The complexity of capital allowances

Share this article

Alun Oliver reviews the capital allowances case of Glais House Care Limited v HMRC

Key Points

What is the issue?

Capital allowances has seen a flurry of recent legal decisions issued in the last few months.

What does it mean to me?

The decision in Glais House Care Limited v Commissioners for HMRC [2019] UKFFT 0059 (TC) published at the end of January 2019. The case highlights the complexity of capital allowances on second hand property purchases and specifically the approach and restrictions on valuation of capital allowances on the purchase of an existing care home.

What can I take away?

Owners of care homes, pubs, restaurants or hotels (properties frequently subject to contract allocations) not caught by the New Fixtures Rules and that had previously limited their capital allowances claims to relatively modest contract allocations may wish to revisit their claims with an independent capital allowances valuation to overwrite the contract allocations in light of this decision.

Capital allowances has seen a flurry of recent legal decisions issued in the last few months. The decision in Glais House Care Limited v Commissioners for HMRC [2019] UKFFT 0059 (TC) highlights the complexity of capital allowances on second hand property purchases and specifically the approach and restrictions on valuation of capital allowances on the purchase of an existing care home, Glais House in Swansea. HMRC challenged the purchase claim made by Glais House Care Limited (Glais House) following their claim for plant & machinery allowances (PMAs) and integral features allowances (IFAs).

Background

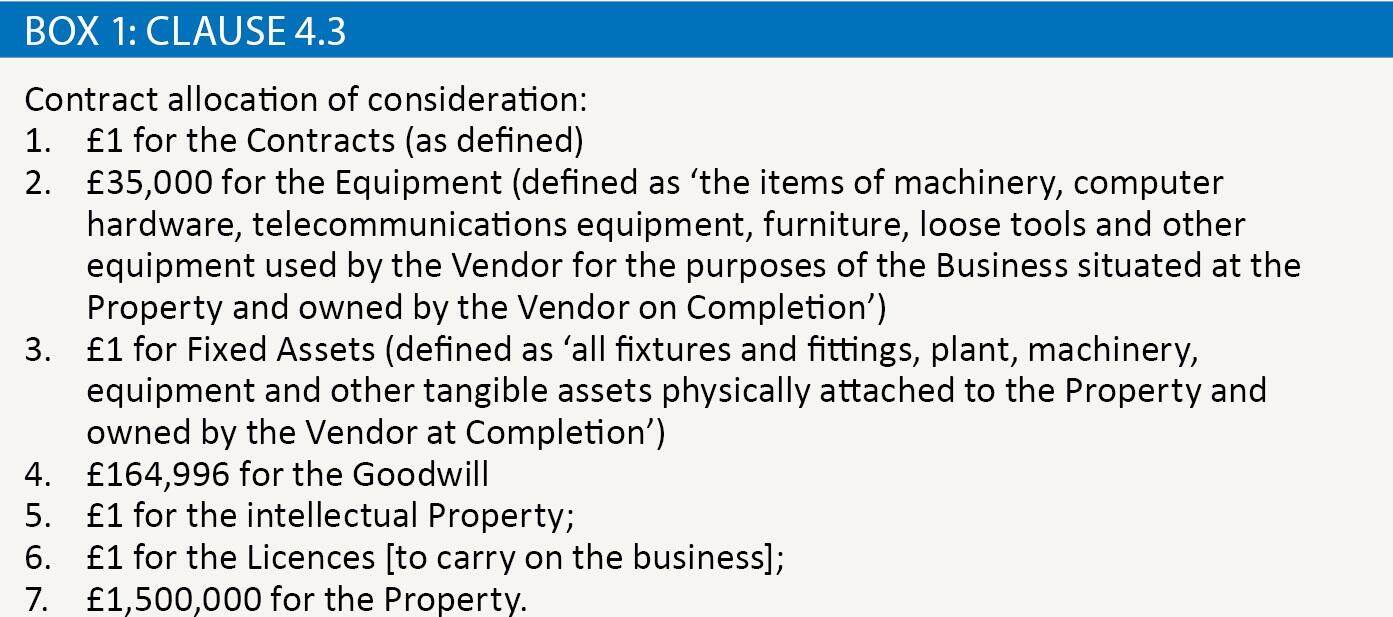

Glais House acquired the care home in May 2011 for a total consideration of £1.7m from the administrators of Kappians Care Homes (KCH) that had owned the property since March 2005. The property was operated throughout as a residential care home. The purchase price was broken down into various elements under clause 4.3 of the contract. See box 1.

Despite these agreed contract values, Glais House subsequently commissioned a capital allowances valuation from a firm of accountants, Lane & Lane (albeit the case transcript is not clear if this valuation was prepared in house by Lane & Lane or by a third party consultant). This was noted in their 2014 accounts as a reclassification of £318,792 from ‘Freehold Property’ to ‘Plant & Machinery’ and the capital allowances claim submitted to HMRC on 26 March 2014.

Although it is not clear why, HMRC seemingly disclosed the private tax details of KCH to another tax payer. They showed that

KCH had a residue of allowances in their main pool as at 2010 of £85,504.

When KCH was subsequently wound up, after the disposal of the care home, they claimed a balancing allowance of £50,803 – agreed by the parties to be a transposition error and correctly reinterpreted as £50,503 residue after the £35,001 that had been included in the prior sale of the care home in points 2 and 3 above.

The valuation for Glais House had been carried out under CAA 2001 s 562 as a ‘just and reasonable apportionment’ of the purchase price. This required the tax payer to assess the value of the constituent parts of the property purchased under a single bargain.

However, HMRC seeks parity between vendor and purchaser so that the tax position is consistent, but also reasonable. Specifically, s 562(3)(a) and (b) look to align the net proceeds of the sale and the proportion of the consideration attributable to an item as both determined by this ‘just and reasonable apportionment’. This is further set out in HMRC’s Capital Allowances Manual at CA12100 which states ‘If you find out that an apportionment has been made you should check with the buyer/seller’s district to make sure that the buyer/seller has used the same apportionment in their capital allowance computations as your taxpayer. You should not accept your taxpayer’s computations if different figures have been used’.

Key issue

Although the parties agreed the issue to be resolved was the application of the elements of the CAA2001 that potentially restricted the capital allowances claim possible; namely:

- CAA 2001 s 185 – limited to that ‘which has been or is required to bring into account’ by the past owner upon disposal; and

- CAA 2001 s 62(1) – ‘any disposal value required to be brought into account…is limited to the qualifying expenditure incurred by the person on its provision’

HMRC took the line that the contract allocation was applicable, with the disposal value set at £35,001. HMRC said that, because KCH had reported only £35,001 in the agreement, this sum should be treated as the amount KCH ‘has been or is required’ under CAA 2001 s 185 to bring into account. Thus the capital allowances Glais House could claim should be restricted to £35,001.

Glais House, however felt that their valuation at £318,792 was the correct figure. Although, there did not appear to be any reference at this stage to any prior claims by KCH – which should have been part of the due diligence in preparing a valuation claim.

Judge Philip Gillett, hearing the case at the First Tier Tax Tribunal, determined that whilst the just and reasonable apportionment was the correct valuation approach, this was still subject to a restriction under s 62(1). This capped the disposal value brought into account by KCH at their original cost and so restricted the subsequent claim.

Decision

It was common ground between the parties that that the original qualifying PMA expenditure by KCH was £220,912 but Judge Gillett felt it was appropriate to exclude the £15,000 incorrectly claimed by KCH for cold water and thus the total was reduced to £205,912. This was accepted as the base figure to which KCH’s disposal value was set.

Having acquired the care home in May 2011, Glais House were now additionally entitled to claim cold water installations and all of the electrical installations (claims prior to the April 2008 introduction of IFAs were limited to partial claims of only certain electrical works as PMAs). Accordingly the findings of the Tribunal were that Glais House could claim £13,226 in respect to the ‘cold water’ and £17,006 in respect of the ‘Mains electrical system’ – both at their 2014 valuation amounts. Chattels (or loose equipment) are normally excluded from the calculations of just and reasonable apportionment under s 562 however Judge Gillett sought to be consistent and therefore also ruled that whilst the 2014 claim valuation had not calculated a just and reasonable figure for the equipment, it would be inappropriate to rely upon the £35,000 contract figure. The case testimony disclosed that these assets only cost KCH £18,458 and thus this amount was deemed to be the maximum possible claim but Gillett J instructed the parties to calculate the relevant figure in a consistent manner with his decision to settle the matter, as they see fit.

Implications

As was acknowledged during the case, that the New Fixtures Rules under ss 187A and 187B have remedied some aspects of this potential imbalance between a vendor’s disposal value and a subsequent claim by the purchaser. Since April 2014, failure by the purchaser to address the capital allowances requirements within their Sale & Purchase Agreement typically result in nil capital allowances under s 187A(3). However owners of care homes, pubs, restaurants or hotels (properties frequently subject to contract allocations) not caught by the New Fixtures Rules and that had previously limited their capital allowances claims to relatively modest contract allocations may wish to revisit their claims with an independent capital allowances valuation to overwrite the contract allocations in light of this decision.

I was rather surprised by the apparent breach of taxpayer confidentiality. Previously tax officers had been instructed within manuals at CA26400 to reject any claim where the tax payer cannot provide the relevant tax history and disposal value from the vendor. This ‘burden of proof’ on the claimant to demonstrate they have a valid claim was reinforced in both West Somerset Railway Plc v Chivers (HMIT) [1995] SpC 1 and more recently in the case of Mr & Mrs Tapsell & Mr Lester ‘The Granleys’ [2011] UKFTT 376 (TC). It will be interesting to see if this case sets a precedent requiring HMRC to release certain tax details of prior owners to help facilitate subsequent tax payers to make their case?

Historically, ‘loose equipment’ or chattels have been regularly accepted at the contract allocation and excluded from any just & reasonable apportionment – typically only applied to land & buildings. However in light of this case, tax payers can clearly potentially challenge any unreasonable figures. No doubt those solicitors acting for vendors will seek to gain a contractual restriction that the parties agree to any contract allocations as having been made in accordance with s 562 and thus are ‘just and reasonable’; and that neither party will seek to challenge, amend or replace the contract figures with any subsequent values, without liability for recompensing any resulting tax consequences upon the other party.

HMRC will no doubt still be seeking to mirror the disposal and purchase position – wherever possible, if claims not denied by the requirements of the New Fixtures Rules.