A much broader scope

Share this article

Michelle Robinson reviews the Fifth Money Laundering Directive, setting out which trusts will be required to register and deadlines for the provision of information to HMRC

Key Points

What is the issue?

Under the EU’s Fifth Money Laundering Directive, registration will be required by a significantly greater number of trusts than under the existing trust register. Information held on the trust register will also be more widely available to the public under the new directive.

What does it mean for me?

Trusts must register for 5MLD purposes if the trustees are liable to pay UK income tax, capital gains tax, inheritance tax, stamp duty land tax, land and buildings transaction tax (Scotland), land transaction tax (Wales) or stamp duty reserve tax.

What can I take away?

Trustees and their advisors will need to determine whether or not they are required to register under the directive and, if so, by when; and of the increased ability for information to be accessed by the public.

The final regulations enacting the EU’s Fifth Money Laundering Directive (5MLD) into UK law took effect from October 2020. As a result, registration will be required by a significantly greater number of trusts than under the existing trust register, which was set up to comply with the Fourth Money Laundering Directive (4MLD). In addition, information held on the 5MLD trust register will be more widely available to the public than it is under 4MLD.

This article summarises key points with regard to the 5MLD trust register and focuses on which trusts will be required to register and the extent to which information will be publicly available.

A summary of deadlines for provision of information to HMRC is also provided. This article does not detail what information must be provided to HMRC.

Trusts required to register

Scope of the registration requirements 5MLD requires the following express trusts to register:

- All UK trusts, including non-taxable trusts. UK trusts are trusts where all the trustees are UK resident or where at least one trustee is UK resident and the settlor was both UK resident and UK domiciled when the trust was set up and/or when the settlor added funds to the trust.

- Non-UK trusts that incur a UK tax liability on UK income or UK assets, as under 4MLD.

- Non-UK trusts that acquire an interest in UK land after 5 October 2020.

- Non-UK trusts with at least one UK resident trustee that, after 5 October 2020, enter into a business relationship with a UK relevant person (such as tax advisers and financial institutions) which is expected to be of at least 12 months’ duration.

Non-taxable trusts are not required to register if they are ‘excluded’ trusts. Additionally, some non-taxable trusts are not required to register with HMRC if they are registered in the European Economic Area (EEA). These points are considered in more detail below.

UK tax liability

Trusts are taxable for 5MLD purposes if the trustees are liable to pay UK income tax, capital gains tax, inheritance tax, stamp duty land tax, land and buildings transaction tax (Scotland), land transaction tax (Wales) or stamp duty reserve tax.

Non-UK trusts are only required to register where a UK tax liability arises on UK income or assets. This means that registration is not required due to the trustees having a tax liability if the trustees’ only liability to UK taxation is inheritance tax on indirectly owned UK residential property (e.g. where UK residential property is owned by an underlying offshore trust company).

Residence

Trustees who are individuals are UK resident for 5MLD purposes if they are UK resident for any of the taxes set out above. In practice, this means residence under the statutory residence test for income tax and capital gains tax purposes and/or, from 1 April 2021, under the stamp duty land tax residence test that the government has announced will apply from that date.

Excluded trusts

Some non-taxable trusts do not need to register with HMRC under 5MLD because they are considered to present a low risk of being used for money laundering or terrorist financing. These include:

- trusts for bereaved minors and vulnerable beneficiaries;

- will trusts created on death that only receive assets from the estate and which are wound up within two years of death;

- trusts that hold life insurance or retirement policies that only pay out on the death, terminal or critical illness or permanent disablement of the person assured, or to pay the healthcare costs of the person assured;

- UK registered charitable trusts;

- co-ownership trusts where the trustees and the beneficiaries are the same persons;

- UK registered pension schemes;

- certain share incentive plans; and

- trusts in existence before 6 October 2020 that hold assets worth £100 or less.

There are some notable exceptions from the exclusions. Registration is required by trusts that are:

- taxable, due to incurring a tax liability (as set out above).

- ‘new’ trusts created after 5 October 2020 of any value, unless the trust is not taxable and is within an excluded category;

- pre-6 October 2020 trusts with assets worth more than £100. This will include many longstanding trusts that do not require active management or ongoing engagement with HMRC, such as trusts created on death entitling a surviving spouse to occupy the family home for life with the property passing to the children thereafter; and

- bare trusts and co-ownership trusts which have different trustees and beneficiaries.

Trusts registered in the EEA

5MLD is an EU-wide directive and all EU member states and the UK must maintain their own 5MLD compliant trust beneficial ownership registers. 5MLD states that the national registers must be interconnected via a European Central Platform by 10 March 2021.

UK trusts and non-UK trusts with at least one UK resident trustee will not need to register on the UK register if they are registered on an EEA trust register, provided the trust is not taxable.

Non-UK trusts that do not have any UK resident trustees will need to register if the trustees acquire UK land even if no UK tax is payable. Information about such trusts will be less broadly available than for other types of trust (see below).

Access to information

HMRC will continue to administer the trust register. At present, information held on the 4MLD register is only accessible to law enforcement agencies and financial intelligence units.

Under 5MLD, information held on trusts will, in addition to law enforcement agencies and financial intelligence units, be available on request to those with a ‘legitimate interest’ in the information held. HMRC published guidance on 25 January 2021 which states that: ‘HMRC will give information to an outside party only if there is strong evidence to show that the trust could be linked to money laundering or terrorist financing’ (see bit.ly/3r9T3xP). This is subject to some exceptions which are noted below.

There is no legitimate interest requirement in order to access information where a trust holds a controlling interest in a non-EEA legal entity. The exception is that this wider access rule does not apply to non-UK trusts that only have non-UK trustees and which acquire UK land – requesters must have a legitimate interest in order to access information about these types of trust.

The disclosure rules above are overridden and HMRC will not share information if it considers that:

- it should be exempt from disclosure because it relates to minors or persons who lack mental capacity, as defined in Statutory Instrument 2017/692; or

- releasing the information would result in the trust’s ‘beneficial owner’ (as defined) facing a disproportionate risk of fraud, kidnapping, blackmail, extortion, harassment, violence or intimidation.

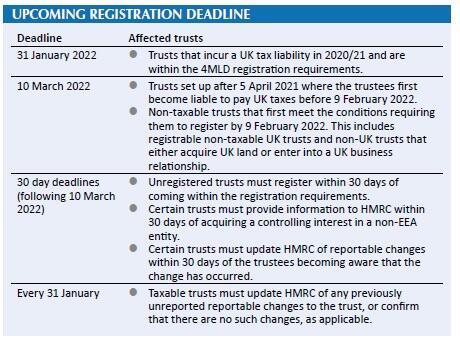

Registration deadlines

Existing trusts that are newly brought within the scope of the trust registration requirements by 5MLD (i.e. non-taxable trusts) must register by 10 March 2022. Any registered trusts that are required to provide additional information under 5MLD must provide it by the same date. Non-taxable trusts will not be able to register until later in 2021, pending HMRC’s systems being updated to enable them to do so.

Trusts that come within the registration requirements from 9 February 2022 must register within 30 days of doing so. A 30 day deadline also applies to update HMRC of any reportable changes to the trust.

In the meantime, trusts that are required to register under the 4MLD registration requirements must continue to do so. This means that taxable trusts must register by the 31 January following the tax year in which the registration requirements are first triggered. Taxable trusts that are already registered must inform HMRC of any relevant changes or confirm that there are no reportable changes by the 31 January following the end of the relevant tax year.

The upcoming deadlines to register or update the register are as set out in the table. In practice, trusts may need to register earlier than is required for trust registration purposes; e.g. by 5 October following the tax year in which an income or capital gains tax liability arises, if the trustees need to notify HMRC of chargeability.

Conclusion

5MLD will greatly increase the number of trusts required to register with HMRC. Trustees and their advisors will need to determine whether or not they are required to register under 5MLD and, if so, by when. Trustees and beneficial owners of trusts should also be aware of the increased ability for information held on registered trusts to be accessed by those with a legitimate interest.

Note: After this article was written, on 15 March 2021 CIOT published an announcement from HMRC stating that, due to delays in expanding the online registration system for non-taxable trusts, the deadlines for registering such trusts will be deferred until approximately 12 months after HMRC’s system is updated to allow such trusts to register. HMRC will publish further updates and clarifications in due course.