In black and white

Share this article

Anthony Nixon explores some tax reliefs for charitable giving

Key Points

What is the issue?

A summary of some of the main income tax, CGT and IHT charity reliefs sparks memories of some great British comedy films of the 1940s and 50s.

What does it mean to me?

The article explores what may for some be less familiar features of the reliefs, and how they can be used to benefit causes close to a client’s heart.

What can I take away?

More knowledge of the range of reliefs and of the particular circumstances when they can be useful.

CGT reliefs: The Ladykillers

I will never forget Mrs Wilberforce.

This wasn’t, of course, her real name, but she could have been the twin sister of the heroine of that great Ealing film The Ladykillers. If you are not familiar with the film, look it up immediately. You will not regret your encounters with Alec Guinness’s sinister false teeth, Peter Sellers and Herbert Lom among the villains (long before their double acts in the Pink Panther films) and the sublime Katie Johnson as Mrs W herself.

My Mrs W came to mind when I was asked to give a talk to supporters of Pallant House Gallery in Chichester. Pallant House is a near neighbour of my firm’s Chichester office and must be one of the top galleries of modern art anywhere outside London. We have been delighted to assist it throughout its existence.

About 35 years ago I helped ‘Mrs Wilberforce’ with a gift of a painting, worth some tens of thousands of pounds. A gift of an asset to a charity, is a no-gain/no less transaction (TCGA s 257) so Mrs W incurred no CGT on her gift. That charity wasn’t an art gallery, so it then sold the painting, taking advantage of TCGA s 256, under which a gain is exempt from CGT, ‘if it accrues to a charity and is applicable and applied for charitable purposes.’ In addition, of course, Mrs W’s gift to the charity was exempt from IHT.

I began my talk at Pallant House with this story and was delighted to find one gentleman, sitting in the front row, was glowing with pleasure. He had realised that he could give a painting from his own collection to Pallant House itself without tax. In this case, the gallery was keen to keep and display the painting.

Gift Aid: Whisky Galore!

Gift Aid is probably the most often encountered charity relief. I do not examine Gift Aid in detail in this article, but just note a few points.

November’s budget announced a simplification of the rules on ‘benefits associated with a gift’. These rules, in ITA ss 417-49, restrict the benefits a donor can receive from a charity while still qualifying for Gift Aid. A review began as long ago as September 2014, since when there have been two formal consultations. The final response to these consultations was published by the government in December. Legislation, including enactment of existing Extra-Statutory Concessions in this area, is due to be in Finance Bill 2019, so will, presumably, come into force on 6 April 2020.

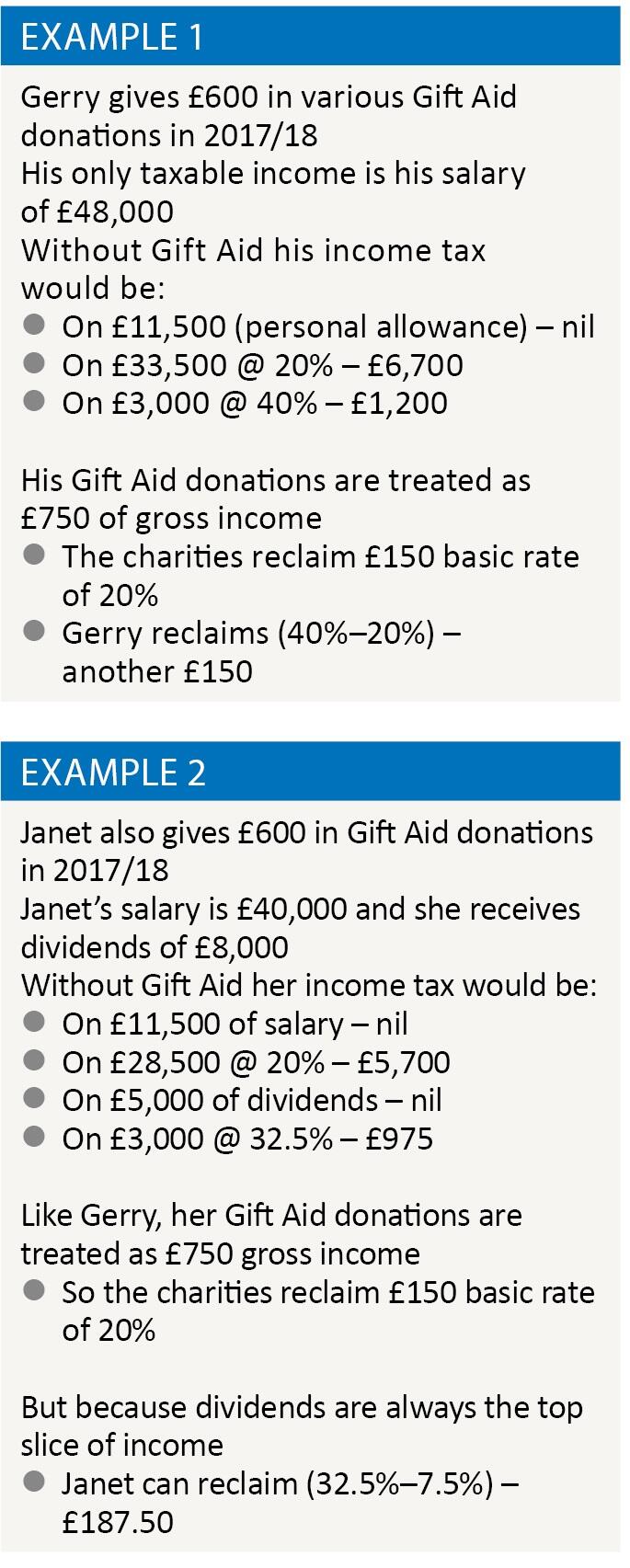

Most of us remember that a donor can only claim Gift Aid if they pay sufficient tax in the tax year they make the gift. The theory is that the donor has deducted basic rate tax from a Gift Aid donation, and it is this tax that the charity reclaims. I had forgotten that Gift Aid can be franked by capital gains tax, as well as by income tax and that, in some circumstances, it is possible for a donor to use tax he has paid in the previous tax year.

Of course, it is more valuable to use income tax, because the donor then gets a rebate of any rates higher than the basic rate. Different rates of tax for dividends can lead to some curious results. See examples 1 and 2.

Higher income tax reliefs: Passport to Pimlico?

Less well known than Gift Aid are the generous reliefs for gifts to charity of ‘qualifying investments’ and ‘qualifying land’ (ITA s 431 onwards). Where these gifts comply with the rules, the entire value of the gift can be set against the donor’s taxable income for the year.

Most quoted investments (both in the UK and abroad) can be ‘qualifying investments’. ‘Qualifying land’ (meaning both land and buildings) must usually be a freehold in the UK.

Anti-avoidance rules apply if:

- the investment given away was owned by the donor for less than four years; or

- the investment was acquired as part of a scheme with a view to obtaining this relief.

In the case of land there is a ‘disqualifying event’, and the relief is cancelled, if, before the fifth anniversary of 31 January following the tax year of the gift, the donor becomes entitled to any rights over the land given.

Gifts of part shares of land do not qualify; and co-owners must all give their interests in the land to the charity for any of them to qualify for relief.

Tainted donations: Hue and Cry

The tainted donation rules, in ITA ss 809ZH to 809ZR, withdraw, for individuals, all the income tax and CGT reliefs I have referred to in this article where, broadly, a donor plans arrangements designed to give him a financial advantage. In some cases, the rules impose an additional income tax charge.

Official guidance on the rules can be found on GOV.UK.

IHT and non-UK charities: Another Shore

One of the curious features of the IHT exemption for charities is that its territorial limits remain uncertain. My firm has been involved in what now has to be called the saga of Routier and another v Revenue and Customs Commissioners. There have been two Court of Appeal hearings and two judgments ([2016] EWCA Civ 938 and [2017] EWCA Civ 1584). At the time of writing we are waiting to hear if the Supreme Court will give us leave to appeal against both.

HMRC hold to the view, laid down in a House of Lords income tax case in 1956, that only British charities should get IHT relief. We have argued that this is not what IHTA s23 says and that, certainly in 2007 (the relevant date for IHT in Routier) this was not in line with the European law principle that there must be no restrictions on the free movement of capital. At the prompting of Europe, the charity tax rules were updated in 2010 to extend relief to other EU countries. It is still not clear if this is really enough, because the EU outlaws restrictions on movement of capital to all other countries as well.

IHT 36% rate: Kind Hearts and Coronets

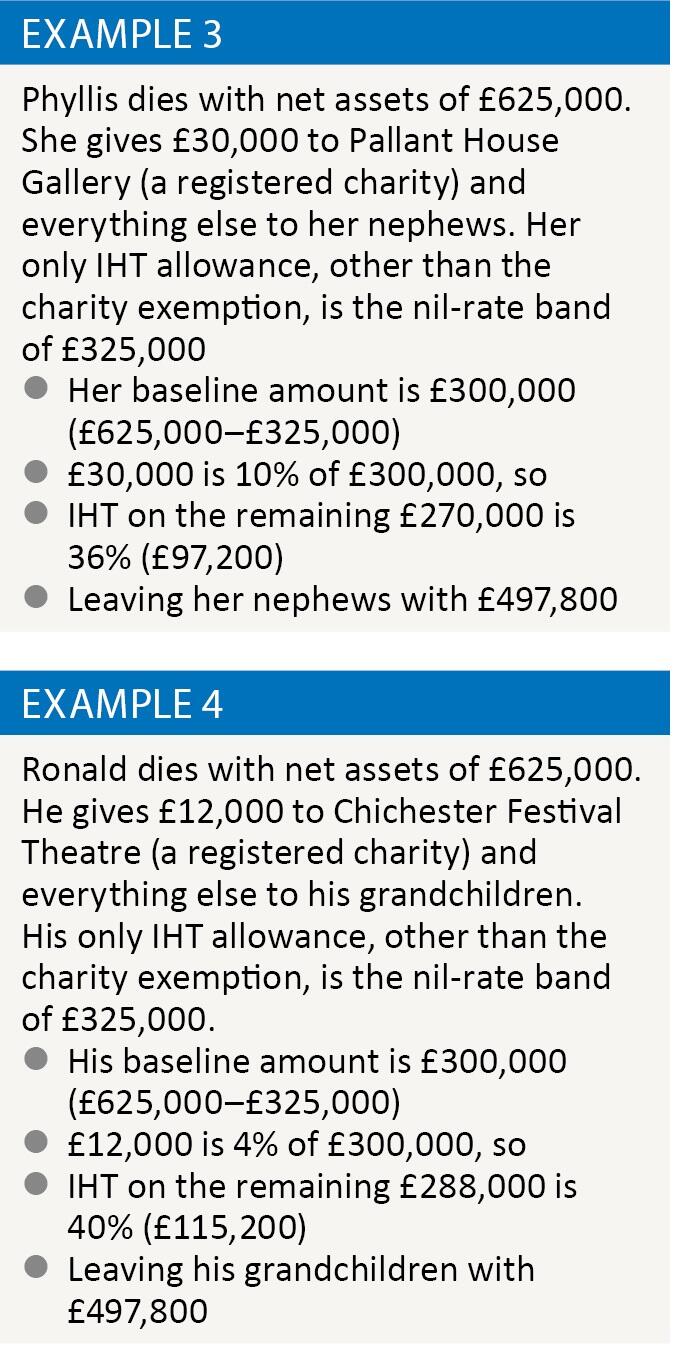

I have the impression that the relief, which reduces IHT on death from 40% to 36%, when a minimum amount is given to charity, is underused. Perhaps this is due to the complexity of the rules, which can be found in IHTA 1984 Sch 1A.

It is often thought that an estate gets this relief only if at least 10% of the whole of it goes to charity. But, in most cases, the ‘donated amount’ does not need to be nearly as much as this.

The threshold is a charitable gift of 10% is of what is called the ‘baseline amount.’ This is the value of the net estate, after all reliefs and exemptions, other than charity relief. (Or it should be; for some reason no account is taken of the new residence nil-rate band.) See example 3.

The apparently complex rules for this relief become more straightforward when this principle is grasped. The complexities actually make the relief more useful, if IHT is payable on assets not passing by will (for example on a qualifying interest in possession). The rules give the flexibility to make claims in the most beneficial way.

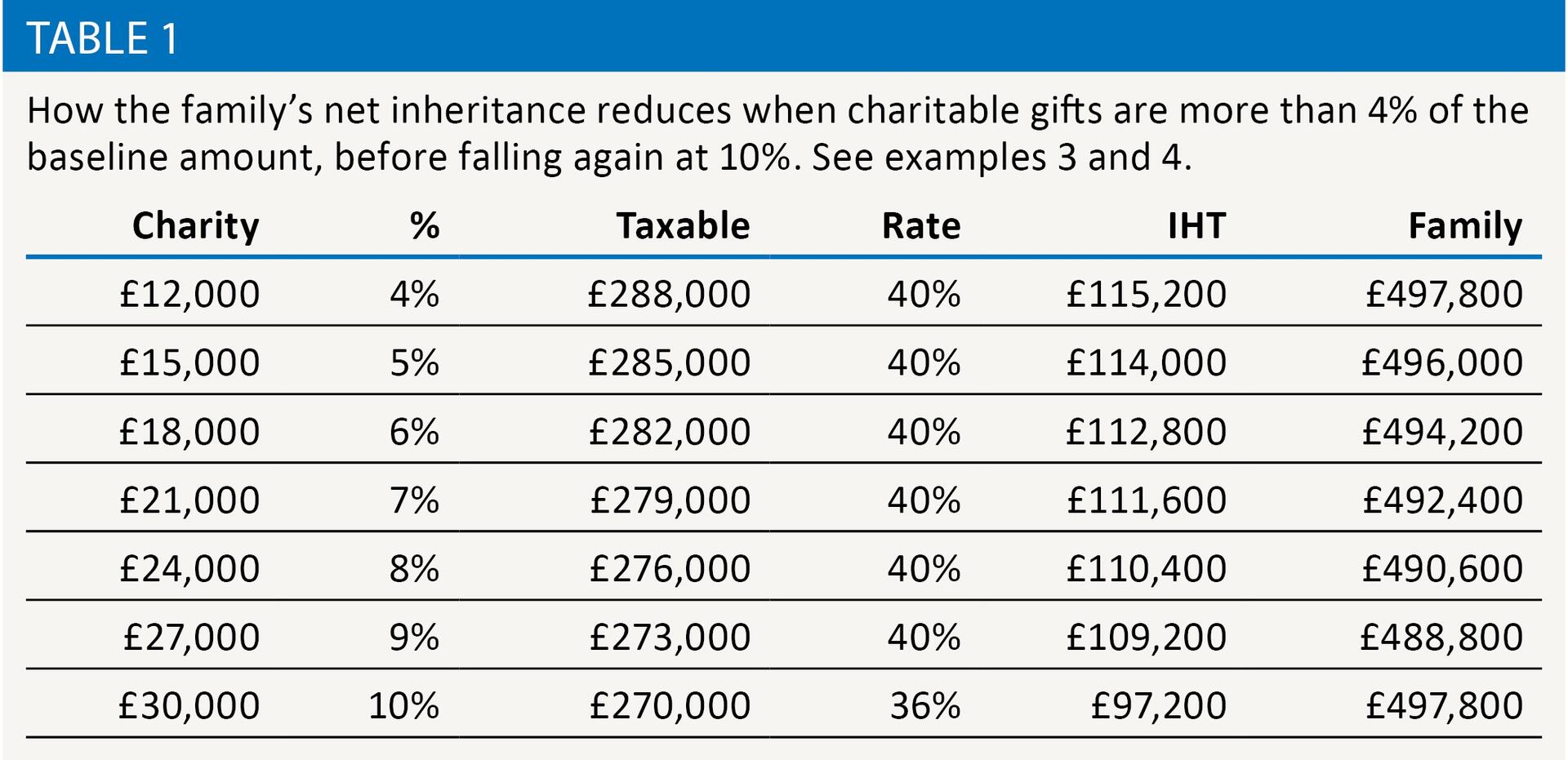

Reducing IHT from 40% to 36% at the 10% threshold results in what I call a cliff – a sudden drop. Example 4, compared with example 3, shows how family beneficiaries receive the same, after IHT, if charitable gifts are only 4% of the baseline amount. If the gift to charity is between 4% and 10%, the family actually get more by increasing the gift to 10% – see table 1.

Variations and trust appointments, within two years of death, give many opportunities to take advantage of this relief. Under IHTA s 142 or s 144 the IHT effect is backdated to death. If there is no gift to charity in a will, when IHT is payable, the cost to the family of inserting a 10% gift to charity is £2,400 for every £10,000 given to charity.

IHT grossing up: The Love Lottery

Suppose Florence has assets worth £2.4 million and wants to leave a quarter to her nephew Jim and the other three-quarters between three charities. There is no easy balance between minimising IHT and fairness.

If Florence’s will divides everything into these quarters then, if she makes no special provision, Jim pays all the IHT. Suppose Florence’s only IHT allowance is the £325,000 nil rate band. His £600,000 has to meet 36% IHT (clearly the charity gifts are much more than 10% of the baseline amount) on the £275,000 over the nil rate band, which is £99,000. Jim gets £501,000 while the charities get £600,000 each.

On the other hand, if Florence gives £600,000 to Jim, and the rest of her estate equally to the charities, that £600,000 will be treated as free of IHT. This means that the gift has to be grossed up to the amount which, after deduction of 36% IHT on the amount over £325,000, would leave £600,000. This is £754,687.50 on which IHT would be £154,687.50. This time the charities have to pay all of the (much bigger) IHT bill. Jim gets his £600,000, but the charities only some £548,000 each.

If Florence wants the division to be fairer, so that each of Jim and the charities end up with the same amount, her will has to say that specifically. Roughly, each of Jim and the charities would end up with about £566,000 and the IHT would be some £136,000.

It really is a lottery. Because charities can’t usually agree to give up anything bequeathed to them, the will has to get this right.

Finally: A Run for Your Money

Altogether these tax allowances for charities have the potential to spread lots of human happiness. Which is what the Ealing comedies do, for both the viewer and most of the characters (the crooks are the exception). Best of all, the long-suffering policeman (Jack Warner, most famous as Dixon of Dock Green) told the original Mrs Wilberforce to keep the loot.