More than meets the eye

Share this article

Meredith McCammond and Samantha Mann provide guidance on dealing with minimum wage arrears

Key Points

What is the issue?

A combination of increasing awareness around underpayments and extra resources for HMRC’s enforcement team, mean that more employers than ever may find themselves needing to pay minimum wage arrears.

What does this mean for me?

An adviser may need to process arrears as part of a payroll service or otherwise advise on it. Are you clear on what happens with tax, National Insurance and related matters such as pensions?

What can I take away?

It is not a simple case of paying the arrears in one lump sum and deducting tax and NIC in the current year.

The National Minimum or Living Wage (NMW/NLW) is the minimum pay per hour most workers are entitled to by law. As discussed in the article ‘Living with the NMW’ in January’s edition, the minimum wage is a significant risk for employers, and underpayments can easily arise.

Workers may be due arrears going back six years, and further guidance on calculating minimum wage arrears can be found in BEIS’s NMW guidance, starting at page 48. The payment an employer needs to make is the total arrears less the tax, NIC and any other deductions such as pension contributions. Here, we look briefly at the rules for such deductions and tell you where to find more information.

Tax

Arrears of pay in minimum wage cases are taxable as ordinary employment income under ITEPA 2003 s 62. In accordance with rule 2 of ITEPA 2003 s 18(1) the tax liability arises in the year of entitlement not the year of payment. It may be the case that this is the same thing – the current tax year, in which case, any back pay can just be paid through the payroll with PAYE tax and NICs calculated in the normal way.

However, entitlement to receive the back pay will often have arisen on an ongoing basis throughout the employment. Applying the ‘entitlement’ principle means that a lump sum of back pay may give rise to taxable earnings in several tax years. Under rule 2 of ITEPA 2003 s 686(1) the payments should also be subject to PAYE on the same basis, that is when entitlement arises. This treatment is usually beneficial to an employee because if the arrears are taxed in the usual way, in one go in the year of receipt, they could push the employee’s earnings into a higher tax bracket.

According to current HMRC employer guidance (CWG2: further guide to PAYE and NIC in section 1.19.2) there are two ways that an employer can deal with the PAYE on the award for any closed tax years. If arrears are due in respect of pre RTI years and a workforce at large, the amounts due can sometimes be calculated by way of a central agreement (‘class 6 settlement’) reached with HMRC. Such special arrangements are allowed under Regulation 141 of the PAYE Regulations to ease matters for employers, employees and HMRC.

Alternatively, employers should allocate the arrears of pay between the tax years in which the payment should have been made and calculate and deduct tax for each closed year in accordance with the employee’s tax code for the year and as if the additional pay had been paid at ‘week 53’ (further detail is set out in PAYE Manual 70023). Employers should submit an Earlier Year Update (EYU) for each of the employees concerned for all relevant years.

Some commercial software will not have this facility or will require a significant ‘roll back’ of previous calculations to be completed in order to give effect to the adjustment. In such cases, employers may need or prefer to use HMRC’s Basic PAYE Tools to submit the EYU if they are not using it already (further guidance on using BPT alongside commercial software can be found on GOV.UK). As EYUs are being submitted to account for the tax, HMRC say that each year will attract its own interest charge for late payment. For example – arrears paid for tax year 2016-17 will be subject to interest from 19 April 2017 until the day payment is made. HMRC’s guidance does not cover penalties – it is conceivable that these scenarios may slip past the PAYE penalty system.

The employee is always assessable upon the gross arrears for each year and is entitled to a credit for the PAYE tax referable to each year. The ‘week 53’ procedure will often see a worker receiving an extra ‘slice’ of personal allowance and so underpaying tax. Strictly, HMRC could seek to claw this money back, however they tend to operate a £50 de minimis where items cannot be easily coded out (as set out in PAYE Manual 12070) which may cover it.

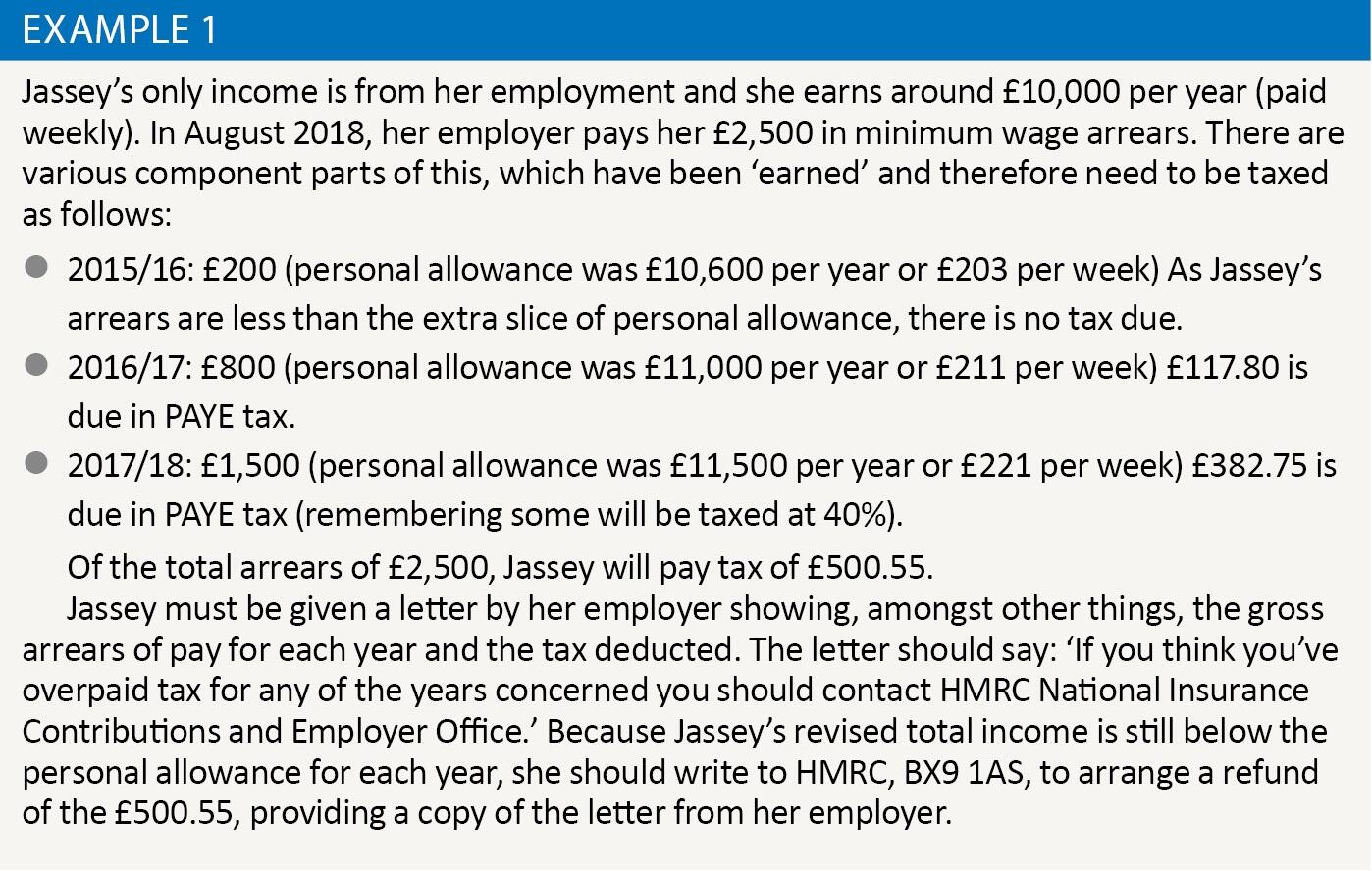

On the other hand, this procedure can still mean a low-paid worker overpays tax, as we can see in example 1.

National Insurance

The NIC element is worked out differently, and is calculated on the basis of the year the payment is made only: it is not related back to prior years. This can save the employee money as depending on how large the arrears are and what other income there is in the pay period, some of it will only be liable for 2% NIC, as compared to 12%.

An employer should report the NICs through RTI on a Full Payment Submission (FPS) for the pay period in which the payment is made. Support may be required from the software provider concerned as to how to process payments for NIC purposes but not tax purposes.

Social Care Compliance Scheme

It has been identified that some social care sector employers may not have been paying the minimum wage for sleep-in shifts by their carers. Further information on the issue around sleep in shifts can be found on LITRG’s specialist website for care and support employers (e.g. New Social Care Compliance Scheme launched – but independent advice essential).

To help reduce the administrative burden on these employers, HMRC will allow employers who have joined the ‘Social Care Compliance Scheme’ to deal with the tax implications of these arrears using an Alternative PAYE Arrangement (APA). Under the APA, employers will deduct tax at 20% from the taxable income for each employee. This arrangement means they will not be required to submit EYUs for each individual payment made. Instead employers will need to complete and return a spreadsheet to HMRC showing the amount of arrears paid, the year they relate to and the tax deducted.

As part of the APA, no interest will be charged for late payment. If an employer chooses not to use the APA they will need to operate PAYE using the ‘week 53’ rules. It is worth noting that discussions are taking place as to whether the Government can help social care employers fund pay arrears (and thus, by extension, any PAYE due). Other employers in financial difficulty or with cash flow problems, and with PAYE to pay, could consider applying for an HMRC Time to Pay agreement. (Update: since first writing this article, a Court of Appeal decision has overturned the ruling that sleep-in shifts need to be paid at minimum wage, however this looks set to be further appealed. It is unclear what these developments mean for the Social Care Compliance Scheme and we await comment from HMRC.)

Pension

If an employer identifies that they need to pay minimum wage arrears to a member of staff, they may need to put the employee into a workplace pension scheme when the minimum wage arrears for a pay period are included as income, or put them in from an earlier date. They may also need to calculate backdated contributions. If the employer has had their first re-enrolment date they will also need to repeat their re-enrolment assessment. The Pensions Regulator (TPR) has detailed guidance available on its website to help employers/advisers dealing with pay arrears (please note this has been specifically developed to assist social care sector employers. We understand from TPR that it is largely applicable more widely, however ‘normal’ arrears should be calculated at the current contribution rates rather than the rates due at the time the arrears arose).

Other considerations

Other deductions an employer may need to consider in relation to pay arrears include statutory payments, the Apprenticeship levy, Student Loan deductions and Attachment of Earnings Orders, but these are all subjects for another article! Hopefully what is here will help you to deal with most situations you come across.

Finally, employers and advisers should be aware that arrears payments may impact any benefits or tax credits employees receive (in the past, HMRC may have been able to come to specific agreements for tax credits under class 6 settlements, however in line with general principles pay arrears are treated as employment income in the year of receipt). Non-declaration by an employee could lead to overpayments or even a penalty, so it is vital that they tell HMRC/DWP/local authorities etc. about any arrears as soon as possible (even if the increase in income then falls to be disregarded for benefits or tax credits purposes). The letter that the employer has to provide to the employee for tax purposes (referred to in the Jassey example) could be expanded to point the employee in the right direction on benefits and tax credits.

Conclusion

As this article shows, there is more to dealing with minimum wage pay arrears than simply processing them as pay in the current period, although many employers may not be aware of these rules and so do this anyway. If this does happen, the employee should contact HMRC and ask that the arrears are assessed on the proper basis.

Of course the best approach is to avoid arrears completely by getting minimum wage pay right in the first place, but this isn’t always as easy as it sounds. In this respect, clear and comprehensive guidance for employers and their advisers is key and it is probably not all that controversial to say that a refocus on this from policy owners BEIS, as well as the enforcers HMRC, would be welcome.