Alphabet Soup

Share this article

Gordon Buist considers the definition of a ‘personal company’ for the purposes of entrepreneurs’ relief

Key Points

What is the issue?

Entrepreneurs’ relief (ER) on the disposal of shares has become more complex following changes introduced in FA 2019. A major amendment has been made to the definition of ‘personal company’, which has extended the 5% test.

What does it mean to me?

The new economic interest tests are an added complexity when advising on the availability of ER in all but the most straightforward of disposals.

What can I take away?

The use of seemingly straightforward terminology with highly prescriptive meanings for tax purposes highlights the importance of always considering the detailed legislation when advising clients on ER.

Entrepreneurs’ relief (ER) was introduced by former chancellor Alistair Darling in 2008 as the replacement for business asset taper relief. In simple terms, ER now operates by applying an effective 10% rate of capital gains tax on gains arising on a qualifying disposal of business assets, subject to a lifetime limit of £10m.

The relief: a refresher?

ER is available on disposals of shares in a trading company if the conditions in TCGA 1992 ss169H-169SH are satisfied. In summary, an individual will qualify for ER in relation to shares in a trading company if, throughout the qualifying period of two years ending on the date of disposal:

- the individual is an officer or employee of the company, or a company within the same group where the shares are in a holding company; and

- the company is a ‘personal company’ in relation to the individual.

If the company has ceased to trade without continuing to be a member of a trading group, the two year qualifying period will end on the date when the trade ceases, provided the disposal of shares is within three years of the cessation date.

A ‘personal company’ in relation to an individual was broadly defined as a trading company, of which the individual held at least 5% of the ordinary share capital, which by virtue of that holding entitled them to at least 5% of the voting rights in the company (the ‘5% test’). I do not intend to consider the definition of a trading company in this article.

Autumn Budget 2018

The Chancellor reaffirmed in his Autumn Budget speech that entrepreneurs’ relief was here to stay, despite some calls for its abolition.

However, two important changes were announced. The minimum qualifying period for ER was increased from 12 months to two years. A second change was apparently intended to address an identified abuse in the initial draft but could have potentially precluded a claim for ER by the majority of family company owners.

Personal company: FA 2019 changes

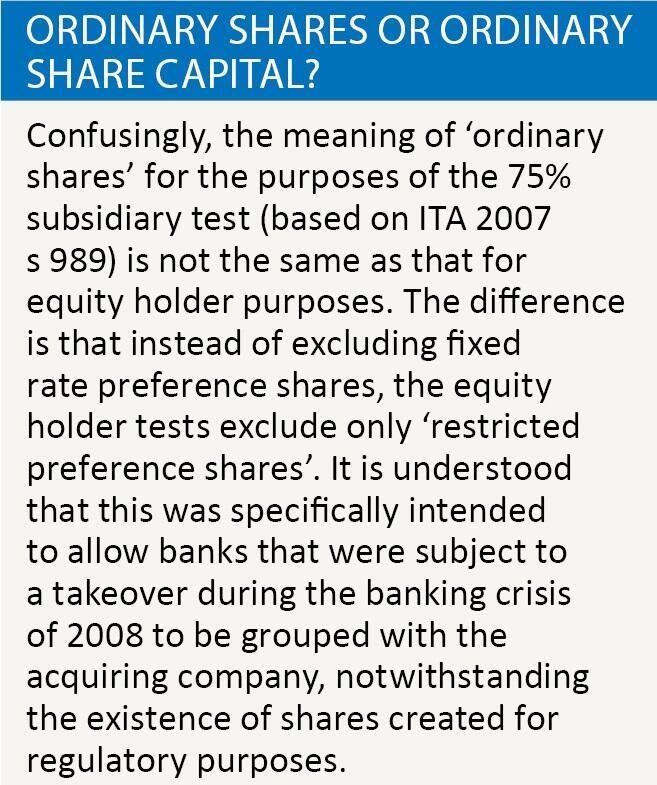

A major amendment has been made to the definition of ‘personal company’, which has extended the 5% test. FA 2019 amended the legislation in TCGA 1992 s 169S(3), which now states that a company is a ‘personal company’ in relation to an individual if:

- the individual holds at least 5% of the ordinary share capital of the company;

- by virtue of that holding, at least 5% of the voting rights in the company are exercisable by the individual; and

- either or both of the following conditions are met:

- by virtue of that holding, the individual is beneficially entitled to at least 5% of the profits available for distribution to equity holders and, on a winding up, would be beneficially entitled to at least 5% of assets so available; or

- in the event of a disposal of the whole of the ordinary share capital of the company, the individual would be beneficially entitled to at least 5% of the proceeds.

The tests in s 169S(3)(c) are referred to as the ‘economic interest’ tests. In its original form, the ‘economic interest’ test was too complex and would have denied ER in many circumstances that were not within the stated policy intention. The problem was largely the result of importing the definition of ‘equity holders’ from the legislation defining a ‘group’ for the corporation tax group relief provisions. Many practitioners believe that the ‘equity holder’ concept is not fit for its newly intended purpose, nor easily applied in the context of a claim for ER by an individual. Thankfully, the test in s 169S(3)(c)(ii) was added into the Finance (No. 3) Bill 2018, following representations from the CIOT and all of the major professional bodies.

This article explores how the ‘economic interest’ test in TCGA 1992 s 169S(3)(c)(i) can apply in practice (the same test also applies in the substantial shareholdings exemption).

5% test: ordinary share capital

An individual must hold at least 5% of the ordinary share capital of the company. Ordinary share capital is defined in ITA 2007 s 989 as meaning ‘all the company’s “issued share capital” (however described), other than capital the holders of which have a right to a dividend at a fixed rate but have no other right to share in the company’s profits’. It is nominal value that is relevant, rather than the number of shares in issue (Canada Safeway v IRC [1973] 1 CH 374).

HMRC recently published guidance on their interpretation of the meaning of ‘ordinary share capital’ in the Company Taxation Manual at paras CTM00509 to CTM00516, which includes examples of different types of preference shares and highlights those that might be regarded by HMRC as ‘ordinary share capital’ for tax purposes.

In practical terms, the fact that certain preference shares may be regarded as ‘ordinary share capital’ for tax purposes, but not for accounting purposes, creates uncertainty as they are often accounted for, and operate, as de facto debt instruments. It is also often unclear whether an individual holds the necessary 5% of ordinary share capital, particularly where a company has external investors that hold preference shares or complex loan notes.

Moreover, certain fixed rate preference shares may be treated as ‘ordinary share capital’ for CGT purposes; for example, a fixed rate preference share, where the coupon compounds if not paid could be treated as ordinary share capital. Similarly, if the coupon is calculated as a fixed percentage of the aggregate of subscription price and accrued unpaid dividends, rather than the nominal value of the preference shares, the preference shares will be treated as ordinary shares (see S Warshaw v HMRC [2019] UKFTT 268).

5% test: profits or assets available for distribution to ‘equity holders’

From 29 October 2018, it is no longer sufficient for a shareholder to satisfy the 5% test in relation to only their holding of ‘ordinary share capital’. The shareholder must now also satisfy the 5% ‘economic interest’ test, potentially against an entire pool of ‘equity holders’ in the company.

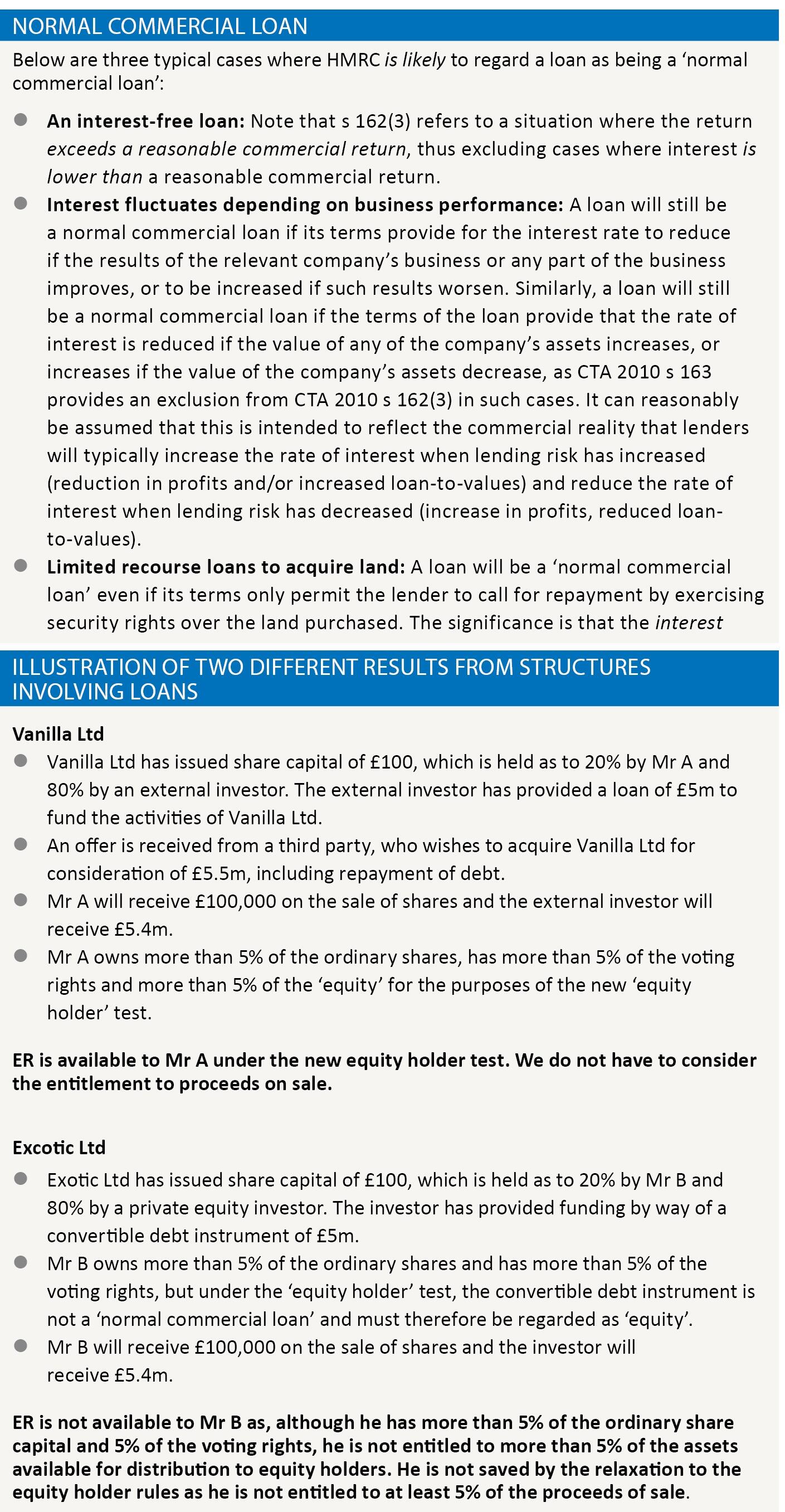

An equity holder is any person who holds ‘ordinary shares’ in the company or is a creditor of the company as regards any loan that is not a ‘normal commercial loan’.

The starting point is that a company’s ‘equity holders’ will include all of its ordinary shareholders. However, without carrying out a more thorough analysis, it is not possible to determine an individual’s ER status without considering the 5% ‘economic interest’ test by reference to either the share of proceeds on a hypothetical sale, or an entitlement to at least 5% of the profits or assets available for distribution to ‘equity holders’.

Equity holders

An ‘equity holder’ includes any holder of convertible loan notes, warrants or other debt securities with ‘equity like’ features, as well as any person who is a loan creditor in respect of a loan that is not a ‘normal commercial loan’.

The inclusion of loan creditors in respect of a loan that is not a ‘normal commercial loan’ would, prima facie, result in many company directors being treated as equity holders on the basis that they are often in the position of making loans on terms that are not particularly commercial, such as providing an interest-free loan to a company. However, a ‘normal commercial loan’ is defined in CTA 2010 s 162 as a loan of, or including new consideration:

- which does not carry any right to the acquisition of shares or securities;

- if the loan is convertible, it can only convert into:

- restricted preference shares which, if they are convertible, convert only into shares or securities in the company’s quoted parent;

- securities on normal commercial terms which, if they are convertible, convert only into shares or securities in the company’s quoted parent; or

- shares or securities in the company’s quoted parent;

- which does not entitle the loan creditor to any amount by way of interest which depends to any extent on the results of the company’s business or any part of it, or on the value of any of the company’s assets, or which exceeds a reasonable commercial return on the new consideration lent; and

- in respect of which the loan creditor is entitled, on repayment, to an amount which either does not exceed the new consideration lent or is reasonably comparable with the amount generally repayable under the terms of issue of securities listed on a recognised stock exchange.

Conclusion

Readers must consider the ‘economic interest’ tests carefully when considering the availability of ER on a sale, particularly where the vendor will not receive 5% of the proceeds on a sale, in which case it is necessary to consider the ‘economic interest’ tests in TCGA 1992 s 169(3)(c) in more detail. Readers would be well advised to consult the legislation, particularly where terms that prima facie have a plain English meaning are actually prescriptively defined in legislation.

The new requirement in TCGA 1992 s 169S(3)(c) will be much more difficult to meet for entrepreneurs holding shares in companies that have issued complex financial instruments or preference shares, which may typically be the case following a management buyout or private equity investment in the company.