The concluding chapter?

Share this article

Matt Stringer considers the most recent developments to the diverted profits tax

Key Points

What is the issue?

From April 2019, the UK applies an income tax charge to intangible property receipts of certain non-resident companies. The new rules are a furtherance of the UK’s response to BEPS via intra-group licensing arrangements and IP locations.

What does it mean to me?

Multinational groups with IP in a low-tax and low-substance location must carefully consider the impact of the new rules. Even groups without a taxable presence in the UK may be subject to a charge.

What can I take away?

An overview of the new law, the story of its development and a renewed desire to watch Return of the Jedi.

Avid Tax Adviser readers (with excellent memories) may recall my article The Sequel! from the May 2017 issue, which considered the changes to Diverted Profits Tax (‘DPT’) from Finance Bill 2016. In that article I considered the rationale for a sequel to DPT, originally introduced in Finance Act 2015, and how DPT II went further than the original DPT measures in its goal of tackling the perceived tax avoidance of a multinational group with a low-tax IP owner.

My final remark back then in 2017 was that sequels are often not the end of the story: for particularly thrilling tales, the concluding chapter of a trilogy is where the real heart of the story lies. I hate to say ‘I told you so’ but…

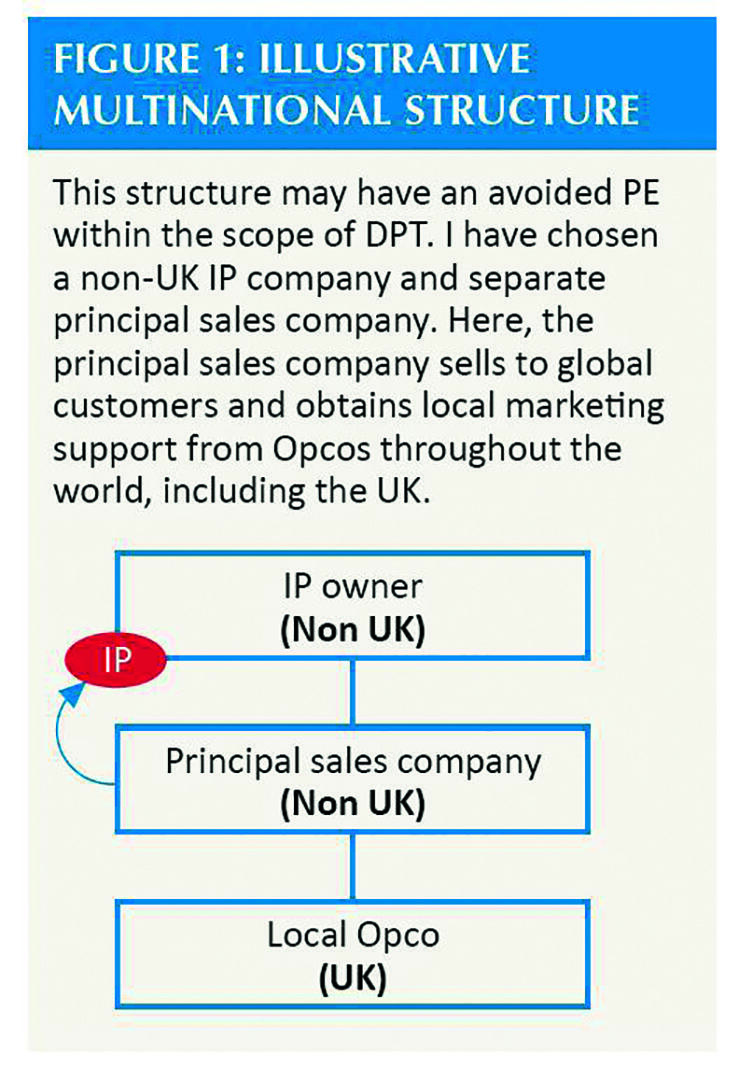

Let us use figure 1 to remind ourselves of the DPT provisions, both the original, and the sequel.

DPT: The original

DPT I was unilaterally introduced in the UK in order to further the stated aims of the Base Erosion and Profit Shifting (‘BEPS’) project, and in response to the calls for increased taxation of large multinational corporations. DPT I applied in two scenarios: where there was a transaction lacking economic substance or where there was an avoidance of a UK permanent establishment (‘PE’). For either scenario to apply there must be an arrangement or series of arrangements where income is ultimately taxed at a low (or nil) rate, or have a main purpose of avoiding a UK corporation tax charge.

The avoidance of a PE is particularly relevant to multinationals with a UK local support function (i.e. marketing, sales support) but with a low-tax offshore IP owner and an overseas sales principal company which conducts sales with customers (including UK customers). Subject to meeting some conditions, this model (as shown in Figure 1) may be within the scope of DPT I by avoiding a UK PE.

In accordance with DPT I, the foreign sales principal that may have an avoided PE must then consider whether it has a liability to DPT. In doing so it must consider the alternative provision that it would have made, had any taxes on income not been a consideration. Where this results in the same type and amount of expenses (i.e. still paying the same royalty, but to a different IP owner in a higher taxed jurisdiction), and the UK company is already fully rewarded for its activities under traditional transfer pricing principles, the DPT liability may well then have been zero.

Said another way, DPT I enabled the UK’s taxing arm to extend only one level: where the UK company and the sales principal of the group were paying their ‘fair share’, DPT I could do no more. DPT II went further to tackle this challenge.

DPT II: The sequel

DPT II changed the way that DPT may be calculated by using a withholding tax mechanism on the royalty payment from the sales principal to the IP owner. Where a foreign company has an avoided PE and pays a royalty which is connected with that trade, the royalty could be deemed to have a UK source. The foreign company must calculate the ‘just and reasonable’ portion of that royalty that should be sourced to the UK vs sourced to the foreign HQ. The portion which has a UK source is then included as diverted profits and subject to a DPT charge.

DPT II was introduced alongside wider changes to the UK’s rules regarding withholding tax on royalty payments. A foreign company with an actual UK PE would be required to undergo the same task, with the UK sourced portion of any royalty payment being subject to UK income tax in that circumstance.

Usual treaty principles may apply in both cases (where the treaty between the UK and the recipient of the royalty may act to reduce or eliminate the royalty withholding tax due/reduce the DPT charge on a proportionate basis). This is of course only of benefit where the UK has a treaty with the jurisdiction of the royalty recipient providing for a reduced rate. Where the IP owner is located in a low or no tax jurisdiction (i.e. tax haven), the treaty network is unlikely to provide relief.

DPT II therefore went further than DPT I was able to. DPT II enables UK taxation to be collected on a royalty payment to a low-tax IP owner, even where the UK group company is adequately rewarded for the UK based activities.

The impact of a sequel

DPT II (rightfully) drew plenty of attention in the international tax world.

One of the fundamental principles of international taxation is that corporate taxes are based on profits which are attributed to the jurisdiction. That attribution has then primarily been based on transfer pricing methodology: considering functions, assets and risks undertaken in the jurisdiction.

This broad principle however leaves many unsatisfied that BEPS has been adequately tackled. Once each jurisdiction has taken their share, many large multinationals continue to leave a ‘residual’ (that last piece of the cake once everyone at the party has taken their slice), with that residual arising in a jurisdiction with nil or very low tax.

DPT II enabled the UK to go further than that traditional collection of arm’s length profit and come back for a second slice of cake after everyone else has left the party. It was a trailblazing change.

The DPT trilogy

For some however, DPT II did not go far enough. If your sights are set on penal taxation of any multinational using a low-tax or nil-tax IP owner to reduce a group tax bill, then more is needed.

The main drawback of DPT II in tackling BEPS via intra-group licensing arrangement is that it requires the group to be within the scope of DPT to begin with. This requires, for example, a group to meet the conditions required to have an ‘avoided PE’, which includes a motive test. HMRC will have certainly been involved in many a debate regarding this motive condition since the introduction of DPT: with multinationals sure to take the position that the taxation of their IP owner is not a matter that had a main purpose of avoiding UK corporation tax.

DPT III goes one step further in the taxation of the low-tax IP owner. It does so in removing all gating conditions to be within the scope of DPT. So much so, that it is not actually DPT at all!

DPT III: Taxing offshore receipts in respect of IP

Section 15 of Finance Act 2019 introduces Schedule 3 – ‘Offshore receipts in respect of intangible property’. The new legislation is a product of a consultation process which began in December 2017 titled ‘Royalties Withholding Tax’. The stated policy aim of the new legislation is to tackle erosion of the UK tax base via intra-group licensing arrangements that achieve an artificially low effective tax rate.

A key point to note is that the measure introduced in Schedule 3 FA19 is not DPT, nor is it a withholding tax, but a direct UK income tax charge on a non-UK resident company. The journey of DPT becomes clear: DPT I was a UK tax on the royalty payor; DPT II was a withholding tax on the royalty payment to a low tax IP owner; DPT III now directly taxes the IP owner.

The new rules state that ‘UK derived amounts’ will be taxable for persons who are (at any time during the tax year), resident in a jurisdiction that is not a ‘full treaty territory’. The person receiving such amounts will then be liable to UK income tax on those amounts.

A ‘full treaty territory’ is any jurisdiction with which the UK has a double tax treaty that contains the non-discrimination clause. This of course means that only a minority of jurisdictions across the globe are within the scope of the measures. The UK has the largest treaty network in the world and looks to include a non-discrimination clause in the majority of those treaties. Jurisdictions that fall within the scope of the measures are therefore, in the main, those that could be considered a ‘tax haven’. There are some notable exceptions though: to take an example, the UK does not have a tax treaty with Brazil. Other jurisdictions without a full treaty with the UK are likely to be mainly developing countries.

UK derived amounts

In my opinion, the most interesting part of the legislation (and the discussion that will surely follow) is how to define and quantify a ‘UK derived amount’. The law defines these amounts in a broad sense – capturing any intangible property receipts that somehow link to revenues derived from UK persons, or based on UK activities. Intangible property is again defined broadly, to encompass all property except those items that have been listed as excluded. The law provides that amounts should be attributed to UK sales based on a just and reasonable apportionment, with the default position being an apportionment based on overall sales.

There are several important points to note here. Firstly, the definition of intangible property is broader than the definition contained in s712 CTA 2009 which UK tax practitioners will be familiar with. Therefore, there may be types of property which are within the scope of the measures that would not be intangible assets for UK corporation tax purposes. The amounts which are within scope in relation to such intangibles is also defined broadly – it is not only royalty payments in respect of IP that are within the scope of the measures, but also IP disposal gains and other payments in relation to IP transfers.

The reference to a just and reasonable apportionment, and a sales fraction being the default position in defining such an apportionment, mirrors that of DPT II. Further, sales as a driving force for the tax charge appears again in the definition of a UK derived amount. Taxpayers and HMRC will need to give due thought to appropriate mechanisms to apportioning their intangible property receipts between UK derived amounts and other amounts, considering the weight that the legislation places on sales.

In general, IP rights provide protection against infringement by other parties. Payments in respect of IP are then made in respect of activities which would otherwise infringe upon those rights, if not for a license or other arrangement in respect of the rights. Sales figures may therefore not always be an appropriate reasonable measure to understand why payments in respect of IP exploitation are made. Payments in respect of customer distribution rights over IP may easily be traced to sales figures. Payments in respect of manufacturing know-how, for example, may be more reasonably placed to the location of the manufacturing site (and not to the location of sales activities). However, given the reference in the new law to direct or indirect enablement, facilitation or promotion of UK sales, and the default position to be an apportionment of sales figures, we can expect HMRC to resist any other basis even where some of those activities occur in different accounting periods to the recognition of the sales.

Exemptions

Certain exemptions are included which would render a foreign company fully outside the scope of the charge.

The first is an exemption based on quantum of UK sales – which is set at £10m. Sales of all connected persons must be aggregated, hence there is no need for the IP owner to also be a customer facing entity in respect of all sales. This exemption is included such that only large groups are within the scope of the measure. It should be noted that the £10m threshold is not a requirement for turnover in a UK resident company, but in relation to any UK sales. The legislation contains no requirement for a group to have any corporate tax presence in the UK – merely that sales are made to UK persons or provided in the UK. It is of course feasible that groups without a UK tax presence could fall within the scope of the measures.

The second is an exemption based on genuine business activity. A company is exempt from the charge where development, enhancement, maintenance and exploitation occurs, in the main, in the country of residence (and always has done). The section is drafted narrowly such that only those groups with genuine IP related activities offshore may meet the exemption. We can expect HMRC to carefully consider the facts of any claim submitted given the narrow drafting.

The third is an exemption based on a comparison of the actual tax suffered on UK derived amounts, and the UK income tax that would have been suffered on the same amounts under these provisions. Where the actual tax suffered is at least 50% of the comparable UK tax charge, the exemption may apply. No theoretical exemption or allowance is given to the UK comparable, hence a straight 20% calculation is deemed (based on the current basic rate of income tax). Subject to specific adjustments to the tax base in the overseas jurisdiction, this broadly provides a 10% tax rate benchmark for the exemption.