The uncertainty of taxes on death

Share this article

The OTS first review of inheritance tax highlights the need to improve the taxpayer experience. Paul Morton provides an overview

Key Points

What is the issue?

The OTS has published the first of two reports on inheritance tax. There is a huge opportunity to reduce the ‘form-filling’ that particularly burdens people at what can be a very difficult time. Other areas of IHT will be covered in a second report in the spring.

What does it mean to me?

There is still an opportunity to send in thoughts on other aspects of inheritance tax as the OTS completes the review over the next few months. Many people worry about IHT even though there might be no liability on death and the OTS will continue to examine how the tax can be better explained and communicated.

What can I take away?

IHT is arguably the tax about which people react most strongly. Although HMRC are doing very good work to improve the taxpayer experience there is more to be done to avoid people worrying unduly about the tax.

There is something about inheritance tax (IHT) which makes it particularly unpopular. Is it because many people worry about the ‘form-filling’ which usually comes at a particularly difficult time? Or is it because people worry about the future impact of IHT on their plans to support their children or wider family? Or could it be because of the way the tax is perceived, as a voluntary tax, paid by those with mid-sized estates, with many traps for the un-advised or unwary?

The OTS received more than 3,000 responses to its on-line survey, 500 emails and 100 formal responses to the call for evidence. The review was featured on the front page of several national newspapers, on the BBC’s Money Box and an FT Podcast and it received wide coverage elsewhere. Taken as a whole, this represented more interest than perhaps all previous OTS reviews combined! Clearly, people have views on IHT.

The OTS strategy is to undertake work which will benefit the largest number of people on the greatest number of occasions and to focus on the ‘user experience’ of those interacting with the tax system. It has been felt for some time that IHT was therefore a very suitable tax for an OTS review and there is also an aspiration to have touched most parts of the tax system, although those advocating a review of the treatment of hybrid instruments, for example, may have to wait a little longer!

Not surprisingly, it quickly became apparent that IHT is a large topic so rather than holding all of the observations and recommendations to the end, it was decided to report in two parts, the first concentrating on the experience of taxpayers in completing the forms and interacting with HMRC and the second looking more broadly at the design of the tax.

It is important to note that the role of the OTS is to make recommendations to the Chancellor on ways of simplifying the tax system including the ‘user experience’ but not to propose policy changes beyond the simplification remit. On this occasion, this presented something of a challenge for the OTS. Among the more than 3,500 responses, and hundreds of comments under the online newspaper articles, were a huge number of observations, comments and suggestions about the design of the tax, ranging from arguments that it should be abolished, with contrary arguments that it should be charged at 100%, to sweeping suggestions of gift taxes, greatly expanding the scope of capital gains tax and other dramatic reforms. The OTS received a few hand-written letters, for example from elderly sisters who had lived together all of their lives and were concerned that the family home might have to be sold when the first sister died. A wide range of such observations have been included in the report reflecting the OTS’s broader objective of encouraging wider debate and discussion. The second report will return to these areas, at least to the extent they are within the scope of the OTS work on simplification.

The online survey indicated that even among the relatively well-informed readership of the FT, the Times and Telegraph, there was a range of levels of knowledge about IHT. The general features of IHT are quite well known including the 40% rate and the main allowances and reliefs but people quickly become lost in the detail. Some people worry about IHT when, in practice, perhaps they need not. The survey indicated that 26% of respondents thought that 20% or more of estates resulted in a cash tax payment whereas the proportion is actually closer to 5%. The report therefore sets out some basic facts to inform the debate.

Every year around 570,000 people die in the UK. IHT forms are completed for about half of their estates, 275,000 in 2015/2016, although IHT is only paid in respect of 25,000 estates, less than 10% of those for which forms are completed. IHT is thought of as an important tax but actually brings in between 1% and ½% of total revenue, about £5.2 billion in 2017/2018. The tax gap is relatively high at around £600 million.

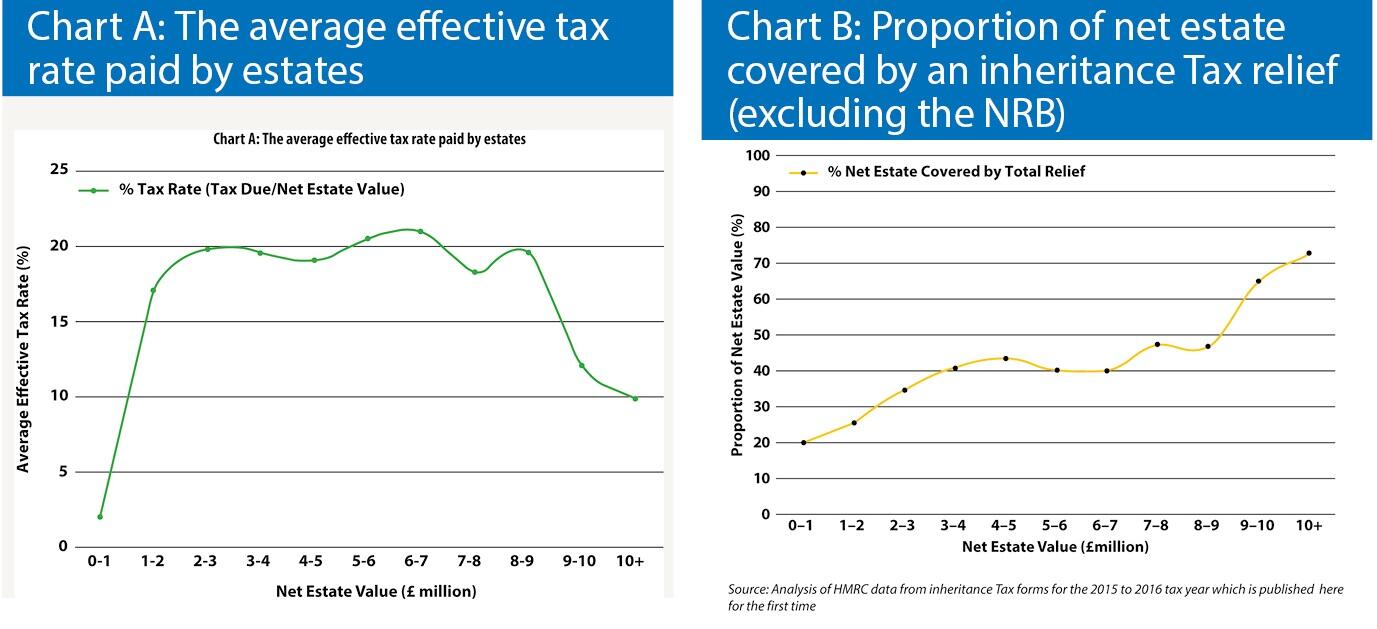

A particularly striking feature is that the average effective rate of tax paid by estates climbs quickly to around 20%, after reliefs, for estates up to £1-2 million and then falls away for estates above £8-9 million to around 10% or lower.

The reason, as shown in the second chart, is that as estates grow in size more of the assets tend to be within the scope of one of the reliefs, particularly business property relief, agricultural property relief or gifts to charity. Although not reflected in the charts, it is also the case that those with more substantial wealth are more able to make lifetime gifts without impairing their financial wellbeing. While HMRC have good quality data on estates on death there is less data available in relation to life-time gifts as they do not need to be reported in all cases.

Turning, in more detail, to some of the concerns people have expressed about IHT, the nil rate band is quite well understood but the residence nil rate band is generally thought to be very complex. Those who do not have children or do not own a home argue that the scope is too narrow. The rules regarding relief for gifts were felt to be confusing and not to have kept pace with inflation. An amount which would have provided for a good wedding when the Capital Transfer Tax Act 1984 was given Royal Assent, £5,000 from a parent, £2,500 from a grand-parent and £1,000 from most others, would hardly provide for an opulent celebration in 2018 - the average wedding now costs around £30,000 according to Brides magazine. Business and Agricultural Property reliefs seem to be working relatively well although some areas, such as furnished lettings and partnerships can be problematic. Other areas, which will be considered in the second report, include the practical operation of the reduced rate which applies where a certain proportion of the estate is left to charity, the treatment of life assurance products and pensions, trusts and gifts with reservation and pre-owned assets.

It was particularly interesting, through the survey and the comments in the press and engagement with a wider audience than is usual for an OTS review, to see some of the broader concerns in the public mind. The rate is seen as relatively high and it is indeed the joint fourth highest headline rate in the OECD. However (thanks in part to the spouse exemption) the average effective rate is around 20% and this is much more in line with international norms. Some people feel that the imposition of IHT means that people are paying tax twice because wealth generated over a lifetime will generally be derived from income which has already been taxed. One might even argue that it would be taxed a third time when spent, albeit on a different person. There is a concern that wealthy people do not pay IHT because they can avoid it through careful planning, for example by placing their assets in trusts to avoid tax, although in reality this is not the case as trusts are subject to their own IHT regime.

The results of the online survey pointed to the need for action in several areas. 38% of respondents who did not use an adviser recalled spending 50 hours or more on administration of the estate. This would include an application for probate, for example, and the general administration involved following a death but nevertheless is a very substantial commitment of time. People indicated that they spent a great deal of time understanding and completing IHT forms. Among those who did not appoint an adviser, some 65% of respondents suggested that despite there being no IHT liability they still had to provide a significant amount of information. Only 11% of these individuals stated that they found the process simple and user friendly. 61% of respondents stated that they did not know how long it would take HMRC to respond once they had submitted their form.

The OTS benefits in all of its work from deep and very positive engagement with HMRC and HM Treasury. HMRC has improved the experience enormously over the last few years and the forms are all available online and great efforts have been made to set out the instructions and guidance as clearly as possible. HMRC is currently undertaking some outstanding and ground-breaking work on the customer experience applying deep expertise in behavioural science. The gap between the results of the efforts so far and the actual taxpayer experience shows what a long journey this will be but also how worthwhile. The OTS has argued that even greater priority should be given to this good work and to bringing IHT fully into the digital era.

The recommendations in the first report all concern the administration of IHT. In particular, the key recommendation is that the government should implement a fully integrated digital system for inheritance tax ideally including the facility to complete and submit an application for probate. The OTS recognises that there are other priorities at present for the HMRC technology budget including Making Tax Digital and a new customs system for the UK so in the meantime the OTS suggests that HMRC should continue its good work on reducing and simplifying the current forms and look in particular at shortening the form for the simplest estates and removing the requirement for a form at all where that is possible.

A consistent theme in all OTS reviews is that HMRC should continue to improve the guidance and target efforts at reducing concern for those who worry unnecessarily. The guidance should be clear and easy to navigate and linked with guidance on probate application and related areas. It should include worked examples, a road map and a tax calculator. HMRC should issue automated receipts as too many people are currently left in limbo for too long.

There is plenty here which can make a meaningful difference to the experience of perhaps more than a quarter of a million people each year. The second report will touch on other, even more difficult, areas but has the potential to relieve the anxiety of an even greater number of people who worry about IHT during their lifetimes.