Tax debt collection

Share this article

Chris Holmes and Jennifer Jones set out HMRC’s powers to collect unpaid taxes from individuals and businesses

Key Points

What is the issue?

HMRC’s systems automatically recognise when tax payments have not been made on time, flagging the debt to the Debt Management and Banking Unit. The rate at which a tax debt progresses through the collection process depends on the nature of the tax and the amount owed.

What does it mean for me?

If the debt remains unpaid, HMRC may issue a Notice of Enforcement, announcing its intention to enforce recovery of the tax debt. If the notice does not result in full payment within 14 days, HMRC may commence enforcement action.

What can I take away?

Effective tax debt collection will likely be a priority for HMRC following the current crisis. Taxpayers and their advisers should be aware of HMRC’s debt collection powers and be proactive in order to manage risks and minimise unnecessary costs and disruption, seeking specialist advice as necessary.

In the June edition, we looked at the principles when dealing with HMRC’s Debt Management and Banking (DMB) Unit and some practical tips for agreeing a Time to Pay Arrangement (TTPA) with HMRC. Whilst the quantum and nature of the tax debt is significant in determining the likelihood of agreeing such an arrangement, understanding where the debt is in the collection process is also key to anticipating how much time a taxpayer may have under any agreement and what HMRC’s attitude may be. This article looks at the tax debt collection process and some of the powers available to HMRC to recover tax debts.

Overview of the collection process HMRC’s systems automatically recognise when tax payments have not been made on time, flagging the debt to DMB. The rate at which a tax debt progresses through the collection process depends on the nature of the tax and the amount owed.

Where the debtor’s contact details are unknown, HMRC can issue a notice to a third party under Finance Act 2009 Schedule 49 to obtain the debtor’s contact information. Where debtors cannot be traced, in some circumstances responsibility for PAYE and NIC debts may be transferred to other parties; e.g. a deliberate failure to pay in cases involving a managed service company, an employment intermediary or even an employee. Specialist advice should be sought if HMRC is seeking to transfer debt.

Once the debtor’s identification is confirmed, HMRC’s collection policy is generally as follows.

Statements of Account

After the payment due date elapses, HMRC will simply issue Statements of Account as a reminder of the amount due.

A request to call

After a period of time, HMRC will write to the taxpayer making specific reference to the debt and request a call to discuss it. Occasionally, for larger debts, HMRC may call the taxpayer directly and ask them if there is a reason for non-payment. It is not uncommon for TTPA discussions to take place at this stage.

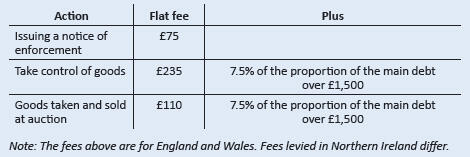

Taking control of goods

If the debt still remains unpaid, HMRC may issue a Notice of Enforcement. These notices announce HMRC’s intention to enforce recovery of the tax debt. If the notice does not result in full payment of the tax debt within 14 days, HMRC may commence enforcement action under the Tribunals, Courts and Enforcement Act (TCEA) 2007 and send its ‘field force’ officers (the bailiffs) to visit a business’s premises or a taxpayer’s home to identify, seize and eventually sell assets to settle the tax debt.

At the initial visit, the taxpayer is usually given a period of time to settle the debt or to agree a payment plan. The field force officer may walk around the premises making a note of the assets that could be sold to cover the tax debt and any associated costs of selling them, such as auctioneer fees. Those items will be written onto a ‘Controlled Goods Agreement’ (a ‘Walking Possession Agreement’ in Northern Ireland), following which the taxpayer is unable to sell or otherwise dispose of the listed assets. If the taxpayer fails to agree payment, HMRC will return and remove the listed goods.

If more funds are raised, net of fees such as auctioneers and advertising costs, upon sale of the seized assets, then the excess balance is returned to the taxpayer. However, if the funds (net of costs) are less than the debt due to HMRC, then it will pursue collection of the remaining debt.

It should be noted that additional fees will be added to the outstanding debt for enforcement action by way of taking control of goods, potentially making a visit from field force costly for the taxpayer.

HMRC increasingly uses third party bailiffs and enforcement agencies to facilitate the collection of the tax debt. The collection agencies are used simply because when a taxpayer is contacted by someone outside HMRC, it often prompts payment or agreement of a payment plan. (In Scotland, such recovery action can only be carried out under court direction by Sherriff Court officers.) If the total debt is not settled through taking control of goods, HMRC will escalate the matter and attempt to collect the debt through DMB or HMRC Late Stage Resolution Department. At this stage, communications with the taxpayer will include the threat of legal action in respect of the debt.

Bankruptcy/insolvency

This is ultimately the final sanction for HMRC. Petitioning to bankrupt individuals and to wind up companies is carried out by the DMB’s Enforcement and Insolvency Office (EIO).

It is important to understand that the EIO does not act like most commercial creditors. It will seek to make a taxpayer bankrupt even where it is clear that it will receive nothing. Such action is permitted even where an assessment is under appeal and awaiting a tax tribunal hearing, where collection of tax is not postponed.

For individuals, the EIO will first serve a Statutory Demand (requesting payment within 21 days) before petitioning the court. The court will then issue a hearing date for the judge to consider making a bankruptcy order. For companies, HMRC will use the compulsory liquidation procedure, by issuing a winding up petition to the court.

Once a petition has been issued, the timetable is very much governed by the court. In the case of a company, the winding up petition will be advertised, bringing it to the attention of creditors and others (including bankers, who are likely to freeze bank accounts) unless the company obtains a court order preventing the advertisement. Even if the company can settle the debt before the date of the hearing, the reputational damage associated with such proceedings can be detrimental to the business.

It should be noted that the taxpayer can seek a TTPA with HMRC at any stage in the collection process. However, the further a tax debt is along the collection process, the less favourable any agreeable TTPA terms will be. For example, HMRC may agree a TTPA covering 12 months for a tax debt at the initial stages of the collection process but only agree to a couple of months if that same tax debt were in the latter stages of the collection process.

HMRC powers in relation to tax debts

Further to progressing the tax debt through the general collection process, HMRC has a range of powers at its disposal to recover tax debts.

Tax collection via coding notices

HMRC can alter individuals’ coding notices to collect self-assessment tax, Class 2 National Insurance debts, contract settlement debts and tax credit overpayments by deduction at source from their salary or pension.

The amount that can be collected this way varies depending on the taxpayers earnings. If a person earns less than £30,000 per annum, then HMRC can collect up to £3,000 via their tax code. If a person earns more than this, HMRC can collect more – up to £17,000 if the person earns £90,000 or more. However, the limit for collecting self-assessment balancing payments and PAYE debts remains £3,000. If the amount owed exceeds these limits, HMRC will not collect the debt via the individual’s coding notice but will use other methods instead.

Direct recovery of tax debts

Finance (No 2) Act 2015 s 51 and Schedule 8 enables HMRC to collect tax and duties due to it directly from taxpayers’ bank and building society accounts. This is known as the ‘direct recovery of debts’ (DRD) and targets those taxpayers who have the means to pay but choose not to do so.

Whilst the use of these provisions has been limited to date, a review of the DRD intervention published by HMRC in April 2019 concluded that the provisions have a significant deterrent effect. Of the 22,667 cases subjected to the DRD provisions between March 2016 and December 2018, payment was recovered early in the DRD process with only 19 cases requiring actual deduction from the taxpayers’ bank accounts.

Direct recovery can only be considered for debts of £1,000 or more and a number of safeguards are in place under these provisions, including the following:

a) Every debtor must receive a face to face visit from HMRC agents before their debts are considered for recovery under the DRD.

b) When determining the amount of funds available to settle the taxpayer’s debt, an amount of at least £5,000 must be left in the debtors account(s) with the bank/building society in most cases.

c) Debtors affected by DRD will have 30 days to object before any money is transferred to HMRC.

d) HMRC will not use its DRD powers to recover amounts owed by vulnerable taxpayers. Further guidance on how HMRC identifies ‘vulnerable taxpayers’ can be found at bit.ly/37aGzNa.

After the face to face visit, taxpayers who are not vulnerable and have sufficient money in the bank but still refuse to settle their debts can be considered for debt recovery. They have up to 30 days to object, although their bank accounts will be frozen during that period which may cause significant issues, particularly for businesses.

If the DRD provisions are applied by HMRC, it is important to check that any notices issued are correctly issued and valid. Objections can be made to HMRC, although the grounds of appeal are limited. If HMRC rejects an account holder’s objections, then the account holder may appeal to the County Court.

Notice of requirement to give security for tax debts

With the aim of limiting its exposure to potential future bad tax debts, HMRC may issue a notice of requirement to give security to companies and their directors, or to LLPs and their partners, if:

a) they failed to comply with their tax obligations in their previous or current business; or

b) HMRC has spotted that the directors were connected or associated with multiple business failures.

Security can be demanded for debts of PAYE, NIC, Construction Industry Scheme, corporation tax, VAT, insurance premium tax, aggregates levy, climate change levy and landfill tax. The notice requires the company and its directors, or the LLP and its partners, to give security in respect of tax within 30 days (or a longer period if HMRC permits). The company and its directors are therefore jointly and severally liable to give the full amount of security.

HMRC will not accept assets as security. The security can only be provided by cheque or bank transfer, opening a joint bank account with HMRC or providing a guarantee in the form of a performance bond from an approved financial institution.

If the taxpayer disagrees with anything in the notice, then they must appeal to HMRC within 30 days of the date of the notice. If no agreement is reached, the matter may be referred for internal review or a hearing before the First-tier Tribunal. Furthermore, if the company knows that it needs a TTPA for any tax debts or the security amount, then they must contact HMRC to request one before the date that the security becomes due. The security is normally held for 24 months but if the company or LLP meets its normal tax obligations (including payments), the holding period may be reduced. When it is no longer required, the security is either repaid or set against outstanding tax debts.

It must be noted that failure to give security is a criminal offence and HMRC may prosecute the company and directors, or the LLP and partners, and convicted parties will be fined up to £5,000. In addition, the taxpayer may be entered into the Managing Serious Defaulters regime as a result of being asked to provide security.

Further information about the requirement to give security can be found in HMRC’s Security Guidance Manual and in its series of factsheets (SS/FS1, SS/FS2a, SS/FS2b and SS/FS3–SS/FS6), and at bit.ly/2CdeSbf and bit.ly/3ixEQqB.

Accelerated payment notices for scheme users

Where the ‘debt’ arises from tax in dispute because of a tax avoidance scheme, HMRC may issue an accelerated payment notice (APN) to the taxpayer under FA 2014 ss 219-229.

An APN effectively prevents postponement of tax while an enquiry or appeal is ongoing. The payment must be made within 90 days of the APN or 30 days after HMRC issues a determination in response to any representations made following the notice’s issue. However, a TTPA can be agreed with HMRC in respect of the amount due.

If the taxpayer instead decides to withdraw from participating in the scheme and settle the outstanding tax, then it may be possible to do this by way of a contract settlement following discussions with the HMRC officer. HMRC is often prepared to include in the contract settlement instalment payments which may be over a period in excess of 12 months. A better result may be achieved in terms of time to pay upon settlement than via a TTPA negotiated with DMB in respect of the APN. However, having settled their tax position with HMRC in relation to the scheme, the taxpayer will not benefit if the scheme is ultimately found to achieve its original aims.

Court action

For tax debts of less than £2,000, HMRC may seek ‘summary proceedings’ from the Magistrates’ Court (TMA 1970 s 65 and DMBM660040). For larger tax debts, HMRC may refer the case for recovery to other courts such as the County Courts or High Court (TMA 1970 ss 66 and 68). In practice, a County Court judgment (CCJ) does not give HMRC any powers of collection that it does not already have.

Therefore, a CCJ is generally only sought where its threat is believed likely to elicit settlement of the debt by the taxpayer – on the basis that the CCJ would seriously impact a person’s access to credit, and could adversely impact their professional status.

Effective tax debt collection will likely be a priority for HMRC following the current crisis. HMRC’s powers will be expanded following Royal Assent of the current Finance Bill as that prioritises certain tax debts on insolvency, as well as making directors and LLP members jointly and severally liable for tax debts in situations involving tax avoidance, evasion or phoenixism. Taxpayers and their advisers should be aware of HMRC debt collection powers and be proactive in order to manage risks and minimise unnecessary costs and disruption, seeking specialist advice as necessary.