Under the surface

Share this article

Helena Kanczula and Robert Harness provide an overview of the common issues encountered when undertaking tax due diligence on smaller companies

Key Points

What is the issue?

Prior to the acquisition of a company’s shares, due diligence is undertaken to ensure that any material tax risks or potential liabilities are identified. It can also be beneficial for a company preparing for sale to perform a tax ‘health check’ in advance.

What does it mean to me?

Tax concerns can often delay or frustrate the acquisition process and can lead to additional costs or indemnities, or a purchase price adjustment.

What can I take away?

This article provides a reminder of some areas commonly identified as tax risks during the due diligence of UK owner-managed businesses.

Tax concerns are often a sticking point on the acquisition of a company’s shares. Material issues can lead to extensive indemnities, a renegotiation of the purchase consideration, or a wholesale restructuring of the transaction. An appropriate level of tax due diligence work is therefore an important part of the acquisition process.

The tax due diligence of a trading company will typically cover all aspects of the company’s tax profile, including:

- Corporation tax and withholding taxes;

- Employment-related taxes, including share reporting;

- VAT.

At the most basic level, the acquirer will require comfort that the company has submitted its tax filings and settled its tax liabilities on time, and that tax computations have been prepared with reasonable care and skill. They will also assess whether there are any open HMRC enquires, and review the outcome of any enquiries or assessments raised in relation to recent periods.

Each transaction brings its own particular challenges. A discussion of these issues cannot identify an exhaustive list of risks, as every company is different, but this article provides a reminder of some areas commonly identified as tax risks during the due diligence of UK owner-managed businesses (OMBs).

Corporation tax

Tax due diligence will usually require a consideration of both the current tax and the accounting for deferred tax. A review of the data room, and discussions with the target’s management and advisors, will help to identify specific risk areas, but the following matters regularly feature.

Waiver of intercompany balances

Balances owed between connected companies will often be waived ahead of a sale on a tax-neutral basis under CTA 2009 s 354 and s 358. However, this treatment is in doubt unless the debt arises from a loan relationship, which will not be the case for all intragroup balances (as confirmed by the MJP Media Services case; also see HMRC Manuals at CFM31040).

If a waiver is anticipated, it may be advisable to put a formal loan instrument in place beforehand in order to demonstrate that a loan relationship exists.

Companies Act rules should also be considered, to ensure the waiver does not constitute an ultra vires distribution.

Connected party transactions

Although small or medium-sized companies may be exempt from UK transfer pricing requirements, if there is a possibility that connected party transactions are not priced on an arm’s length basis, this should be considered.

For medium-sized companies, HMRC may still require adjustments through the issue of a transfer pricing notice, and even small companies do not enjoy an exemption in the case of transactions with ‘non-exempt countries’ (i.e. those with which the UK does not have a qualifying tax treaty).

Even where a company is small, costs such as management charges will only be deductible if they were incurred wholly and exclusively for the purposes of the trade. If the nature and quantum of charges cannot be supported, this remains a risk area.

Overseas permanent establishments

In many industries, employees are required and able to work remotely from anywhere in the world. There is often a risk that the activities of internationally mobile employees could create a permanent establishment in another jurisdiction. A careful assessment, of the individuals’ activities and their relationship to the business of the company as a whole, may be necessary. Overseas advice may also be required as there may be non-UK payroll and VAT issues associated with a person’s activities.

Availability of tax losses

An understanding of any tax losses and their potential benefit to an acquirer is clearly important. Where the losses are significant and date back several years, it may be appropriate to investigate the provenance of the losses to confirm that they were recognised correctly and are available for future use.

If a major change in the nature or conduct of the company’s trade has taken place in the three years prior to the acquisition – or is likely to take place in the three years afterwards, the carry-forward of trading losses to the post-acquisition period will be denied.

Restrictions will also apply to pre-transaction capital losses of the target under the rules in Sch 7A TCGA 1992. As such losses could have little future benefit for many acquirers, it may be reasonable to discount them fully when valuing the target’s shares.

Section 455 tax

OMBs will typically be ‘close’ (within the definition at CTA 2010 s 439), which raises the possibility that loans made to shareholders are subject to s 455 tax. In cases where a s 455 charge has been omitted from a company’s tax return, the acquirer will need to ensure that the company makes a disclosure to HMRC.

The bed-and-breakfasting rules introduced by Finance Act 2013 introduced additional complexity and scope for error. Section 455 may also apply when a close company provides goods or services to a participator on extended credit terms; transactions with LLPs and partnerships in which a participator is a member should also be reviewed.

Degrouping charges

This is less of a concern for trading businesses than it once was, thanks to the changes to the degrouping charge mechanism made by Finance Act 2011 (degrouping charges on chargeable assets now arise in the company that sells the shares, and SSE may be available on the gain). However, these changes did not extend to the corporate intangibles regime, so degrouping charges on intangible assets could still arise in the target company. On acquisition of a group, the review of intragroup transfers in the last six years remains essential.

SDLT group relief claimed on intragroup transfers of UK land and buildings may also be clawed back if the transfer took place within the last three years.

In both cases, no charge will arise if the transferor and transferee companies both form part of a subgroup being disposed of.

Crystallisation of rollover relief

Historic gains may have been rolled over into chargeable assets, such as trading premises, currently held by the target company. Where the sale of such assets takes place as part of the post-acquisition integration process, historic gains may crystallise.

Furthermore, gains rolled over into capital expenditure on depreciating assets (e.g. fixed plant and machinery with a useful economic life of less than 60 years) may come into charge on the 10-year anniversary of the asset, i.e. before the assets are sold.

Payments made in contemplation of a change of control

Some employment-related costs may not be allowable. Where payments in compensation for loss of office are made to director-shareholders in anticipation of a sale, it is unlikely that a corporation tax deduction will be available. Cases such as James Snook & Co provide useful background.

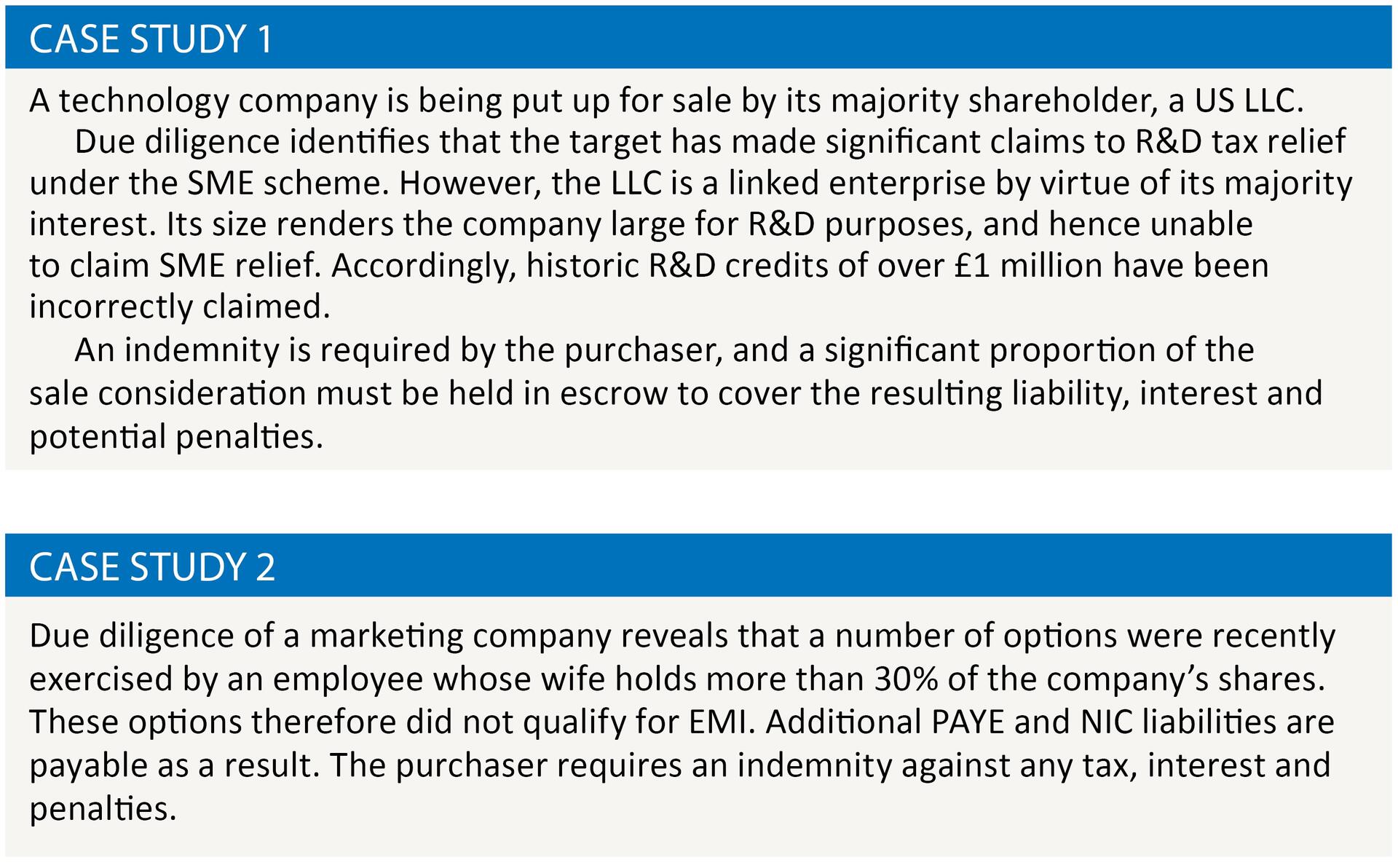

R&D claims

Where R&D relief has been claimed, the acquirer will want to confirm that historic claims include only qualifying costs and project activities are within the scope of the relief. Third parties engaged under general consultancy agreements may not fall within the strict definition of sub-contracted R&D, for example. Consumables costs should be reviewed for any ineligible expenditure (e.g. rent).

Beyond this, compliance with the broader technical conditions should be checked. Has SME relief incorrectly been claimed where Notified State Aid has been received, or where the company is undertaking R&D as a subcontractor?

It is also important to check that the results of any linked and partner enterprises have been considered when determining the company’s size for R&D purposes: is the influence of any venture capital shareholders sufficient to qualify them as linked enterprises, for example?

Withholding tax on interest and royalties

As business becomes increasingly globalised, withholding taxes on payments of interest and royalties are more likely to apply.

If withholding taxes are due, e.g. on yearly interest paid overseas, a Form CT61 must be filed, and the relevant tax paid to HMRC, within 14 days of the end of the return period. If the recipient is resident overseas, a reduced or nil rate may be available under the relevant double taxation treaty or EU Interest & Royalties Directive, although strictly HMRC consent must be obtained in the case of interest payments.

Where a failure to withhold the correct amount of tax occurs, disclosure should be made to HMRC to rectify the position.

Employment taxes

This is often the area to which most time is devoted during the due diligence process, and aspects of this work may also have an impact on the corporation tax position (e.g. the availability of a deduction under Part 12 of CTA 2009).

Contractor employment status

Where a company has made payments to individual contractors, particularly where they have been retained long-term or work on the company’s premises, care should be taken to ensure that their self-employment status can be justified. HMRC consider consultancy payments made to non-executive directors to be an area of particular risk.

In practice, many contractors operate through personal service companies. For the time being, such an arrangement should insulate private-sector employers from penalties and a potential NIC liability in the event that HMRC successfully argue an employment relationship exists. (Whether the proposed changes to the rules for off-payroll workers in the public sector will be extended to all businesses in due course remains to be seen.)

Post-acquisition, disposing shareholder-directors are often compensated with a higher salary in lieu of the dividends they took before. The change in the company’s PAYE profile may well prompt a payroll compliance review from HMRC. Contractor status often forms a key part of such reviews.

EMI options and employment-related securities

Many businesses seek to incentivise key staff through share option schemes: EMI schemes are often popular with smaller companies, with options vesting immediately prior to the sale.

Implementation of such schemes ought to be straightforward. However, there are a number of pitfalls in the legislation and if it becomes apparent that the options fail to qualify for EMI – either because of a technical failure at the time of issue or a subsequent disqualifying event – staff will lose the tax benefits they had expected. The payroll costs associated with the exercise of non-qualifying options could be significant.

Common areas which it is prudent to review include:

- The overall purpose of the scheme: where an option scheme has been implemented shortly before the sale, it may fail to qualify for EMI on the grounds that it is a means to return more cash in capital form rather than to retain and motivate staff. This may be relevant where directors already hold shares that meet the Entrepreneurs’ Relief conditions, and have been granted further options.

- Whether options were notified within 92 days after grant.

- For options registered online, whether working time declarations have been made: employees receiving EMI options are required to make an explicit declaration that they meet the relevant working time requirements (broadly, that they work for the employing company for at least 25 hours a week, or 75% of their working time, if less).

The taxation of employment-related securities is a complex topic on which extensive amounts could be (and have been) written. The specific risks of each scenario will be dependent upon the particular circumstances but, as many of the relevant issues are highly subjective – valuations, whether restrictions apply, whether the securities are employment-related in the first place, and so on – a careful review will almost always be warranted.

Benefits-in-kind

The rules relating to benefits in kind are scattered with pitfalls. Where potential non-compliance is identified, it can be time-consuming to rectify the position – any problems will often not be material in themselves, but point to the quality of the company’s compliance more generally.

Common areas of scrutiny include:

- Directors’ loan accounts;

- Application of the £150 staff entertainment exemption for annual events;

- Whether VAT has been included in P11D entries; and

- Whether a PAYE Settlement Agreement has been put in place to cover expenses that are minor, irregular or impracticable to allocate to individual employees.

VAT

A review of a company’s VAT affairs will typically focus on whether returns have been submitted correctly and on time. Confirmation of options to tax made in respect of commercial property will also be sought. Where relevant, it is also important to ensure that partial exemption calculations have been prepared correctly.

Other matters that it would be prudent to consider include the following:

Irrecoverable VAT

It is good practice to ascertain whether VAT has been recovered on expenditure in respect of which it is not correct to do so, such as the costs of entertaining.

Capital Goods Scheme

The Capital Goods Scheme most often applies to property-related capital expenditure (e.g. fit-out costs). Where the value of such expenditure exceeds £250,000, it is necessary to review the extent to which the building has been used to make exempt supplies (or for non-business activities) for up to ten years following the acquisition. Where there has been a change of use, or a change in the mix of taxable and exempt supplies, part of the input VAT initially recovered may need to be repaid.

This is particularly relevant where the business undertaken from the premises in question is partially exempt, or will be post-acquisition.

EC Sales and Intrastat returns

Where EC Sales Lists and Intrastat returns have not been filed, significant penalties may arise. Failure to make Intrastat returns may even result in a prison sentence.

Final thought

In most company acquisitions, due diligence is an essential step. However, it may also prove beneficial for a company preparing for sale to perform a tax ‘health check’ in advance, to help ensure that tax matters do not disrupt the completion timetable.