Hive downs

Share this article

James Tryfonos considers the reform of the intangibles regime in FA 2019 and provides a refresher on how it works in practice on a pre-sale hive down

Key Points

What is the issue?

One of the measures in Finance Act 2019 (FA 2019), with effect from 7 November 2018, reforms the intangibles regime. Its intention (so the Policy Paper says) is to ‘reduce frictions that inhibit commercial mergers and acquisitions’.

What does it mean to me?

This may be an issue where prior intra-group transfers have taken place, especially where there is a hive out scenario.

What can I take away?

Although Purchasers should still be wary if they intend to realise any IFAs post-acquisition and factor this into their deliberations (or price) the removal of the de-grouping charge will still be incredibly beneficial in not creating immediate tax charges. As such, the changes should remove one of the frictions in M&A transactions.

One of the measures in Finance Act 2019 (FA 2019), with effect from 7 November 2018, reforms the intangibles regime. Its intention (so the Policy Paper says) is to ‘reduce frictions that inhibit commercial mergers and acquisitions’. By taking a pre-sale hive down as an example, this article provides a refresher on how this should work in practice.

The intangible fixed asset regime

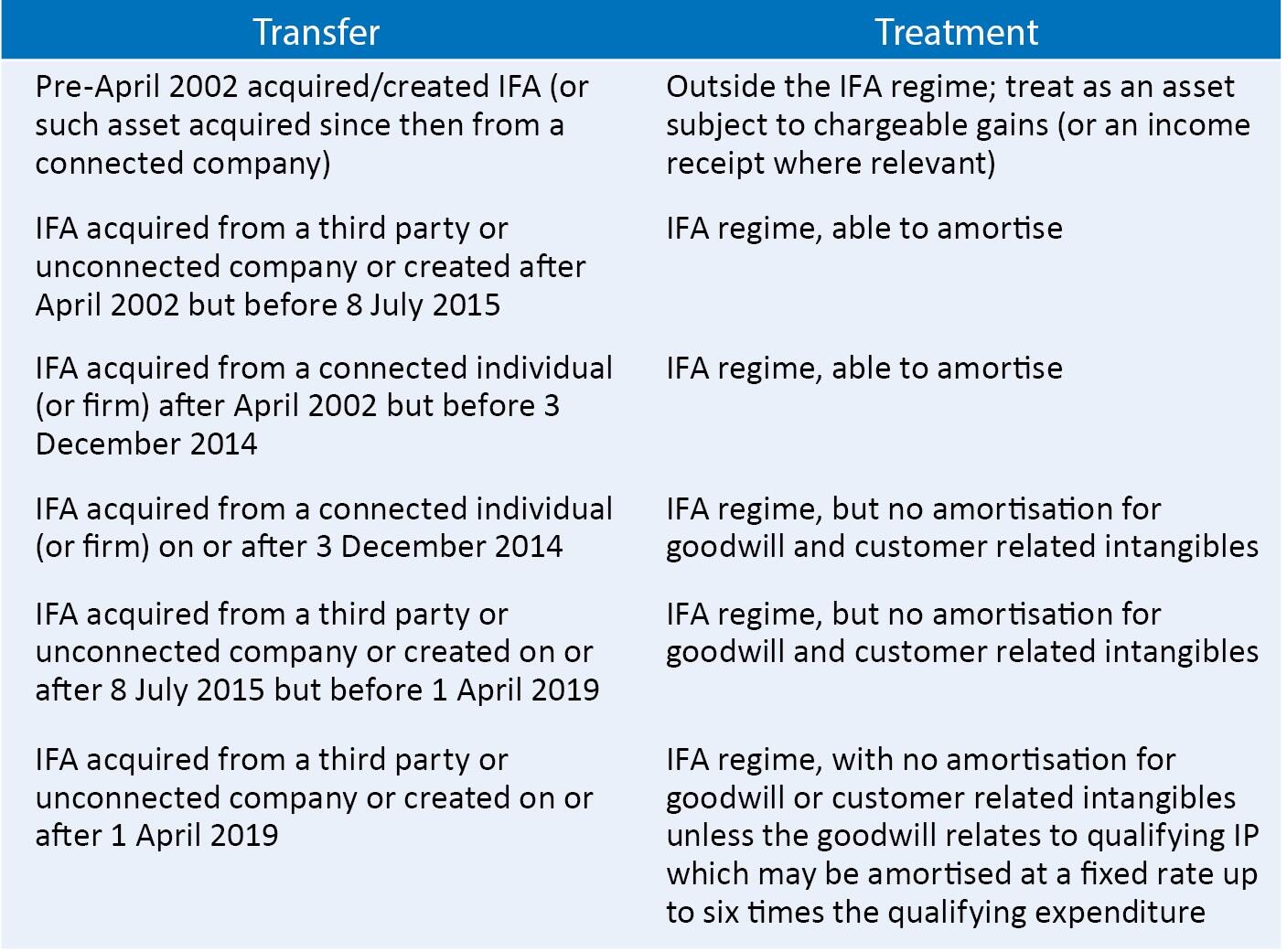

Broadly speaking, intangible fixed assets (IFAs) are (in the main) goodwill and intellectual property. As such, IFAs can be immensely valuable. The specific IFA regime was introduced for companies in April 2002. Until that time, companies’ IFAs were treated no differently from other assets and were taxed under general principles (as they still are for individuals).

The IFA regime has been changed on several occasions since. One of the benefits of the regime was the ability to amortise but from 3 December 2014, any goodwill or certain customer related assets purchased from a connected individual (or firm with a connected member) would lose the right to amortisation. From 8 July 2015, this restriction was extended to cover IFAs purchased from unconnected third parties also.

Most recently, FA 2019 Schedule 9 further amended the position (this time beneficially) by providing that goodwill, to the extent it relates to qualifying IP, acquired post-April 2019 must now be amortised at a fixed rate, currently set at 6.5%. The amortisation is however limited to six times the expenditure on that ‘qualifying IP’ (which includes patents, design rights and copyrights). Note that IFAs transferred within a corporate group should retain their characteristics prior to that transfer. By way of summary, figure 1 may be a helpful reference point.

As can be seen, the question of when the asset is acquired is key.

When connected parties transfer assets to and from each other, if those parties are also grouped, provisions can apply to make that transfer tax neutral. The IFA regime is no different, allowing grouped entities to transfer IFAs within the group on a tax neutral basis, unless and until that transferee company leaves the group at which point de-grouping charges potentially arise. The de-grouping rules for IFAs look back six years.

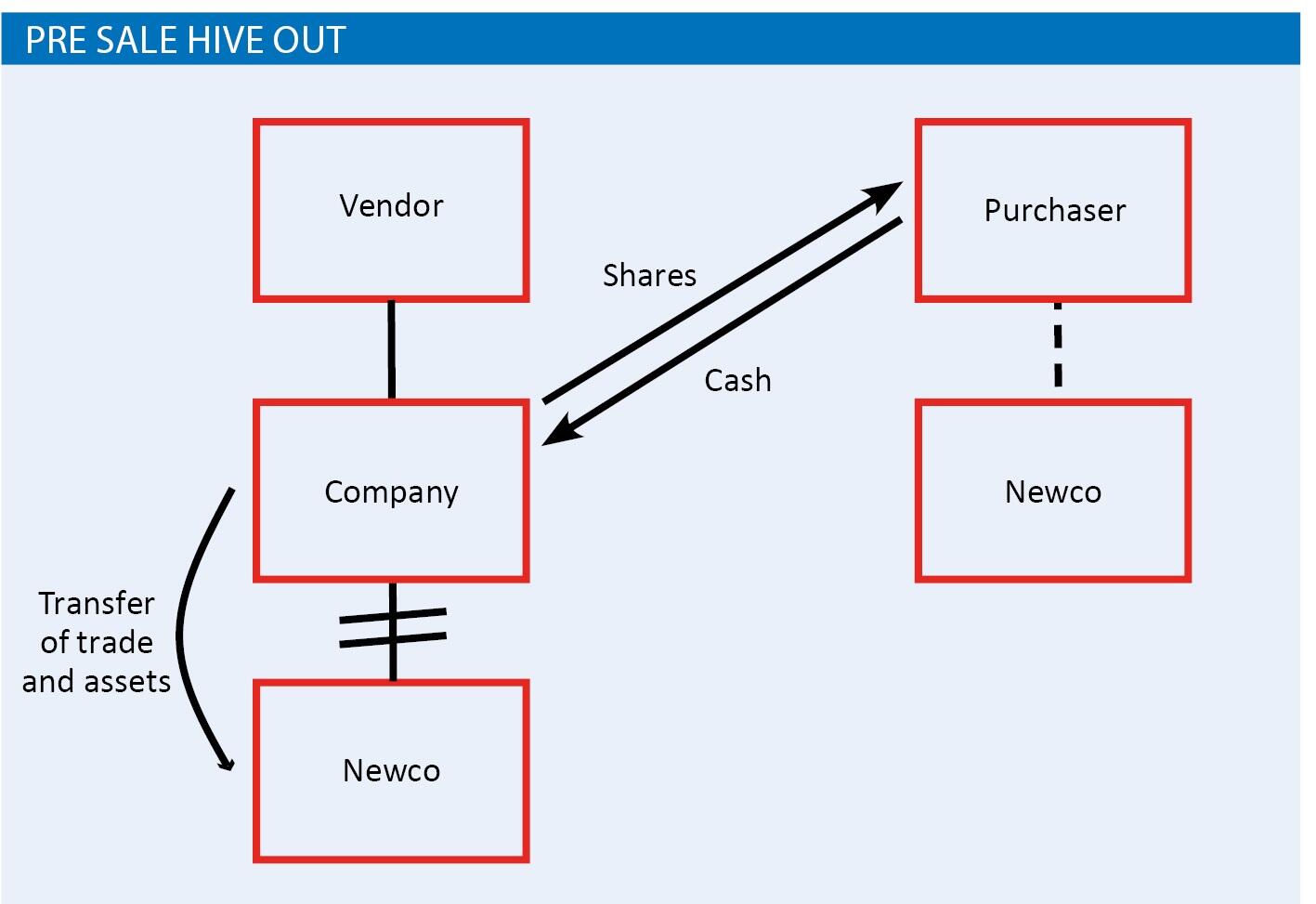

Pre-sale hive down transaction

This may be an issue where prior intra-group transfers have taken place, especially where there is a hive out scenario. A hive out prior to a sale may be considered where target Company has a trade which Purchaser wants but that target Company has been trading for many years, in many different guises and has different trades and historic tax issues or other potential liabilities. Vendor would be glad to sell target Company as the tax liabilities remain within that Company and by selling the shares Vendor removes itself from the potential risk (subject of course to any secondary liabilities or indemnity or tax covenant between Purchaser and Vendor). Purchaser of course only wants the trade and not the additional risks.

There is a commercial choice at this stage to determine whether an asset sale or share sale is the preferred route. But there is another option: the pre-sale hive out (we shall look at hive down as an example), as set out in figure 2 below.

The pre-sale hive down allows the Purchaser to get the assets it wants without the additional risks via a share sale transaction (generally considered a ‘cleaner’ transaction). Vendor receives capital gains treatment which may essentially be tax neutral if it benefits from the substantial shareholding exemption (‘SSE’).

The sticking point was often the de-grouping charge on IFAs.

Chargeable gains

To explain the point, we’ll start with the chargeable gains treatment in our example (the IFA regime was based on, and split out from, this after all).

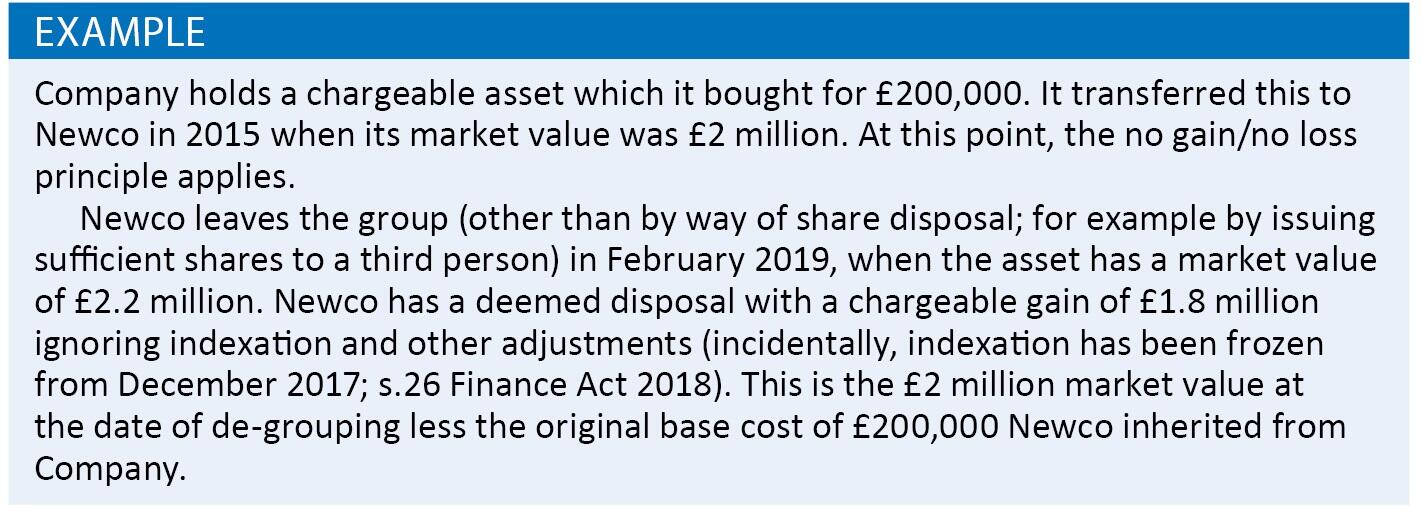

Say Company owns land (assuming the transactions in land rules do not apply) or another asset subject to chargeable gains treatment in the UK, the transfer from Company to Newco will be on a no gain, no loss basis thanks to, Taxation of Chargeable Gains Act 1992 (TCGA) s 171 (assuming the group test is met, as is the case here). The historic base cost for the Company will be the asset’s base cost for Newco.

If Newco then leaves the gains group within six years of the transfer of a chargeable asset to it whilst still owning that asset (or an asset it has rolled over the gain on the original asset into), TCGA 1992 s 179(3) applies to create a deemed disposal for Newco. Newco is treated as having sold and immediately reacquired the asset for its market value at the time of the no gain, no loss transfer. This will usually create a gain or a loss. See Example 1.

As we can see, the de-grouping charge in this situation falls on the entity leaving the group. However, should the parties so agree, a gain or loss arising under TCGA 1992 s 179 de-grouping rules can be transferred from the entity leaving the gains group to another entity remaining within the group under TCGA 1992 s 171A. This can be useful where SSE does not apply and there are capital losses which may be utilised elsewhere in the group.

SSE

Special rules apply where the de-grouping charge arises by way of share disposal which qualifies for SSE.

SSE broadly exempts any gain or disallows any loss upon the sale of shares where the specified conditions apply. For SSE to apply, the seller needs to have held 10% or more of the ordinary share capital of the target company and be beneficially entitled to 10% or more of the profits available for distribution, and the assets available on a winding up, to equity holders.

There are also trading requirements but these have recently been relaxed in respect of the seller (although still remain in respect of the company being disposed of).

As of 1 April 2017, these conditions need to have been met for the period of one year beginning no more than six years before disposal. The increase to a six year rather than two year ‘look-back period’ (following Finance (No.2) Act 2017) should help more companies have tax free gains when they eventually sell their minority shareholding (not so good for those with post-SSE sale minority holdings being held at a loss).

The chargeable gains de-grouping rules link back to SSE via TCGA 1992 s 179(3D) which provides that where the de-grouping charge arises as a result of a sale subject to the SSE, the de-grouping gain or loss is treated as forming part of the consideration for sale of the target company.

As a result, the gain is effectively extinguished by SSE. This also means that any intra-group acquired asset held at less than market value has its loss disallowed (but this is usually reflected in pricing).

For the company leaving the group, it is still treated as having sold and then immediately reacquired the chargeable assets at market value subject to de-grouping. It is just a question of whether that gain or loss is taxable/relievable (and for whom), depending on whether the sale is within SSE or not.

As a result, those chargeable assets (assuming the carrying base cost is less than market value) get a step up in base cost to the market value at the time of the intra-group transfer upon de-grouping.

SSE can therefore be immensely valuable for companies for chargeable gains purposes (although it is worth noting that the rules can disallow otherwise valuable losses arising on de-grouping and disposals for some companies).

There is an issue in our hive down scenario however, as the one year holding period is unlikely to have been met by the newly established Newco. Fortunately, TCGA 1992 para 15A Sch 7AC allows the holding period to factor in and include the time when another group company carried on the trade which is transferred to Newco. It is important, in order for this treatment to apply, for Newco to continue carrying on the trade immediately after the disposal.

Care needs to be taken at this stage however, where there was no group in the first place. In our scenario, Vendor and Company form a group which Newco then joins. This is within the remit of the TCGA 1992 para 15A Sch 7AC treatment.

What if Vendor was an individual? There would be no chargeable gains group under TCGA 1992 s 171 initially, and so, one would assume that by creating Newco as a subsidiary to the Company a group is created (of which the Company is a ‘member of the group’) thereby being within the scope of TCGA 1992 para 15A Sch 7AC.

Sadly, HMRC’s capital gains manual at CG53080C takes a different view. HMRC read the condition that the trade be carried on by a ‘member of the group, while it was a member of a group’ as meaning at a time before Newco was created, i.e., in HMRC’s view, if Company was a sole corporate entity not within a corporate gains group (for example owned by individual(s) and without any subsidiaries) then the creation of Newco does not form a group for these purposes.

Readers can take their own view on this interpretation and note that caution must be taken when deviating from HMRC guidance. The author, however, is yet to be convinced that if one sets up Newco (without the assets being transferred to it upon subscription), then this in and of itself creates a group; thereby allowing Company, in its new capacity as ‘a member of a group’, to use the assets ‘while it was a member of a group’ as prescribed by TCGA 1992 para 15A Sch 7AC.

Some may seek to create Newco earlier in time to strengthen the argument but it is likely that HMRC’s interpretation may still leave advisers and clients uneasy.

The other alternative ‘fix’ could be to create a group prior to the introduction of Newco in the structure through the addition of other companies into the structure.

Both approaches appear to be unnecessary steps indicating that HMRC’s interpretation is at odds with the draftsman’s intention (and what the legislation actually says).

One could of course take sufficient umbrage with CG53080C until ultimately the tax tribunal gives its interpretation of the provision but then again, why should taxpayers incur the cost, risk and uncertainty of tax litigation in order to correct HMRC’s over-zealous narrowing of tax legislation? Such considerations are beyond the scope of this article.

IFA

Turning back to the treatment of IFAs, unlike chargeable gains which have been linked to SSE via the treatment described above since 2011, Finance Act 2011 made no amendment to the IFA de-grouping charges.

As a result, the transfer of IFAs from, in our example, Company to Newco will be tax neutral pursuant to Corporation Tax Act 2009 s 775 but, without the link to SSE, a de-grouping charge could previously arise under CTA 2009 s 780. That provision works in a similar way to the de-grouping charges for chargeable gains provision, with Newco being subject to a deemed realisation of the IFA and immediate market value reacquisition as at the time of the intra-group transfer.

From 7 November 2018 however, FA 2019 s 26 introduced new CTA 2009 s 782A which effectively removes any de-grouping debit or credit arising in respect of an IFA where the requirements of SSE are met.

Interestingly however, instead of allowing the IFA to become part of the consideration for the share disposal (as is the case for chargeable assets), CTA 2009 s 782A is an exclusion to the provisions of CTA 2009 s 780 taking effect (new CTA 2009 s 780(5)(aa)).

As a result then, the legislation whilst allowing a company to be sold without creating a de-grouping charge, does not allow a tax written down value (TWDV) step up/down to market value (which was the case for the chargeable assets’ step up in base cost). Newco will still hold the initial TWDV for the asset (which it inherited from Company) and so will still be taxed on any future disposal of the IFA based on the difference between the TWDV (upon sale) and the proceeds received.

One rationale behind this is presumably that tax relief may have been provided during the life of the asset through amortisation (if available). The potential issue with this is that it is the Vendor which may have had the benefit of that amortisation prior to the Purchaser acquiring the asset. Purchaser due diligence should therefore still focus on IFAs, particularly if the Purchaser ever intends for Newco to sell the intra-group acquired IFA (and ensure that the purchase of Newco is priced accordingly).

A charge may not arise on purchase of Newco, but if the IFA asset has increased in value but been subject to amortisation (for example at a fixed rate thereby potentially diverging from economic reality) during the time when the Vendor group owned the asset, the amortisation is effectively recovered by HMRC from the Purchaser on any future sale (if at a price higher than TWDV). Again, the effect of this will be subject to the amortisation position of the relevant IFAs; and as such, the relevant time when the asset was acquired as discussed above.

On the whole then, although Purchasers should still be wary if they intend to realise any IFAs post-acquisition and factor this into their deliberations (or price) the removal of the de-grouping charge will still be incredibly beneficial in not creating immediate tax charges. As such, the changes should remove one of the frictions in M&A transactions.