The scope of the rules

Share this article

Paul Lloyds provides an overview of the 2017 reforms to US estate and gift tax and the scope of the US transfer tax regime

Key Points

What is the issue?

There have recently been major US tax reforms that include the doubling of the federal estate and gift tax exclusion amounts – specifically the thresholds at which gift or estate tax is payable on the transfer of assets.

What does it mean to me?

There is a difference in the assessment to US estate and gift tax depending on whether an individual is a US citizen/domiciliary or a non-US citizen/non-domiciliary. Non-US persons (such as a UK national) with US situated assets are unlikely to benefit from the generous exclusion amounts and therefore will often have a US estate and gift tax exposure.

What can I take away?

Non-US persons should take appropriate advice to understand their federal estate and gift tax exposure on their US situated assets. They should also be aware that additional estate or inheritance taxes may be payable at local US state level.

The US transfer tax system is composed of three taxes – gift, estate, and generation-skipping tax. Gift tax is assessed on property transferred during lifetime, whilst the estate tax is charged on property transferred at death. The generation-skipping transfer tax, or ‘GST’ tax, is a separate tax imposed on certain transfers that skip a generation (for example, gifts from grandparents to grandchildren), or are made to an unrelated donee who is more than 37.5 years younger than the donor. The GST tax is complex in its own right and is not the focus of this article.

The US has for a long time had generous transfer tax exclusion amounts, allowing the vast majority of US taxpayers to pass on their assets during lifetime or on death with little or no estate or gift tax payable. Whilst the top rate of the US federal estate and gift taxes are aligned with the top UK inheritance tax (IHT) rate – 40% – the difference in the thresholds at which the US federal transfer taxes become payable is substantial. The UK IHT exclusion amount (i.e. the Nil Rate Band) has been set at £325,000 since 6 April 2009. In comparison, prior to the recent US tax reforms (discussed below) an individual’s lifetime estate and gift tax exclusion amount was $5.49 million (inclusive of inflation adjustment).

Changes under the 2017 US tax reforms

The Tax Cuts and Jobs Act (TCJA) of 2017, which was signed into law on 22 December 2017 by President Donald Trump, enacted the first major overhaul in the US federal income tax system in over 30 years, including reform of the US transfer tax system.

The original Republican tax proposal was for a full repeal of estate tax, however the TCJA ultimately followed the Senate’s direction and instead the TCJA effectively doubles the estate and gift tax exclusion amount to $11.18 million after inflation adjustment with effect from 1 January 2018.

The TCJA reforms were passed as part of the ‘budget reconciliation’ process, meaning that they did not need a 60 vote majority in the Senate. In consequence the increased estate and gift tax exclusion amounts will only remain in effect through to 31 December 2025, at which point they will ‘sunset’ and return to the 2017 thresholds. It is also worth noting that there is a possibility of an earlier clawback – for example changes in Congress with the mid-term elections could theoretically undo the increased exclusion amount prior to the 2025 ‘sunset’.

Whilst on first glance it would appear that US transfer tax has in effect been repealed for virtually all but the wealthiest of taxpayers, UK tax practitioners dealing with clients who hold US situated assets should be aware that the generous estate and gift tax exclusion amounts do not apply to non-US citizens/non-domiciliaries, and there may also be inheritance taxes payable at local state level.

Who is liable?

US citizens

All US citizens are potentially subject to estate and gift tax on the transfer of their assets owned worldwide.

The ‘domicile’ catch

Additionally, citizens of other countries who are ‘domiciled’ in the US are also subject to the US transfer taxes on their worldwide assets. Similar to the difference between residency and domicile for UK tax purposes, for US transfer tax purposes domicile is a distinct concept from US tax residency. An individual could be a resident of the US for federal income tax purposes but not domiciled in the US for transfer tax purposes, or vice-versa.

The Treasury Regulations define the term ‘domicile’ by general description as opposed to a precise definition. However it can broadly be said that a non-US citizen (perhaps a UK national) will be considered a US domiciliary for estate and gift tax purposes by either (a) residing in the US with an intention to make it their permanent home without having a definitive present intention of leaving, or (b) by having previously resided in the US but currently live abroad with an intent to return to the US to live.

Since domicile status depends on a person’s intent to make the US their permanent home, all relevant facts and circumstances will be considered by a US court trying to determine an individual’s domicile (e.g. green card status, location of assets and principal residence, where the individual is registered to vote, where their driving license was issued, and so on).

Non-US citizens/non-US domiciliaries

Individuals who are neither US citizens nor US domiciliaries are generally only subject to US transfer taxes on certain property located or deemed located within the US at the time of the transfer. More specifically, a non-US citizen/non-US domiciliary will only be liable to gift tax on the transfer of ‘tangible’ property (e.g. real estate) situated in the US, but will be subject to estate tax on both ‘tangible’ property and certain ‘intangible’ property with a US situs (e.g. shares in US corporations) on their death.

Non-US citizens/non-US domiciliaries are hereafter referred to as ‘non-US persons’ for ease of reference.

An overview of gift tax

As indicated, although US citizens and domiciliaries are broadly subject to gift tax on the transfer of all assets owned worldwide, non-US persons are generally only subject to US federal gift tax on the gratuitous transfer of real and tangible property situated or deemed situated within the US at the time of the transfer.

The US federal estate and gift taxes share what is known as a ‘unified tax credit’, which in effect creates an exclusion amount that allows up to $11.18 million (as of 1 January 2018) of assets to be passed by US citizens and domiciliaries free of estate or gift tax. However there is no gift tax unified credit available to non-US persons (although as explained below, non-US persons are entitled to an estate tax unified credit which shelters the first $60,000 of US situs assets from estate tax on death).

A common scenario seen by UK tax practitioners is where an individual (that is a non-US person for estate and gift tax purposes) owns US real estate, perhaps a second home in Florida or an apartment in New York City. Since there is no gift tax exclusion amount for non-US persons, there would be an immediate gift tax liability at a rate up to 40% on the fair market value of the real estate if the property was transferred to their children during lifetime. See example 1.

But there are less well-known traps to be aware of. Since a non-US person is subject to US gift tax on tangible personal property physically located in the US, a gift of expensive artwork or jewellery should not be made until the item has been physically removed from the US. In addition, cash is considered to be tangible personal property for these purposes and should be transferred to a non-US bank account before it is gratuitously given to another person.

All donors, regardless of citizenship and domicile, may exempt the first $15,000 (as of 1 January 2018) of gifts made to each donee from US gift tax, as long as the transfers are gifts of a present interest. Since gifts in trust often represent gifts of future interests, transfers to trusts generally do not qualify for the annual exclusion without careful planning.

In addition, an unlimited gift tax marital deduction is generally allowed for gratuitous transfers of property to a US citizen spouse, regardless of the citizenship or domicile of the donor, as long as certain requirements are met. Lifetime gifts made to spouses who are not US citizens do not qualify for this deduction, however such gifts to non-US citizen spouses are usually eligible for a $152,000 annual exclusion (as of 1 January 2018). See example 2.

Capital gains tax on lifetime transfers

As a general rule, under US tax law a gift is not taxed as a sale or exchange and there is no charge to capital gains tax. Rather the donor’s base cost in the gifted property is generally carried over to the donee. However the donee’s base cost in the property is increased to the extent of any gift or GST taxes paid in relation to the gift, if attributable to appreciation on the gifted property.

An overview of estate tax

US citizens and domiciliaries are subject to estate tax on assets owned worldwide at death. Additionally, they may be taxed on certain property transferred during life that they retained certain rights over or interests in (e.g. certain trust interests). Lifetime gifts are not included in the individual’s taxable estate (with the exception of certain property transfers made within three years of death), however any such lifetime gifts are taken into account in determining the tax rates that apply to the individual’s estate.

Non-US persons are generally only subject to US estate tax on the value of their real, tangible, and intangible property that is situated or deemed situated in the US at the time of death. However, there are certain exemptions that exclude for example the proceeds of life insurance on the life of a non-US decedent and certain US bank deposits and debt instruments.

Gifts made during lifetime are taken into account when determining the amount of the $11.18 million exclusion that is available on the death of a US citizen or domiciliary. However non-US persons are only eligible for an exclusion amount of $60,000. To the extent that the non-US person has chargeable US situs assets in excess of the $60,000 exclusion, US federal estate will become payable. See examples 3 and 4.

An unlimited estate tax marital deduction is generally allowed for testamentary transfers of property to a US citizen spouse, regardless of the citizenship or domicile of the deceased. Bequests that are otherwise subject to US estate tax made to spouses who are non-US persons do not qualify for the unlimited marital deduction unless the bequest is made to a specifically designed testamentary trust called a qualified domestic trust, (or ‘QDOT,’) for the spouse’s benefit.

A non-US person for estate and gift tax purposes is allowed an estate deduction for a proportionate share of all debts, based on the ratio of their US estate and their worldwide estate. Care is therefore needed to ensure that a mortgage on US real estate is a ‘non-recourse’ debt, such that it is fully deductible against the US real estate and not partially allocated to non-US assets (which are otherwise not within the scope of estate tax to a non-US person).

Capital gains tax on death

There is generally no US capital gains tax charge on death. Most but not all property acquired from a decedent is stepped up or down to fair market value on the estate valuation date.

State death and inheritance taxes

Historically most US states imposed a ‘pick-up’ estate tax that was creditable against federal estate tax. However under the 2001 Tax Act, the state death tax credit was gradually phased out and replaced by a deduction for state death taxes paid. Due to the mechanics of the credit mechanism, state authorities began losing out on revenues from the ‘pick-up’ tax which has culminated in most states eliminating their transfer taxes entirely. There are currently 17 states with their own estate or inheritance tax. Delaware and New Jersey recently eliminated their estate taxes as of 1 January 2018 (although New Jersey retains an inheritance tax of up to 16% on certain family transfers).

State exclusion amounts are typically less than the federal exclusion amount. For example, Connecticut has an estate and gift tax exclusion amount of $2.6 million (although this is set to increase to the federal amount in 2020). Minnesota has an exclusion amount of $2.4 million for 2018, increasing to $3 million after 2019.

For illustration of potential cost, in an estate subject to the 40% federal estate tax, if state tax is imposed at a rate of 16%, which is the current top rate in New York state for example, the net burden of the state tax would be an additional 9.6% after factoring in the state tax deduction against the federal estate tax.

The US/UK estate and gift tax treaty

This article has only considered the US domestic law transfer tax position. However a brief mention of the US/UK estate and gift tax treaty is needed. The 1979 bilateral tax treaty between the UK and the US that covers transfer taxes (i.e. US federal estate, gift, GST, and UK IHT) broadly gives rise to the following consequences:

- Exclusive taxing rights are given to the country of the individual’s domicile, with the exception of Article 6/7 property (i.e. real estate or permanent establishment property)

- The non-domiciliary country can still subject its citizens to transfer tax according to domestic law, and

- Double taxation should not normally arise under tax credit provisions.

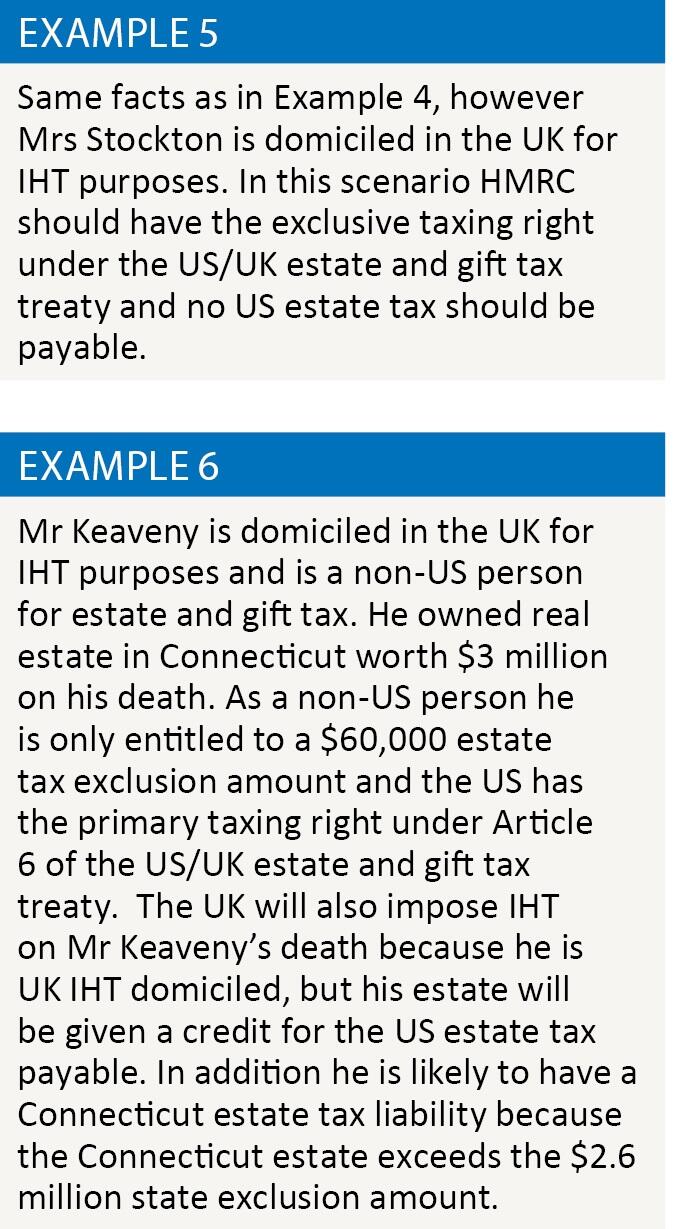

- See examples 5 and 6.

It is worth highlighting that the US/UK estate and gift tax treaty does not apply to state transfer/inheritance taxes, and unhelpfully most states do not allow foreign tax credits. This can lead to the possibility of unanticipated US state estate/inheritance taxes arising on an individual’s death.

The key message

Despite the generous US transfer tax exclusion amounts given to US citizens, non-US citizens/non-US domiciliaries should take appropriate advice to understand their US federal (and state) estate and gift tax exposures in relation to their US situated assets.

The information contained in this article is not intended to be ‘written advice concerning one or more federal tax matters’ subject to the requirements of section 10.37(a)(2) of Treasury Department Circular 230.