Year by year

Share this article

Neil Warren considers the role of advisers in producing year-end accounts and ensuring VAT returns are correct

Key Points

What is the issue?

It is important to ensure that the turnover figure on the annual accounts of a business is reconciled with the declared outputs on VAT returns for the same period. The VAT control account balance should also be checked against the liability on the return.

What does it mean to me?

It is better for advisers to reconcile annual accounts and VAT return figures each year and investigate differences rather than for HMRC to identify a problem many years later.

What can I take away?

There are many reasons for differences that do not mean the business has understated sales on its VAT returns and should be assessed for additional output tax.

I was recently involved with a VAT problem that HMRC identified on a compliance visit, namely a difference in the sales figure on the annual accounts of a business compared with the outputs declared on its returns. The figure on the accounts was higher. Please make sure you are sitting down before I reveal the total discrepancy. Ready? Over two financial years it was £700,000!

You might be wondering why the accountants failed to identify the problem as soon as the first accounts were produced rather than wait for it to come to light on an HMRC visit two years later. And did the discrepancy not produce a creditor balance in the nominal ledger that was much higher than the declared liability on the VAT return? Was this checked?

I’ll let you consider these questions but the message is clear, namely that VAT is far too important to ignore when producing year-end accounts.

Case study

Let us create an imaginary business that has three units in north-west England trading as a wholesaler of paint and wallpaper. All sales are invoiced to retailers and about 10% of sales are exported. A comparison between the turnover figure on the year-end accounts shows sales of £2m compared with outputs of £1.5m on the VAT returns for the same period. What is the solution to this problem?

A comparison between turnover and outputs is an essential check, as shown in the First-tier Tribunal (FTT) case of Wholesale Clearance UK Ltd, more of which later. It is also important to compare the VAT control account balance in the nominal ledger with the liability on the return at the end of each VAT period. A year-end check should be easy because most businesses have VAT periods that coincide with their financial year.

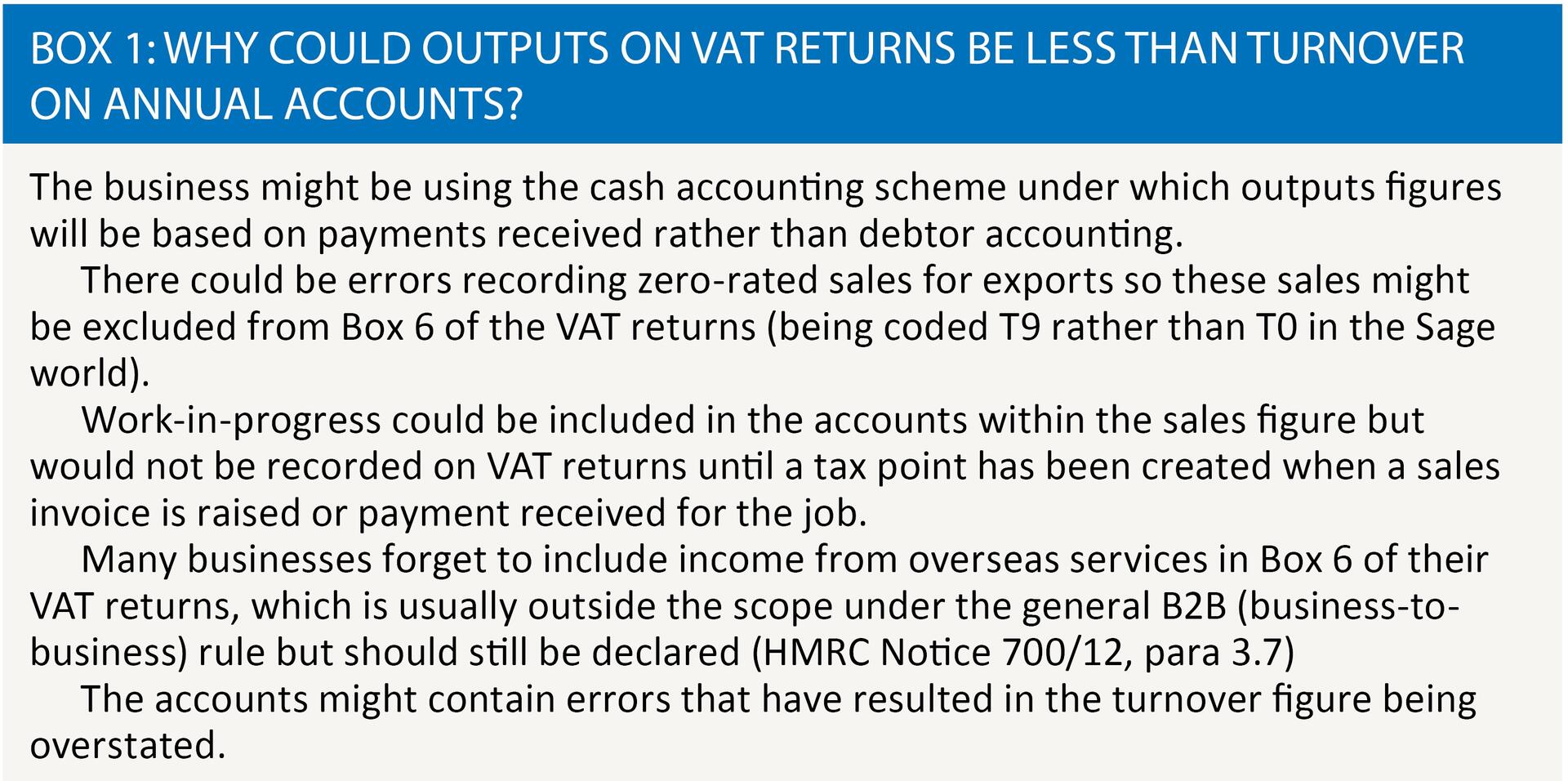

So as a practical challenge, what are the possible reasons why there could be a difference between the accounts and VAT returns of our wallpaper business, which will not result in extra output tax being payable? See Box 1 for suggestions.

Wholesale Clearance UK Ltd

As the saying goes, it is better to nip a problem in the bud before it gets out of control and more difficult to solve with the passing of time. The recent FTT case involving Wholesale Clearance UK Ltd (TC5027) highlights this point.

An HMRC officer compared the turnover on the accounts with the declared outputs on VAT returns for the years ending 31 July 2009 to 2011. An assessment was raised for £27,768 because more sales were recorded in the accounts than on the returns. It was later reduced to £17,614 because only the final quarter of 2009 was in time under the four-year assessment rule. The assessment was raised on the basis of VATA 1994, s 73(1), which gives officers the power to ‘assess the amount of VAT due … to the best of their judgment’.

The accountant was not available to explain the differences to the tribunal because of a ‘personal tragedy’ and the officer did everything expected of him to produce a fair assessment including taking into account the company’s zero-rated export sales (about 11% of total sales). The appeal was dismissed.

A key learning point from this case is that it can be difficult to back pedal and explain differences that happened many years earlier. This is the reason for my suggestion that the ‘turnover v outputs’ check should be carried out each year.

True story

The scenario of the wallpaper business is based on an inspection I did about 25 years ago in my Customs and Excise days. Computer systems were not as sophisticated as they are today, and the reason for the £500,000 difference was that the sales (and VAT) from one of the three trading branches escaped the VAT returns because of a computer software problem.

But the situation was made worse by the fact that the finance director realised there was a problem because the VAT creditor balance in the nominal ledger was always higher than the liability on the computer-generated VAT return. So he made a note to debit the VAT account at the end of each quarter and post a credit entry to a ‘balance sheet suspense account’ so that the control account balanced to the VAT returns. He planned to look into the reason for the differences when he had more time. You are probably thinking the same as me: that it was a good job it happened 25 years ago before the current penalty regime for careless and deliberate errors was in place!

Second tribunal case: basic error

The FTT case of Ppig Ltd (TC4655) was not directly concerned with the figures on the annual accounts but relevant to an error that should have been identified many years before HMRC discovered it.

The problem was that the director, Mr MacMillan, had claimed input tax on his UK returns for five successive years in relation to VAT paid in other EU countries, which HMRC rightly disallowed on a compliance visit. The officer raised an assessment for £67,178 plus interest for the previous four years. The company should have claimed overseas VAT through the EU refund system, under which claims must be made within nine months of the end of the previous calendar year. This caused the company a big problem because it was out of time in most cases as far as a potential claim was concerned.

My initial thought was to wonder why Mr MacMillan’s accountant did not alert him to the errors. But after a period of reflection, I realise how very different things are in the modern global world when producing accounts. A lot of work is now done by electronic communication, a very different approach from the old days of a bundle of records and invoices being brought into the office in a Tesco carrier bag.

Conclusion

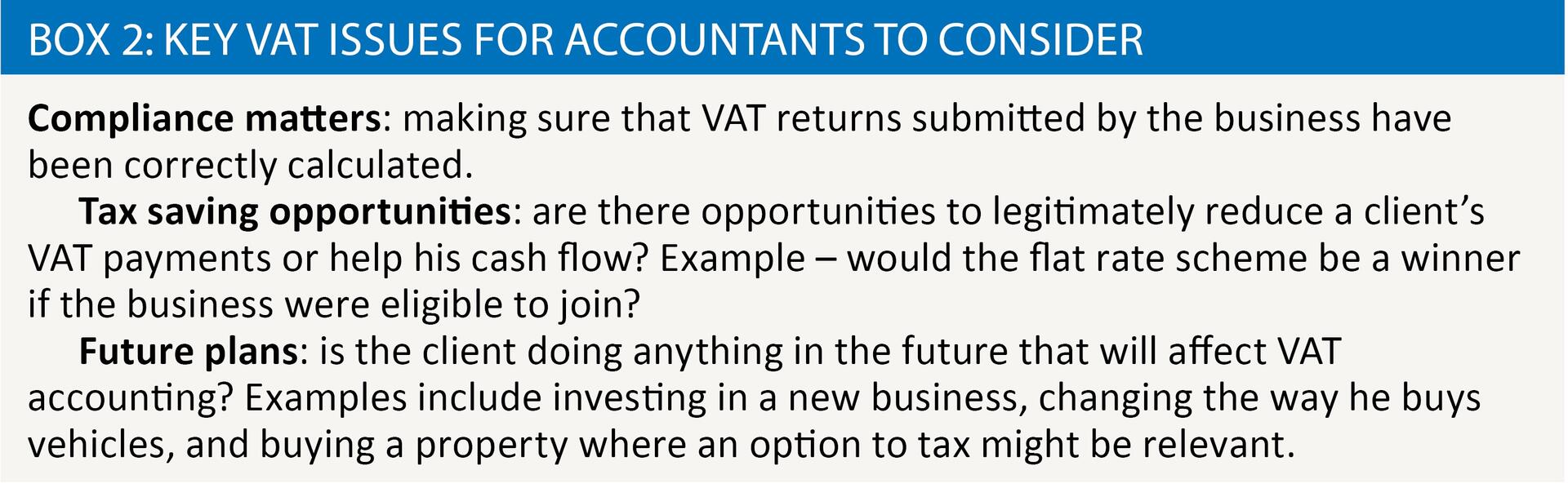

As far as the nation’s favourite tax is concerned, there are three main objectives that are relevant when we try to give a good service to clients as highlighted in Box 2. I hope these give food for thought.

As a final tip, do not assume that HMRC officers are specialists in analysing accounts or that their conclusions are always correct. A colleague I worked with in C&E about 30 years ago thought that the ‘profit on asset sales’ figure on a profit and loss account related to a monetary profit on the asset, ie, selling price more than cost. In the case of used motor cars, he assessed this ‘profit’ as VAT inclusive within the second hand margin scheme. It took a long time for him to understand about depreciation and the difference between a book profit and monetary profit. But we got there in the end!