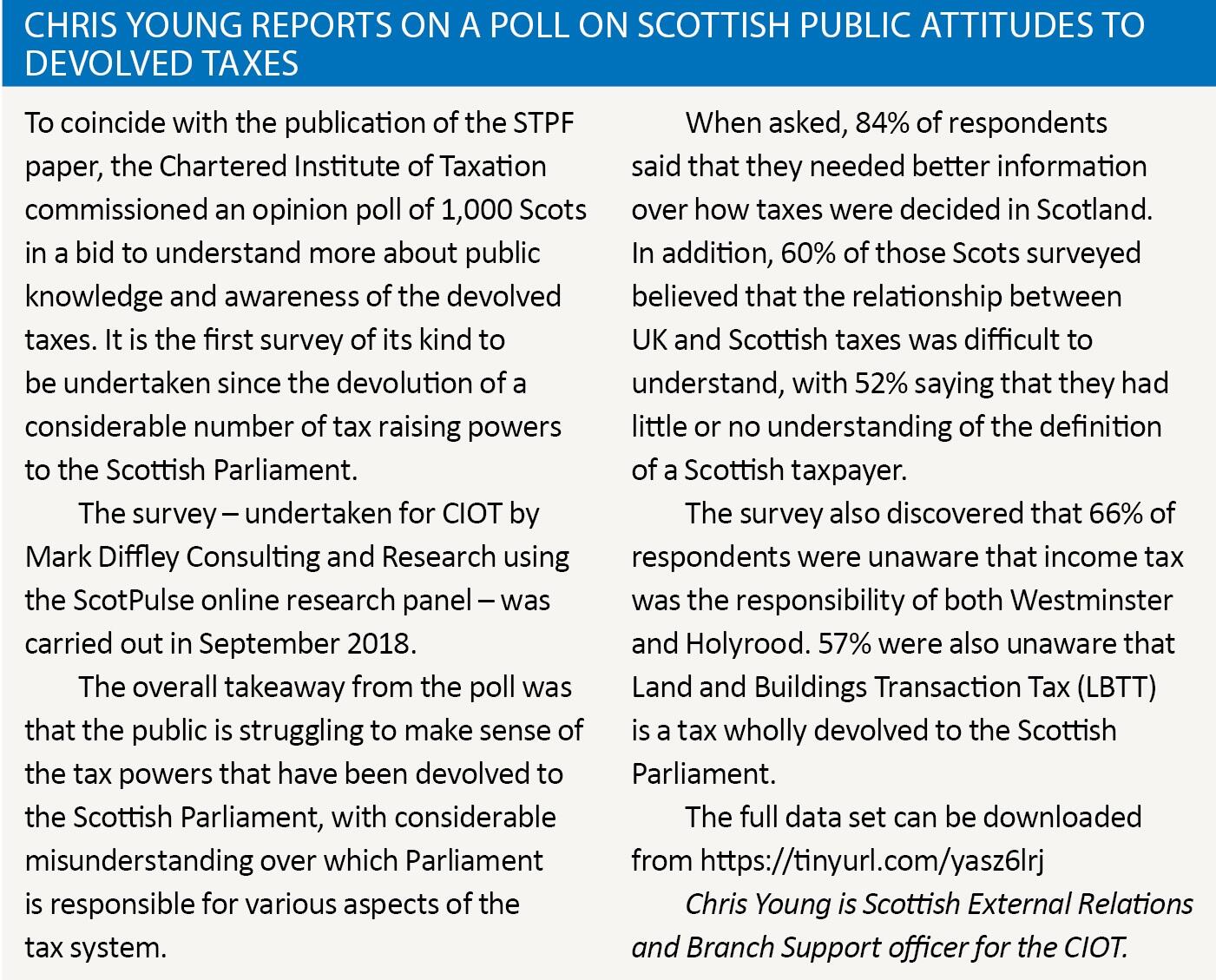

Devolving taxes: learning from the Scottish experience

Share this article

Joanne Walker and Charlotte Barbour report on a new initiative by the CIOT and ICAS

Key Points

What is the issue?

There has been significant devolution of tax powers in the last two Scotland Acts of 2012 and 2016 but their overall impact needs to be analysed – in relation to Scottish taxes and in relation to the rest of the UK tax system.

What does it mean for me?

With devolution introducing new powers and responsibilities around tax, this brings its own complications. Practitioners need to be aware of tax in the different parts of the UK and the spill over this may have into UK tax practice.

What can I take away?

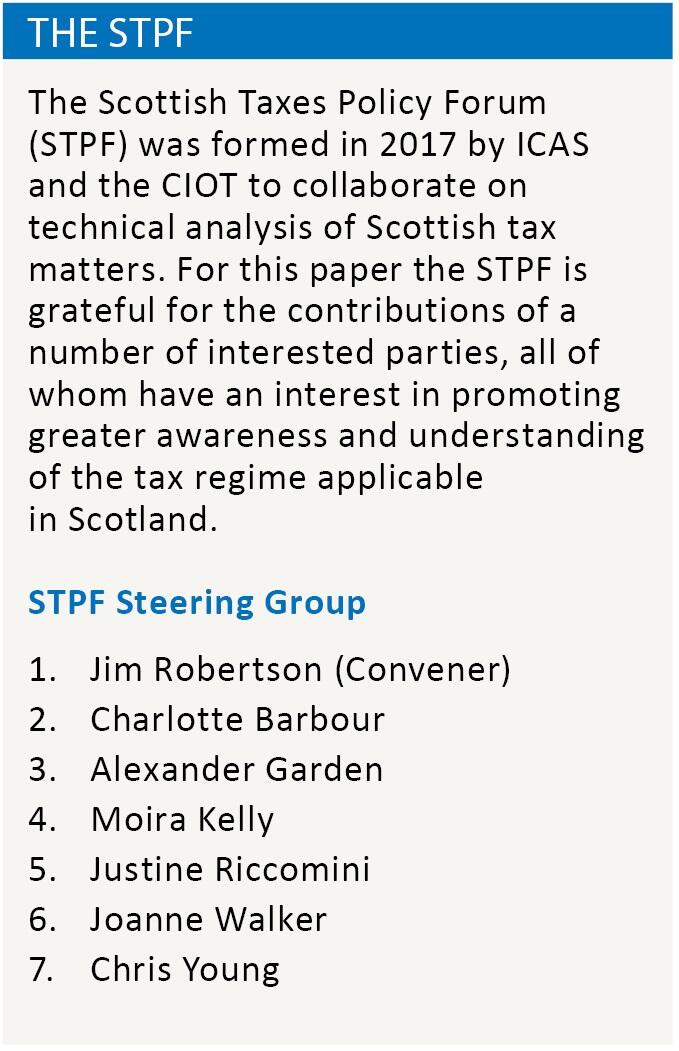

The CIOT and ICAS have formed the Scottish Taxes Policy Forum to collaborate on technical analysis of Scottish tax matters to inform the debate around the devolution of taxes – and there is much that can be learnt from the experience in Scotland to date. The professional bodies continue to call for the Scottish Government to work closely with the UK authorities to ensure that tax administration is kept as streamlined as possible.

Introduction

The Scottish Taxes Policy Forum (STPF) has been formed in order to collaborate on technical analysis of Scottish tax matters, and with a view to produce and build alignment around expert opinions that are clear, realistic, accurate and politically neutral. We want to inform the debate around the devolution of taxes – and there is much that can be learnt from the experience in Scotland to date.

In October 2018 the STPF produced its first paper ‘Devolving Taxes across the UK: Learning from the Scottish Experience’, which is a critique of the current tax powers that have been devolved to the Scottish Parliament – their challenges, risks and opportunities – and it discusses the progress of devolution of taxes to Scotland since the Scotland Act 1998. The main focus is on the taxes devolved in the Scotland Acts of 2012 and 2016 with a special emphasis on Scottish Income Tax, given its importance in terms of numbers of taxpayers affected and revenues raised.

The paper focuses on the operational aspects of Scottish taxes with the questions of principle that such matters flush out, such as:

- The interaction of Scottish rates with UK mechanisms for giving tax relief at source (e.g. relief at source on pension contributions, or Gift Aid) – which leads to the question of whether Income Tax reliefs should be delivered in a different way, devolved, or abolished altogether.

- The need for both Scottish tax calculations for non-savings, non-dividend (NSND) income and UK based calculations if a Scottish taxpayer also has savings income and dividends introduces added complexity for taxpayers, agents and HMRC – which leads to the question of whether Income Tax rates and bands applicable to all sources of income should be devolved.

- The possibility of tax planning and behavioural responses where there are differentials in rates and bands between jurisdictions, or between taxes some of which are devolved and others of which are reserved – which raises the question of whether tax competition is a positive economic tool or encourages unintended tax avoidance.

- The administrative issues and costs that can arise in identifying Scottish taxpayers and building new software to collect Income Tax from them – which leads to the question of whether there are more efficient ways to administer and collect Scottish income tax.

- The tailoring of devolved taxes, which have been ‘cut and pasted’ from the UK legislation to some extent, but with differences to interact with Scots law and to deliver distinct policy aims means that there may be conflicts with the business desire for consistency. Land and Buildings Transaction Tax (LBTT) has elements that are unique to align it with Scots property law (such as with leases), but nevertheless in the three years since its introduction it has become more closely aligned with Stamp Duty Land Tax (SDLT) – which raises questions about the purpose and strategic thinking around devolution or whether there should be greater use of partial devolution.

The questions we raise are meant to provoke discussion with a view to reaching a consensus on what needs to be achieved to optimise the efficiency, practicality, simplicity and transparency of the devolved tax system in Scotland, in line with Adam Smith’s four canons of taxation. Overall, the big question is: is the current devolution model delivering on its potential?

There are also a number of recommended priorities:

Across the UK tax system

- We would welcome a more logical and consistent strategic framework for the devolution of tax powers across the UK, as it would lend itself to generating a greater understanding and preparedness by taxpayers, businesses and advisers.

- We think further consideration of the UK Income Tax framework and how the process of devolution of the rates and bands dovetails into it would enable the UK and Scottish Governments to eliminate unwanted consequences from their chosen plans and actions.

- More effective and transparent collaboration between each of the devolved Governments and the UK Government around negotiations on taxation policy should lead to increased public awareness of devolved taxes. We believe that it is important that the public and industry are aware of the devolved taxes space as this leads to increased cooperation and compliance.

- Better data than is currently available on Scottish taxpayers and the movements between jurisdictions should be developed. At present, for example, Scottish taxpayers are still being discovered by HMRC and there is still an estimation of a gap between who falls into the Scottish taxpayer category and who HMRC have categorised as such, which is potentially detrimental to the Scottish purse.

- There should be a more realistic time frame between the UK and Scottish Budgets to allow more time for the Scottish Government to react. This issue was considered by the Budget Process Review Group reports, so our paper did not cover it in any further detail.

Across the Scottish tax system

- More openness around strategic thinking is needed – for example, setting out a five-year framework or process map for Scottish taxes, including clear aims and objectives of what the taxes are going to achieve, and to tie in with the Scottish Fiscal Commission’s five-year projections format.

- We would welcome the introduction of a Tax Committee in the Scottish Parliament, which could focus on taxation in Scotland and sit separately to the Finance and Constitution Committee. This Committee could, for example, comprise members with specialist taxation expertise which would be required to enhance and fortify the tax focus.

- We think an annual care and maintenance provision, such as a Finance Act, should be introduced into the Scottish legislative cycle. This would ensure that anomalies and unintended consequences of devolved legislation can be addressed in a regular process without the need for piecemeal amendments by way of either standalone acts or by secondary legislation, while continuing to ensure proper scrutiny.

- There should be more policy collaboration between Revenue Scotland and the Scottish Government. Greater liaison on policy would allow Revenue Scotland to actively input operational experience to policy making, and for policy making to gain from this.

The Scottish Taxes Policy Forum is undertaking strategic engagement with government, politicians and wider civic society, with the aim of promoting greater public awareness and understanding of Scotland’s changing tax landscape and its interaction with the wider UK tax regime. It would also welcome feedback and further insights from CIOT members.

The paper can be found on the CIOT website.