Key Budget decisions: what they will mean in practice.

Share this article

We ask what impact the Budget decision will mean for UK taxpayers in practice and how they may impact our behavioural responses.

Writing about the Spring Budget isn’t easy, not least because we have already heard from economists, politicians and commentators on the main Budget decisions.

It seems clear that parts of the Budget were put together at the last minute; there wasn’t enough time to produce a paper on the abolition of the furnished holiday letting regime from April 2025. The paper on the major changes to the non-domiciled rules, also from April 2025, is a high level document, with the promise of much more to come on the detail. Fortunately, there was sufficient time for the Office for Budget Responsibility to estimate the revenues and costs from the measures and add their uncertainty rating.

We all know the backdrop to this and preceding Budgets. Overall, taxes continue to rise, to pay for the £370 billion of Covid support and the reduced tax yield at the height of the pandemic. For most individuals, the rising tax burden does not affect cash income tax; rather, there is an increased tax take on growing incomes, as allowances and rate thresholds are not increased for inflation.

The big giveaway

The big giveaway in the Budget was a further 2% cut in the main national insurance rate, costing over £10 billion. This goes both to employed and self‑employed individuals, so the new rates become 8% for employees and 6% for self-employed people (the 2% rate above £50,270 is unchanged). About 27 million people benefit from the cut, with the largest cut (£754) going to those with earnings of £50,270 or more. The Office for Budget Responsibility estimates that it will reduce tax motivated incorporations by a cumulative 83,000 by 2028-29.

The Chancellor also floated the idea that individual national insurance might be abolished. However, the cost is currently about £46 billion (compared to total tax for 2024-25 of just over £1 trillion), so it is clear that national insurance will be with us for many more years. Employers’ national insurance remains unchanged and would surely stay even if individual national insurance were to disappear.

Naturally, some have pointed out that 12.5 million pensioners do not benefit from national insurance cuts, but they have had the benefit of a 19% increase in the main state pensions over the last two years – more than the average pay rise for employees.

High income child benefit charge

The major change to the high income child benefit charge will benefit up to 485,000 households, with 170,000 people no longer liable to pay the charge. From April 2024, the lower threshold rises to £60,000 and the higher threshold will be £80,000. This reduces the taper for one, two and three children to 48.7%, 53% or 57.5% respectively, compared to 53%, 61% and 68% currently.

Complexity arises because many people will now find it worthwhile to claim child benefit, although HMRC has successfully embedded claims in the new version of the personal tax account and the HMRC app. The data from 2020-21 (unhelpfully the latest published) showed that 355,000 people paid high income child benefit charge in that year and 683,000 households opted out of receiving child benefit, raising about £1.5 billion for the exchequer.

There must be a suspicion that these figures are understated, as they do not include those who did not register for child benefit, or those who did not report liability. There will be a consultation on moving the charge to household income, which would bring additional complexity and challenge independent taxation, whilst appearing superficially fairer.

Property and lettings

The furnished holiday lettings regime was discussed by the Office of Tax Simplification in its 2022 Review of residential property income (see tinyurl.com/2dxnp7rf). About 127,000 furnished holiday lets were declared in 2019-20, with 17,000 in Europe (out of 2.9 million properties). The use of the regime varies; many owners make personal use of the property, while others operate substantial complexes or holiday villages.

The regime was originally introduced in 1982-83 to provide clarity over whether operating a short-term holiday rental business should be treated as a trade for tax purposes, following a number of cases.

The Office of Tax Simplification recommended that if the government did abolish the holiday letting rules, it should introduce a ‘brightline’ test for a holiday letting trade, with similar advantages to the current regime. Without this, there would no doubt be a return to uncertainty for those operating substantial businesses. It is to be hoped that this will be considered, together with some easements for those moving out of the capital allowance regime to the renewals basis.

The government has already acted to prevent owners from benefiting from business asset disposal relief on selling properties from 6 March. They will, however, benefit from the cut in the capital gains tax rate to 24% on sales of residential property from April 2024.

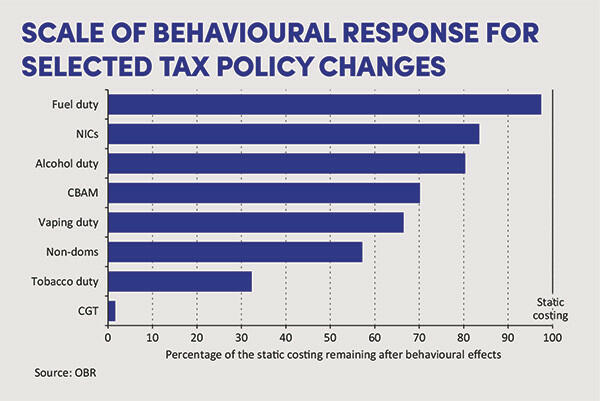

Behavioural responses

One of the useful explanations from the Office for Budget Responsibility covers uncertainty and behavioural responses (see tinyurl.com/3xm6py32).

Obviously, there is a tiny number who bought fuel just before the Budget, in case fuel duty rose; most of us didn’t bother. Conversely, reducing the capital gains tax rate on residential property means that virtually no one will conclude a sale in March – whilst many are thought to accelerate sales into the following two years, with more actually paid in stamp duty land tax (and equivalents) than capital gains tax.

The major changes to the non-dom rules are covered by Anthony Whatling (see page 11). It is just worth adding that the Office for Budget Responsibility’s costings estimate that between 10% and 20% of current non-domiciled individuals will leave; it has not modelled the impact of people potentially not coming to the UK. Its estimated tax yield in the short term comes from just 5,500 individuals, ineligible for the new regime.

The UK’s carbon border adjustment mechanism – a levy payable when the carbon price in the country of origin is lower than the carbon price paid by UK producers – is thought to raise £200 million in 2028-29, which comes almost entirely from iron and steel imports from China, as well as aluminium. The Office for Budget Responsibility estimates that the EU carbon price will remain above the UK price – otherwise a much larger amount would be raised.

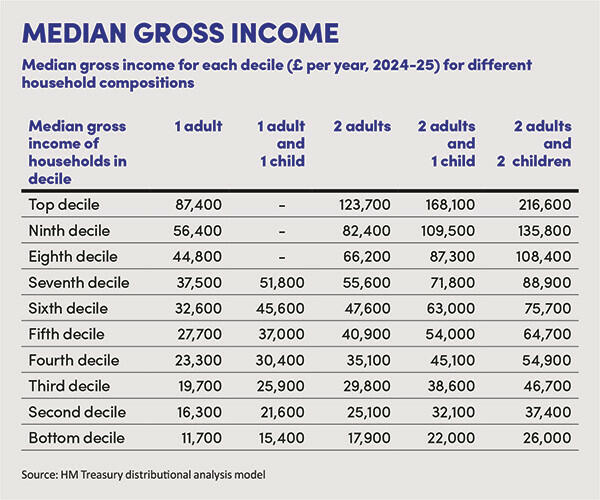

Just as for previous years, the government estimates that the majority of households (over 60%) receive more in welfare income and benefits in kind than they pay in tax. There were 28.2 million households in 2022; some 8 million (30% of households, but only 13% of the total number of people) live alone (see tinyurl.com/2uuuvchz). The median income before tax for households is interesting (see tinyurl.com/2479f7th); the much higher income for two adults with two children compared to two adults without children is presumably not because the children go out to work!

In conclusion

Finally, tax professionals will need to consider the government’s proposals for new regulation. The consultative document initially covers those acting as tax agents, rather than the much wider category of tax advisers. A choice is put forward between mandatory membership of a recognised professional body; joint regulation with HMRC; and regulation by a new government body.

Regulation by HMRC alongside professional bodies is the least desirable model, in my view – so the choice should be between an enhanced role for professional bodies, with no doubt increased inspection of members, or handing over regulation to a new body, as happens with solicitors.

Whichever route is chosen is likely to mean much higher costs for tax agents and advisers. Software developers have been left out, as well as those already regulated, such as solicitors and barristers. It is surely doubtful whether an enhanced role in the UK tax system for third-party software is compatible with a lack of regulation.

The second Finance Bill of the year has already been published, with few of the important changes included. Tax Administration and Maintenance day comes on 18 April, with the promise of more tax documents to mull over. Time will tell whether we have further fiscal events in 2024.