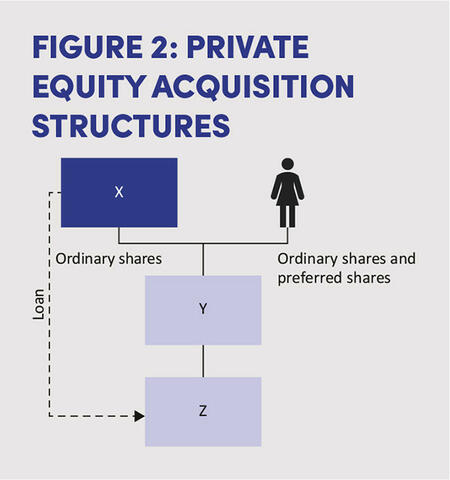

In private equity acquisition structures, it is not uncommon for holding companies to have no profits (due to income being recognised at the end of the investment; i.e. on disposal). Further, due to the difference between capital gains and income tax rates for individuals, management teams may prefer to hold preference shares instead of shareholder loans, but with equivalent economic terms (see Figure 2: Private equity acquisition structures).

- Institutional investor via X (a UK tax resident holding company): A ordinary shares and loan notes (e.g. with an 8% coupon).

- Management: B ordinary shares and B preference shares (the latter of which provide an equivalent economic return to the loan notes held by the institutional investor; e.g. an 8% preferential return).

If an assessment of the profits available for distribution to equity holders was carried out at a time when Company Y has no profits, the full £100 of deemed profit would be allocable to the B preference shares held by Management. Company X would therefore not meet the ‘Part 2: Substantial shareholding’ requirement, such that the substantial shareholding exemption would not be available.

Conclusion

The substantial shareholding exemption provides a wide-ranging exemption for capital gains arising on the disposal of shares. However, as can be seen from the above examples, care should be taken to ensure that the specific facts and circumstances of each structure are carefully considered before making an assessment as to whether the exemption is available.