Non-reportable employee benefits and PAYE Settlement Agreements

Share this article

We examine the items which are commonly exempt from reporting obligations for employee benefits, as well as covering PAYE Settlement Agreements and payrolling benefits under HMRC’s statutory regime.

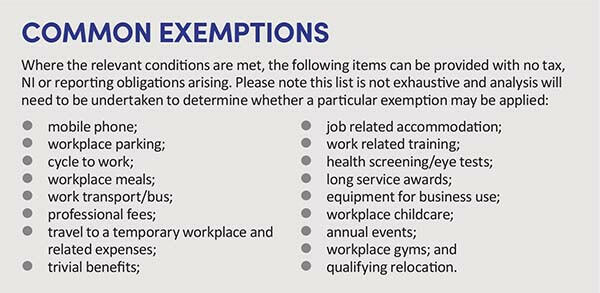

The distinction between an exemption from tax and a deduction that can be claimed by the employee is an important one, particularly when considering the treatment of cash reimbursements to employees. Whilst some further explanation is outlined below, some common examples of items that may be treated as exempt for income tax, National Insurance (NI) and reporting purposes are listed in Common exemptions.

Exemptions

There are a number of benefits that are specifically exempted from tax and NI where the relevant conditions are met (the majority are outlined in the Income Tax (Earnings and Pensions) Act 2003 (ITEPA 2003) Part 4 ss 227 to 326B)). Where the conditions are met, no reporting requirements and/or liabilities arise for the employer. However, determining whether an exemption is available is becoming increasingly complex for a number of reasons, including a divergence between the strict terms of some exemptions and common working practices (exacerbated by Covid-19) and changes of approach by HMRC.

For example, whilst some exemptions apply to both ‘the provision’ of a benefit and cash reimbursements made by an employer (e.g. workplace parking), many exemptions do not extend to cash reimbursements. A common example of this is the exemption for an eye test (ITEPA 2003 s 320A). Whilst HMRC accepts that this extends to the provision of a non-cash voucher to obtain an eye test, it does not extend this to cover cash reimbursements.

Given this lack of flexibility, care needs to be taken by employers to consider whether the conditions have actually been met for an exemption to apply and that a process is put in place to ensure that any taxable cash reimbursements are processed via the payroll for both tax and NI purposes. Where an employer would prefer to cover the employee’s tax/NI liability on such reimbursements, this could be grossed up via the payroll. However, given both the cost of this and the administrative burden of processing this in ‘real time’, employers should consider entering into/ including such items in a PAYE Settlement Agreement (see below).

Of particular complexity is the application of the trivial benefits exemption (ITEPA 2003 s 323A), introduced with effect from 6 April 2016 to provide clarity as to what small benefits can be provided to employees without an income tax, NI or reporting obligation arising. Broadly, the trivial benefits exemption can apply where:

a) the benefit is neither cash nor a cash voucher (e.g. a cheque);

b) the cost (including VAT) to the employer of providing the benefit does not exceed £50 per person;

c) the employee is not contractually entitled to receive the benefit and it is not provided under a salary sacrifice arrangement; and

d) the benefit is not provided in recognition of services performed, or to be performed, in the course of the employment.

Whilst this was originally applied liberally by employers, HMRC has been narrowing the application of the exemption; for example, stating that condition (a) has not been met where cash reimbursements are made (see EIM21866). HMRC is offering no flexibility in this regard. For example, it has confirmed that the exemption does not apply to any cash reimbursements for flu jabs, despite the fact that this was the only practical option available to a number of employers during Covid-19.

HMRC has also been restricting the application of each of the other conditions above. As such, any employers that have previously relied on this exemption should review the items to which it has been applied in order to consider whether HMRC’s narrower interpretation of the conditions has been met.

Deductions

Since April 2016, amounts that would be deductible for the employee (under ITEPA 2003 Part 5 ss 327-385) can be treated as exempt where reimbursed by the employer. Expenses are tax deductible for the employee if they are incurred wholly, exclusively and necessarily in the performance of the duties of the employment (ITEPA 2003 s 336).

When deciding if the payment is tax deductible under this general rule, HMRC considers both of the following, namely whether:

- a particular employee needed to incur the expense; and

- any employee carrying out the duties of the employment would have incurred the expense.

Aside from any items covered by s 336, the most common deductible item(s) covered by employers is travel to a temporary workplace and related expenses.

As an aside, expenses incurred by an employee on the terms outlined above that are not reimbursed by the employer can be claimed as a deduction against taxable income by the employee.

Temporary Covid-19 easements

In response to the Covid-19 pandemic, a number of Covid-19 easements were introduced (as set out below). Where a benefit meets the conditions of one of these easements, neither a tax, NI nor reporting requirement arises and therefore this item should not be included in any benefit reporting for the 2021/22 tax year. In addition, HMRC has also published guidance on the treatment of certain benefits and expenses provided during the pandemic (see ‘How to treat certain expenses and benefits provided to employees during coronavirus (Covid-19)’ at bit.ly/37jEu5O.

Any positions taken regarding these easements will now need to be reviewed (or reviewed ahead of the 2023/24 tax year in the case of Covid-19 tests) and a process put in place to capture any taxable items.

Covid-19 antigen tests: The government introduced a temporary tax exemption and NI disregard for any relevant coronavirus antigen/viral ribonucleic acid (RNA) tests (but not any antibody tests) provided by an employer, where the relevant conditions are met. This is a temporary measure for any relevant test provided by an employer from 8 December 2020 for tax purposes and 25 January 2021 for NI purposes, until the end of the 2022/23 tax year (i.e. to 5 April 2023). HMRC will exercise its collection and management discretion and will not collect tax and NI due on the cost of any tests from 6 April 2020 to the date the relevant legislation came into force.

Homeworking equipment: The government introduced a temporary tax exemption and NI disregard for expenses reimbursed to employees to cover the cost of equipment needed by employees who were required to work at home due to Covid-19, where the relevant conditions are met. This measure has effect for amounts reimbursed from 11 June 2020 until the end of the 2021/22 tax year (i.e. to 5 April 2022). HMRC will exercise its collection and management discretion and will not collect tax and NI due on any reimbursed payments made from 16 March 2020 to 11 June 2020.

Cycle to work scheme: One of the conditions for an employee to benefit from the tax exemption for employer-provided bicycles and safety equipment is that the employee uses the bicycle and equipment mainly for ‘qualifying journeys’ (broadly travelling to or from work or in the course of work). Restrictions imposed by the government to combat the Covid-19 pandemic have meant that many employees have been required to work from home and have not, therefore, been able to make the qualifying journeys to work, such that the conditions for the tax exemption may not have been met. To prevent a tax charge arising, the ‘qualifying journeys’ condition was temporarily removed for employees who joined and received their cycling equipment on or before the 20 December 2020. The easement was in place until 5 April 2022, after which point all the conditions must be met for the exemption to be available.

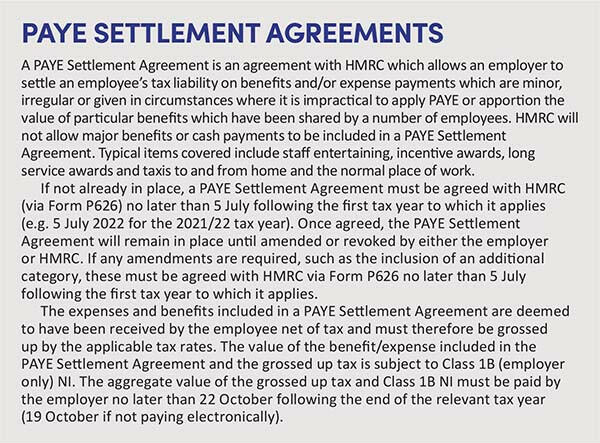

PAYE Settlement Agreement

Employers can choose to settle an employee’s tax liability on certain benefits and expense payments via a PAYE Settlement Agreement (see PAYE Settlement Agreements). Where included in a PAYE Settlement Agreement, the relevant item does not need to be included in either Form P11D or Form P11D(b). Settling the tax and NI via a PAYE Settlement Agreement can be expensive. For example, applying the 2021/22 rates for England and Northern Ireland, the additional tax and NI cost on top of the cost of the benefit is:

- 42% for basic rate taxpayers;

- 90% for higher rate taxpayers; and

- 107% for additional rate taxpayers.

However, given both the administrative burden of calculating and reporting the taxable value for each relevant employee, as well as the ethics of expecting employees to pay tax on something that is intended to be a reward (e.g. a thank you voucher or a social event), many employers choose to bear the additional cost.

It should further be noted that including items in a PAYE Settlement Agreement is generally administratively simpler and cheaper than grossing items up via the payroll. Such gross up can also cause issues; for example, for employees receiving universal credit and/or the level of taxable income for purposes such as the high income child benefit charge, personal allowance tapering and capital gains tax rates.

The temporary increase to NI for the 2022/23 tax year will mean that these costs increase. However, this increase does not impact the PAYE Settlement Agreement liabilities due to be paid by 22 October 2022, given that such liabilities should be calculated by reference to the 2021/22 Class 1B NI rate of 13.8%.

Image

Payrolling benefits in kind

Subject to formal agreement from HMRC, since 6 April 2016, employers can voluntarily elect to payroll certain benefits in kind, thereby removing the requirement to report these benefits on Form P11D, although the value of any benefit subject to Class 1A NI will still need to be reported via Form P11D(b) for Class 1A (employer only) NI purposes.

Since 6 April 2017, all benefits other than accommodation and beneficial loans can be processed via the payroll. Employers must register online to payroll benefits and notify HMRC which benefits they wish to payroll. Registration can be completed any time up to 5 April of the tax year preceding the first tax year a particular benefit will be payrolled (i.e. on or before 5 April 2022 for the 2022/23 tax year). Registration is for a full tax year and is automatically carried forward unless HMRC is informed otherwise.

As well as notifying employees following registration that benefits are being payrolled and outlining what this means for the employee (including any potential impact on their tax code), employers must also provide specified information to employees on or before 31 May after the end of the tax year for which benefits were payrolled. Whilst this can be included in a separate statement, many employers include the relevant information as part of the employee’s payslip.

Since 6 April 2021, informal arrangements to payroll benefits are no longer accepted by HMRC. Any benefits not payrolled (together with the benefits that cannot be payrolled) must still be reported on Form P11D.

Where an employer has elected to process a particular item via the payroll for tax purposes, any benefits that are payrolled do not need to be included on Form P11D. However, other than those items subject to Class 1 NI (e.g. gift vouchers and settling of pecuniary liabilities), the taxable value still needs to be included in Form P11D(b) for Class 1A NI purposes.

Further information can be found at ‘Payrolling: tax employees’ benefits and expenses through your payroll’ (see bit.ly/38ng1gh).

Ongoing review

Whilst the above summary gives an overview of an employer’s key obligations in relation to employee benefits, it also highlights that the factors employers need to consider are getting ever more complex. As a first step, employers should ensure they have a process in place to regularly review any polices and/or positions and ensure any changes (whether legislative or change of approach by HMRC) are reflected and that they are making use of exemptions, where available. Further, employers should ensure that the employment tax treatment is considered ahead of the introduction of any new employee benefits.