VAT for charities

Share this article

Neil Warren highlights some important VAT concessions available to charities on their overheads and also the exemption on fundraising income which extends to non-profit making bodies

Key Points

What is the issue?

Charities do not get special VAT treatment but they do benefit from certain concessions within the legislation, e.g. a landlord’s option to tax can be overridden in some circumstances on property rented by the charity.

What does it mean to me?

Many tax advisers serve on charity and club committees and should be aware that overcharges of VAT can be corrected going back four years by asking the supplier for a credit.

What can I take away?

Don’t forget that the VAT exemption on income from fundraising events extends to events held by non-profit making organisations as well as charities, e.g. most sports clubs owned by members and run by a voluntary committee.

VAT challenges for charities

A very common question I get asked by accountants is as follows: a client is doing some work for or selling goods to a charity and the charity has told the client not to charge VAT because charities are exempt from paying the tax. The finance officer or treasurer of the charity will happily wave a charity number at the client with great enthusiasm and totally believe what he or she is saying. Unfortunately, such claims of universal VAT exemption are wildly inaccurate!

The challenge for advisers is to be aware of the concessions available to charities in the VAT legislation, which mean that some goods and services they pay for are not subject to VAT or subject to the lower rate of 5% in some cases. These concessions are very worthwhile and I will share some in this article. I will also include some analysis about the exemption for fundraising income and highlight the important fact that this exemption is available to non-profit making organisations as well as charities, e.g. a members’ golf club holding a dinner to raise funds to buy a new lawn mower would qualify.

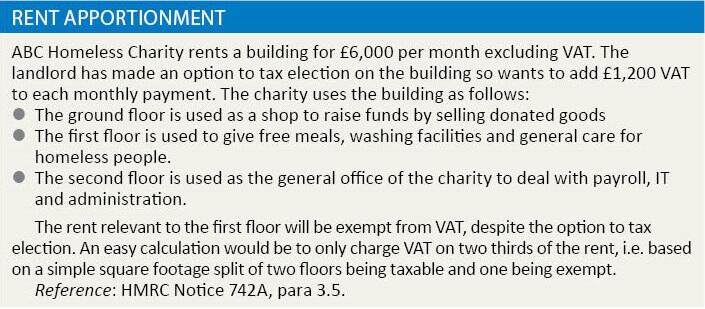

Rental charges

On the basis that rent and wages are often the two main overheads of many charities, let me start with the issue of rent, and the potential to override an option to tax election made by a landlord.

The starting point is that a landlord who has made an option to tax election on a building must charge 20% VAT on all income earned from the building, unless it relates to residential property. So what is the position as far as charities are concerned and an override of the landlord’s election?

- The charity must be using the building (or part of the building if there are clearly defined areas) for a relevant charitable purpose other than as an office for general administration purposes, i.e. the good causes of the charity for which it was established.

- The charity does not need to complete a certificate but the landlord should ask the charity to certify its use of the building in writing and the letter should be signed by a senior officer of the charity, e.g. CEO, Trustee etc.

- If a building is partly used for charitable purposes and partly for business purposes (e.g. a charity shop) and the different areas are clearly defined, then the landlord should apportion the rent in a fair and reasonable manner – see Rent apportionment.

Image

Advertising costs

To develop the theme from the previous example, the trustees of ABC Homeless Charity have decided to launch an advertising campaign to encourage donations from the general public and also seek more donated goods for its shop. What is the situation with the VAT charged on the cost of the advert by, say, a newspaper, radio station or website?

The good news is that there is a specific HMRC publication on this subject, Notice 701/58. And the relevant legislation for the zero-rating of charity advertising is contained in VATA1994, Sch 8, Group 15, Item 8. However, there is a twist to the tale:

- A supply of advertising to a charity registered with The Charity Commission (or to a charity which is not registered with the Commission but is recognised for its charitable aims by HMRC) is zero-rated. This includes advertising relevant to the business activities of the charity ie the shop in my example.

- However, many charities carry out their business activities under a separate trading company, which is not a registered charity, even though it will be owned by the charity and usually gifts all of its profits back to the charity. These companies must pay VAT on their advertising costs because they are not a charity.

- A condition of zero-rating is that the advert must ‘communicate with the public’ (see paras 3.1 and 3.2 of Notice 701/58).

- The zero-rating extends to the costs of designing an advert but not to the general services of designing or managing a charity’s website.

Note – for more analysis about the question: ‘What is a charity?’–see para 2.2 of HMRC Notice 700/58.

Fuel and power

Supplies of gas and electricity to a charity for non-business purposes are subject to 5% VAT when charged by the fuel supplier. But what happens, I hear you ask, if a building is partly used for charitable purposes and partly for business purposes, such as the building used by ABC Homeless Charity considered above?

- The charity must certify to the fuel supplier the proportion of the building that qualifies for the reduced VAT charge, i.e based on its non-business use.

- If the qualifying part of the building exceeds 60% of the total building use, then the entire supply of fuel and power will be subject to 5% VAT. This is a very good outcome.

- Reference: HMRC Notice 701/19, section 3.

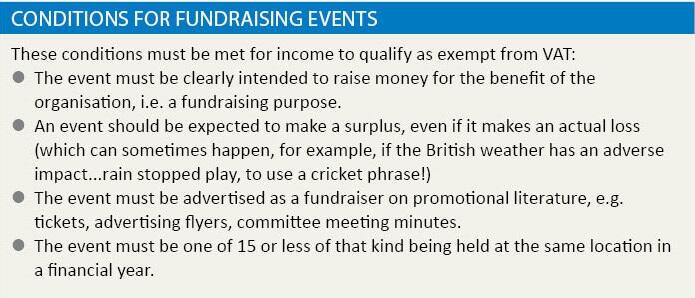

Exemption on fundraising income

To finish with an income concession, a fundraising event organised by a charity or non-profit making body will qualify for exemption for the event in question (VATA1994, Sch 9, Group 12). The exemption applies to trading subsidiaries wholly owned by a charity and also not for profit bodies such as sports clubs and most professional associations. An organisation can host up to 15 events of the same type at the same location in its financial year, which is good news for, say, a monthly car boot sale hosted at the ground of a local football club. Unfortunately, if 16 or more events are held in a financial year, then none of the events qualify for exemption. The exemption covers all income generated at the event, including admission fees, the sale of commemorative items and food. However, similar events can be ignored for the 15 event limit if total gross takings in a week are less than £1,000 (Note 5, Group 12, Sch 9, VATA 1994). The challenge is to ensure that all events meet the necessary criteria – see Conditions for fundraising events.

To share a tale, a VAT registered cricket club I was involved with many years ago wisely took advantage of the fundraising exemption for some events, and the committee also recognised that the direct costs of the events were input tax blocked under the rules of partial exemption, e.g. catering fees, cabaret cost, venue hire. However, they did not realise that because the input tax numbers were kind, they were able to still claim this input tax using the partial exemption de minimis rules at the end of their partial exemption tax year (they were partly exempt in the quarter when the event was held but de minimis when the annual adjustment was carried out). This subject is beyond the scope of this article but see VAT Notice 706, section 11 and also my article for Tax Adviser in April 2017 (page 34).

Final tip

If you act for charity clients and have identified some VAT overpayments in this article, then the challenge is to identify any errors and go back to the supplier and ask for a VAT credit for supplies made to the charity in the last four years, i.e. the error correction period we have in the world of the nation’s favourite tax. The supplier will not be out of pocket (hopefully) because he will reduce the output tax on his next VAT return. Any overpayments that extend beyond four years are unfortunately out of time and cannot be adjusted.