Doing the calculations

Share this article

Phil Gilbert provides guidance on how to ensure any of your clients who have been involved in disguised remuneration avoidance schemes are able to settle

Key Points

What is the issue?

With April 2019 just five months away, HMRC is busy working on settlement calculations and agreements for those who want to settle before the loan charge comes into effect.

What does it mean to me?

You can prepare full calculations for your client, then using settlement templates which HMRC can provide, send us a complete offer on behalf of your client. We will review this and, where accepted, confirm agreement. Alternatively, HMRC can calculate the potential settlement figures and generate the settlement paperwork.

What can I take away?

If your clients wish to settle but are concerned about paying then we will work with them to agree a payment plan that is manageable for them. We encourage you to explain to your clients the difference between settlement and paying the loan charge, and also to make clear HMRC’s view on arrangements claiming to avoid the loan charge.

With April 2019 just five months away, HMRC is busy working on settlement calculations and agreements for those who want to settle before the loan charge comes into effect.

This will affect those who have been involved in disguised remuneration avoidance schemes.

What should you or your clients expect settlement to look like?

There is detailed guidance on GOV.UK which covers the majority of what we expect to see in most settlements. However, every client’s circumstances will be different and some elements could prove more complex than others so we’ve created a case study using the settlement terms we published in November 2017 to demonstrate how it works. Although the case study looks at an Employee Benefit Trust (EBT) the loan charge will apply across a range of disguised remuneration (DR) schemes including contractor loans.

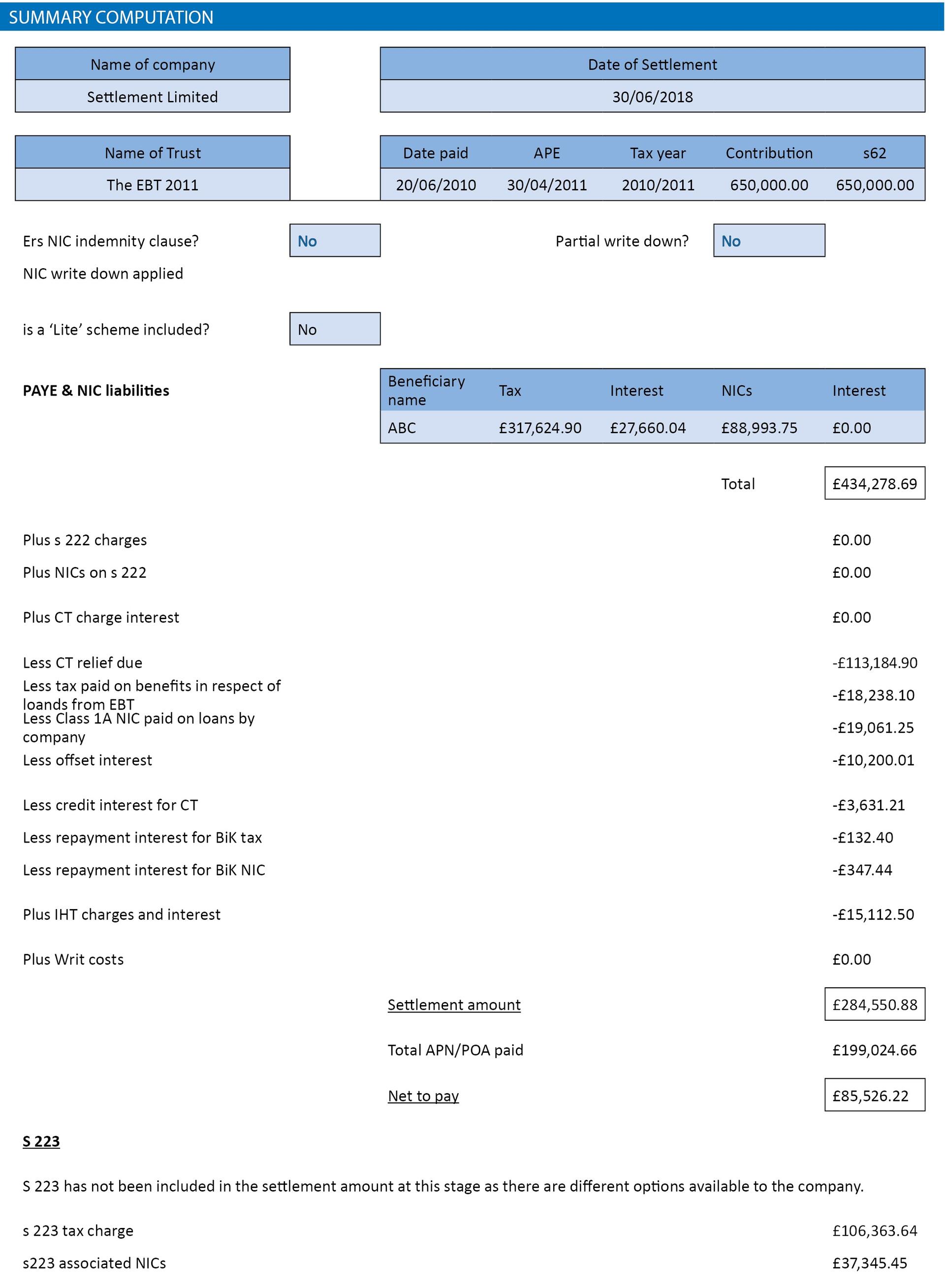

Case study: settlement of an employee benefit trust scheme

The company used an employee benefit trust in 2010/11 to remunerate a sole director. They made a contribution of £650,000 to the trust and it’s agreed that the contribution is earnings on entry to the trust in line with the Rangers decision.

The settlement summary is based on a settlement date of 30 June 2018.

Voluntary restitution

Voluntary restitution of National Insurance Contributions (NICs) and part of the income tax is included. Without voluntary restitution the company would have to pay the loan charge.

Based on information provided, HMRC raised a Regulation 80 determination in 2013. The determination was raised at basic rate. The PAYE tax due in settlement is £317,624, but interest is only charged on the £130,000 of tax determined. There is no interest charge on the further £187,624 of tax payable. This will generally be the position where HMRC have made insufficient determinations despite having the full facts available to them.

No decision under section 8 of the Social Security Contributions Act 1999 was issued in respect of the unpaid NICs so there is no interest charge on the NICs paid in settlement, nor any county court cost to be paid.

Corporation tax position

There was an open inquiry into the relevant company return. A deduction for the £650,000 contribution was included in their accounts, giving a profit of £1,678,504. Under BIM47090 the tax and NICs due in settlement (in connection with the £650,000 contribution) is allowed as a deduction for the same period. This means corporation tax (CT) was overpaid for that period and so the overpaid CT and repayment interest is offset in the settlement calculation.

In other cases relief may not be available in the year the scheme operated. Some options remain open until 5 April 2019:

- The PAYE and NICs paid in settlement can be offset in the earliest subsequent year where the CT position is open or where it remains possible to file an original or amended return.

- If there is an open enquiry but the returned profit is insufficient to relieve deductions flowing from the settlement this will create a loss in the enquiry year. The normal rules on loss relief will apply.

- Where a deduction wasn’t claimed for the contribution, no relief will be available under statute. By concession, under the settlement terms, HMRC will agree to current year relief where a relevant step is taken.

Any of these claims can be wrapped up in the settlement process to arrive at a net amount due.

Benefit in Kind of an interest-free loan

The employer reported loans from the EBT as a benefit in kind. The contribution is now agreed as earnings so the tax and NICs paid on the benefit so it can be relieved in the settlement. The director must make a claim to overpayment relief for the years where one can validly be made and sign a mandate to allow the repayment and interest to be set off in the settlement.

Inheritance tax

The EBT incorporated a wide beneficiary class which allowed all or most employees of the company to benefit, and in terms which satisfied the conditions of s 86 Inheritance Tax Act (IHTA 1984). However when the property was allocated onto the sub-trust for the director, the narrower beneficiary class failed the IHTA 1984 s 86 tests and consequently relevant property charges applied to the trust.

There are a number of possible points where an IHT charge could arise.

- Entry to the trust: potential charges arising under IHTA s 94 on participators by the transfer of value by a close company into the trust are relieved. This is because the full corporation tax deduction was allowed for the contribution, thereby giving relief under IHTA s 12. The company had also traded for at least two years, and none of the excepted assets conditions applied, so business property relief under IHTA s 103 also applied to relieve the s 94 charge.

- Transfer to sub-trust: the contribution into the offshore EBT was allocated to the director’s sub-trust within three months of the original contribution into the trust. As the funds moved to the sub-trust within three months, the charges on property leaving employee trusts under IHTA 1984 s 72(2)(a) did not apply.

- Exit from the trust: the trust was wound up and the loans made by the trust to the director were released following settlement of the income charges on 4 July. An exit, or proportionate, charge under IHTA 1984 s 65 became due on the loss of value to the trust of the loans it held.

The company, as settlor of the offshore trust, is liable for the trust charges incurred, and as part of the settlement terms, the trust charge of £15,112 is included in the overall settlement.

Accelerated Payment Notice (APN)

The company received an APN in 2016 and paid the full balance of £199,024 on 6 September 2016. The APN is offset against the settlement liability together with credit interest. If an APN is being paid in instalments then credit (and credit interest) would be given for each payment separately.

Any late payment penalties need to be paid and can be included in the settlement.

ITEPA 2003 section 223

The employer is paying tax that should have been deducted from the contribution in this settlement. The full £650,000 has been paid away so the company cannot make a deduction and there are a number of options available including:

- The director can make good the income tax paid by the company; there will be no charge under s 223.

- If the director doesn’t make good there will be a charge as earnings under s 223 on the tax paid by the company. This will be a personal liability of the director. There will also be a corresponding NICs charge for the employer to account for.

- The company can opt for settlement on a ‘grossed up’ basis. They will need to account for tax on an amount of gross earnings to leave the income tax paid figure of £317,624 as the net amount receivable.

When they return the settlement pack the company should tell HMRC which route they are taking as this will impact on the final settlement figure. There’s more guidance on s 223 in the Employment Income Manual at EIM21790.

Next steps

You can prepare full calculations for your client, then using settlement templates which HMRC can provide, send us a complete offer on behalf of your client. We will review this and, where accepted, confirm agreement. Alternatively, HMRC can calculate the potential settlement figures and generate the settlement paperwork. Whichever route is taken we need prompt return of the paperwork to finalise the case.

We realise the cost of settlement will be significant for some. If your clients wish to settle but are concerned about paying then we will work with them to agree a payment plan that is manageable for them.

HMRC is aware that some promoters are offering arrangements they claim avoid the loan charge. HMRC’s firm view of all the arrangements seen is that they do not work and those using them would still need to pay the loan charge. In many cases settlement is cheaper than waiting for the loan charge to arise. We encourage you to explain to your clients the difference between settlement and paying the loan charge, and also to make clear HMRC’s view on arrangements claiming to avoid the loan charge.

To discuss payment and settlement options with HMRC, please call 03000 534 226.