Moving the EU goalposts

Share this article

In the first of two articles, Neil Warren considers practical VAT issues that will apply from 1 January 2021 when the UK’s transitional deal ends with the EU, focusing on reporting requirements and VAT returns

Key Points

What is the issue?

Major VAT changes will take place on 1 January 2021 when the UK’s transitional deal ends with the EU. The article considers changes to returns currently submitted by a UK business and how these will change in the future.

What does it mean to me?

Intrastat arrivals declarations must still be completed in 2021 but dispatch reports will end, as will EU Sales Lists apart from in Northern Ireland.

There will be new procedures for dealing with the mini one stop shop (MOSS) scheme and also claiming VAT paid in other EU countries.

What can I take away?

The introduction of postponed accounting for VAT on worldwide imports of goods will provide a cash flow boost for UK businesses. However, care is needed to ensure VAT returns are completed correctly – the article gives practical examples.

Although the UK officially left the EU on 31 January, the status quo on trading arrangements continued after this date. The key date when the goalposts will move in dramatic fashion will be 1 January 2021. In this article, I will consider what reports and returns will remain and which will disappear. There are a couple of surprises on this issue.

VAT return boxes

HMRC’s extensive guidance published in July makes it very clear that trading in goods with EU countries will be the same as for non-EU countries. In other words, references to goods sold into the EU as ‘dispatches’ will end, as will the description of ‘arrivals’ for goods coming into the UK. Northern Ireland is an exception. A recent HMRC letter sent to businesses refers to a ‘full external border with the EU’.

So, a logical question to ask is whether the current nine boxes on UK VAT returns will be reduced to six. This is because Boxes 2, 8 and 9 solely relate to trading in goods with EU suppliers and customers. The answer is ‘no’ because these boxes will still be needed by businesses based in Northern Ireland, which will continue to make acquisitions and dispatches as part of the Northern Ireland Protocol. But for businesses based in Great Britain, only six boxes will be relevant from 1 January 2021.

Postponed accounting

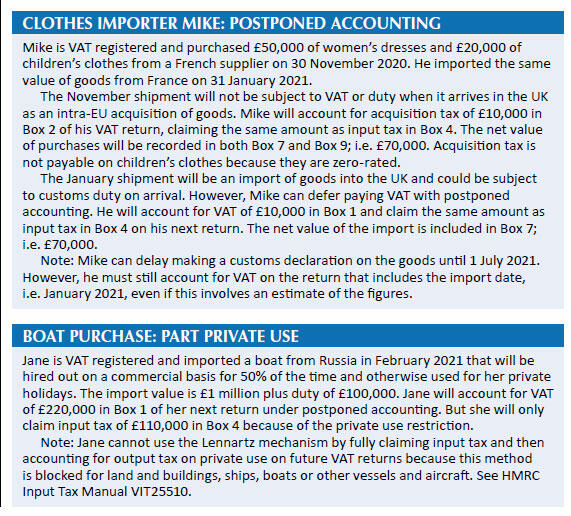

An important change for VAT on imports will be the introduction of postponed accounting from 1 January 2021. This will apply to imports from EU and non-EU countries and will provide a massive cash flow boost for VAT registered importers. VAT payable on goods coming into the UK from anywhere in the world can be postponed at the point of entry and included on the importer’s next VAT return, instead of being paid on arrival and subsequently claimed as input tax. See Clothes importer Mike: postponed accounting.

I have worked in VAT long enough to remember when we last had postponed accounting in the UK before it was abolished in 1984. The abolition produced a one-off cash flow boost of £1 billion for the government at the time because it resulted in a time delay between paying VAT at the border and then claiming input tax. The opposite now applies and there will be a negative cash flow outcome for the government. An importer that is not VAT registered will pay VAT when the goods arrive in the UK.

Input tax

Postponed accounting will produce extra compliance challenges to HMRC. Think about a new business that imports a big piece of machinery from a non-EU supplier. Under current procedures, the import VAT is likely to produce a large repayment claim by the business on its first VAT return, which HMRC often verifies before making the repayment. However, if import VAT is postponed when the machine enters the UK, the Box 1 and Box 4 compensating entries will mean that no repayment return will be submitted.

The other potential risk is that a business owner might forget to adjust the Box 4 input tax for any private or non-business use of the imported goods. The Box 4 entry must pass the same input tax tests as a purchase invoice received from a UK supplier. See Boat purchase: part private use.

Intrastat

A big surprise when I read the HMRC guidance is that Intrastat declarations must still be completed in 2021 for arrivals of goods from the EU. The guidance was silent about Intrastat dispatch returns but HMRC has since confirmed that these declarations will not be required (see below). Intrastat reports must currently be completed by UK businesses that annually sell more than £250,000 of goods to VAT registered customers in the EU or buy goods from EU suppliers exceeding £1.5 million.

I contacted the HMRC press office for a steer: ‘The UK government has taken the decision to introduce the new border controls in stages up until 1 July 2021. This means businesses have the opportunity to delay the submission of customs declarations for imports from the EU into GB. As from 1 January 2021, the customs declaration would be used to compile trade statistics for imports from EU member states but this could leave the UK with significant gaps in the information available to compile import statistics. HMRC needs to carry on requiring businesses to submit Intrastat arrivals declarations for goods received in GB from the EU during 2021.’

This outcome makes sense, and the spokesperson confirmed the situation with Intrastat dispatch returns: ‘Our intention is that we will not be requiring businesses to provide Intrastat dispatches declarations for exports from GB to the EU as we will collect this information from export customs declarations.’

EC Sales Lists

EC Sales Lists will only be needed for sales of goods to EU businesses that are treated as intra-Community dispatches under the terms of the Northern Ireland Protocol. They will not be required for any supplies of services or for any supplies of goods relevant to Great Britain. This is good news for businesses – a welcome saving of time and administration costs.

Reclaiming VAT paid in EU countries

A UK business registered for VAT currently reclaims VAT paid in other EU countries by submitting an online claim to HMRC, which is forwarded to the tax authority of the other country. Claims for a calendar year must be made by the following 30 September but can be made quarterly during the year, with a sweep up claim at the end of the year. From 1 January 2021, this procedure will no longer apply. A UK business must submit individual claims to each tax authority where VAT has been paid. This will usually be a paper form. In VAT speak, UK businesses will move from submitting what are commonly known as ‘8th Directive’ claims to ‘13th Directive’ claims. The deadline dates for submission need to be checked for each EU country.

MOSS returns

B2C supplies in the EU of broadcasting, telecommunication and electronic services are taxed according to the VAT rate that applies in the customer’s country. The mini one stop shop (MOSS) return is the way a business pays this tax at the end of each calendar quarter.

A UK business making B2C digital supplies does not currently have to worry about MOSS if total annual B2C sales in the EU are less than £8,818; i.e. 10,000 Euros. However, there will be major changes from 1 January 2021:

- The £8,818 threshold will end - a zero threshold will apply instead.

- A UK business making MOSS sales must register in an EU country of its choice under the non-EU MOSS scheme and submit returns and pay tax in that country. The alternative is to separately register for VAT in each EU country where digital supplies are made, which will be very time-consuming.

- The final UK MOSS return will include sales up to 31 December 2020 and be submitted by 20 January 2021.

See bit.ly/307gTyJ for further information.

Final tips

If your clients import or export goods, they must apply for an Economic Operator Registration and Identification (EORI) number from HMRC as soon as possible if this has not already been done.

A ‘GB’ number is needed for both importers and exporters.

The application process only takes about 15 minutes, and numbers are usually issued within seven days.

See www.gov.uk/eori.

In my next article, I will consider the new procedures for moving goods to and from the UK after 1 January; how the VAT outcome can change if the consignment value is more or less than £135; and what will happen if Online Market Places and overseas businesses are involved in a deal. There are some interesting twists!