What is a disbursement?

Share this article

Neil Warren highlights the important differences between an expense recharged by a supplier to a client for his own costs and a genuine disbursement that is not subject to VAT

Key Points

What is the issue?

If an expense paid by a supplier belongs to his customer, then the recharge to the customer will not be subject to VAT if certain conditions are met.

What does it mean to me?

It is important to be clear that there is a big difference between a genuine disbursement and a recharge of a supplier’s own expenses for e.g. travel and accommodation. The latter will be subject to 20% VAT in most cases.

What can I take away?

HMRC have the power to correct errors going back four years, so a review of accounting procedures for dealing with disbursements might prove worthwhile to avoid future problems.

The idea for this article was prompted by a recent First-tier Tribunal case partly won by the taxpayer about whether a car repair business could treat recharges of MoT testing fees to vehicle owners as a disbursement with no VAT charged on sales invoices, or whether the deficiencies in his invoicing procedures meant he was liable to account for VAT on the payments made by customers. The issue of VAT and disbursements is one that many clients find confusing and they often think (incorrectly) that a recharge of their own business expenses (e.g. mileage or rail fares) is a disbursement. I’ll consider this issue and also review the case of Ellon Car Clinic Ltd (TC5813) about the MoT fees.

What is a disbursement?

The key issue with the ‘expense or disbursement’ challenge is to consider whether an expense belongs to the supplier’s customer rather than the supplier. To give an easy example, when a solicitor deals with a house purchase on behalf of a client, he will often pay for expenses that belong to the client e.g. local authority search fees, Stamp Duty Land Tax, land registry fees. These expenses will eventually be paid for by the house buyer so they are clearly the buyer’s expenses and not the solicitors. As long as the solicitor adopts certain procedures on his sales invoices, these disbursements will not be subject to VAT.

However, as a contrast, if I do some consultancy work for a client in London, and the client agrees to pay my train fare, mileage expenses or hotel accommodation for my travel to and from London, this is not a disbursement situation – it is effectively an increase in my standard rated consultancy fee to cover my out of pocket expenses. See Architect charging expenses.

Conditions for disbursements

Going back to the solicitor acting for a house buyer, he needs to be strict as far as his procedures are concerned to ensure there are no VAT problems in relation to disbursements charges:

- He must ensure that all relevant costs belong to the buyer rather than his own business and he must have acted as an agent for the buyer when he paid the various third parties e.g. local authorities, land registry office etc.

- The buyer must have received and used the goods or services provided by the third parties and the buyer was responsible for paying the third parties and authorised the payments to be made.

- The payments must be itemised separately on the solicitor’s invoice(s) and he will only recover the exact amount paid to the third parties.

HMRC VAT Notice 700, para 25.1

As far as record-keeping is concerned, the business charging disbursements without adding VAT must be able to satisfy HMRC on two issues, if so requested:

- Evidence of the actual payment made to the third party supplier, with a document confirming the detail and amount.

- HMRC must be satisfied that no input tax has been claimed on the disbursement by the business recharging it to his customer. There might be scope for the final buyer to claim input tax (if the expense relates to taxable supplies etc.) because the goods or services belong to that person or business.

MoT tribunal case

The priority is to ensure that a business only charges its customers the exact cost of a disbursement and does not apply a mark-up or profit margin. So if our solicitor pays £80 for a land registry fee but charges his client £100 on his sales invoice, HMRC will usually seek to assess tax on the £20 profit margin and, in some cases, the full £100 fee. It would not be a problem if he charged £80 as a disbursement and then a separate fee of £20 for an administration charge – the latter would be standard rated but not the disbursement.

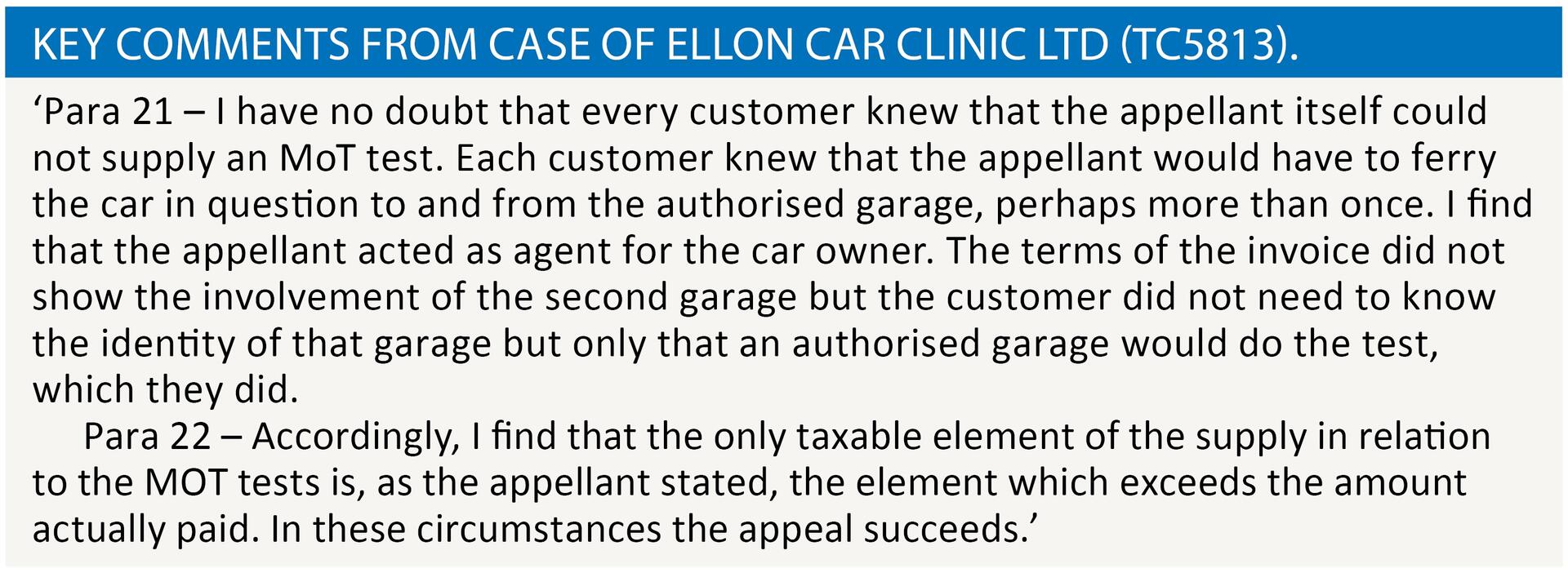

This was the problem in the case of Ellon Car Clinic Ltd (TC5813) that I mentioned in the opening paragraph, concerning MoT recharges. The company was not licenced to carry out MoT tests on customers’ vehicles, so subcontracted these tests to other garages, paying between £40 and £54.95 per test. It charged its customers a standard fee of £49.95 (no VAT), which HMRC assessed as being subject to 20% VAT, i.e. the disbursement conditions had not been met. The problem was made worse by the fact that the company did not separately itemise the testing fees on its sales invoices. However, the tribunal supported the taxpayer on the basis that an agency arrangement was evident and the supply was clearly between the testing garage and the customer, a fact of which all parties were aware. The company was only subject to output tax on the profit margin ie for those tests that cost less than £49.95. The balance of the payments was outside the scope of VAT as a disbursement. No output tax was due on deals where the company made a loss. See Key comments from case of Ellon Car Clinic Ltd (TC5813).

As a further twist to the tale, the tribunal noted that VAT Notice 700 (section 25) was ‘less than a model of clarity or good exposition of law’ and suggested that revisions were necessary. The judge commented that the same issue had arisen in three earlier cases and that the guidance should set out very clearly ‘how garages should avoid the trap of being treated as a principal.’

VAT registration

To share a tale with you that did not have a happy ending, HMRC identified from the self-assessment tax returns of a business that it should have registered for VAT many years ago as a marketing consultant. The returns had shown sales of about £90,000 for the previous five years, i.e. above the registration threshold. The business accountant replied to HMRC with the following two reasons as to why registration was not needed (and the client did not want to register anyway because his customers were mainly exempt businesses that were unable to claim input tax):

- About £5,000 of annual sales related to overseas business customers in other EU countries and should therefore be excluded from the value of taxable sales as far as the registration limit is concerned.

- About £10,000 of sales related to the travel and hotel expenses of the consultant, which was recharged on sales invoices to his customers.

The good news is that the accountant was right above the overseas services – these are outside the scope of VAT under the general B2B (business to business) rule. Any sales that are outside the scope of VAT or exempt are ignored as far as the registration threshold is concerned. However, his thoughts about the travel and hotel expenses are misguided – as we established with Example 1, a recharge of a supplier’s expenses to his customer forms part of his fee. So with the figures I have used above, the relevant figure for the VAT registration threshold is £85,000, i.e. gross sales less the EU fees. And to rub salt into the wounds, when it comes to late VAT registration, HMRC have the power to backdate the registration up to 20 years.