Thresholds in the tax system: the challenges for future tax policy

Share this article

We consider the difficulties that the main tax threshold rules cause to individuals and small businesses, and how future tax policy can address these challenges.

Thresholds are an integral part of the tax system. They apply to exempt some taxpayers from a charge; define when tax is levied, or a higher rate applies; or define when an allowance or other benefit is withdrawn. Thresholds can define administrative savings (those with income, gains or sales below a threshold may not need to register and comply with a tax or may be able to file in a simpler way). Yet thresholds also present challenges for taxpayers. Going over a threshold may result in very high tax costs, as well as administrative costs and burdens.

The Tax Law Review Committee has recently published a discussion paper ‘Thresholds in the tax system: policy and administrative considerations’, authored by Sally Campbell, Bill Dodwell and Patricia Mock (tinyurl.com/5x9xfces). It discusses the difficulties in the main tax threshold rules as they affect individuals and small businesses, and considers a range of principles which might assist in the design of tax policy in the future. The paper focuses on the additional thresholds layered onto the basic system, such as the tapering of the personal allowance for incomes of over £100,000.

There is a distinction between a threshold where a higher tax rate applies if the threshold is exceeded, and one where exceeding the threshold means that the taxpayer is worse off overall:

- The tapering of the personal allowance for incomes of over £100,000, where a higher marginal tax rate applies across a band of income, is an example of an unexpected higher effective rate.

- The removal of tax free childcare, the threshold for which is also £100,000, is an example of where going over that £100,000 threshold makes the individual materially worse off. Put another way, the marginal tax rate on a band of income is over 100%.

Economists refer to the former as kinks and the latter as notches.

The discussion paper has seven general recommendations (see General recommendations) and specific recommendations on childcare costs, VAT, savings and pensions.

General recommendations

Policymakers should take particular care to minimise (and ideally avoid completely) the occasions when exceeding a threshold makes a taxpayer noticeably worse off; i.e. the tax liability is greater than the additional income.

- Policymakers should take care when setting taper rates not to create significant barriers to taxpayers increasing their income. In general, a lower taper rate is preferable, even though this will increase the numbers of taxpayers subject to the taper and receiving a benefit whilst also increasing the exchequer cost.

- Research should be undertaken or commissioned by HMRC to understand better the impact of thresholds and higher marginal rates on different types of individual decisions. This could support better decisions on the rate and length of tapers, which at present appear arbitrary.

- Policymakers should consider whether multiple events could occur at broadly similar income levels and ideally avoid the potential for multiple charges.

- Policymakers should review thresholds and exemptions periodically to assess whether they continue to meet the policy intent. A standard review period of, say, five years should be established, and the result of the review announced. Where after a review policymakers decide not to increase a threshold or exemption (thus making more people liable to a charge, due to the impact of inflation), policymakers should indicate the additional numbers affected and the exchequer impact – just as is done when a new policy is introduced.

- Policymakers should consider the impacts of future inflation when designing new thresholds or allowances. Compromises in design that might be accepted when few taxpayers are affected may not remain acceptable when applied to many more taxpayers.

- Policymakers should keep administrative thresholds under review, in the same way as substantive thresholds. Whilst minimising administrative burdens is in principle desirable, there are cases where administrative thresholds have been set too high, such that insufficient information is provided routinely, when it may be done more cheaply and conveniently. This can introduce additional costs due to compliance checks or the lack of a suitable alternative reporting mechanism.

The VAT registration threshold

There are a number of well-known problematic thresholds in the UK tax system. The VAT threshold acts as a barrier to growth, as evidenced by the Office of Tax Simplification in 2017 and, more recently, by the Office for Budget Responsibility.

Too many businesses have sales just below the £85,000 limit, as their owners know that increasing sales will reduce their profits and bring additional administrative burdens. The number just below the registration threshold has increased every year, no doubt due to inflation; the Office for Budget Responsibility predicts that it will reach 44,000 in two years. Introducing an allowance, or rebate, for businesses which go over the threshold could help to promote economic growth.

Evidence from Finland shows that work is also needed on VAT administration; perhaps this could in part be eased when Making Tax Digital for Income Tax has been introduced, such that most businesses keep digital records. The variability of the VAT base is unlikely to change, though. Despite academic encouragement, the public (and thus politicians) seem keener on yet more VAT exemptions.

Child benefit and childcare thresholds

The high income child benefit charge brings a high and variable tax rate on income between £50,000 and £60,000. A parent with one child faces a marginal income tax and national insurance rate of 54% in this band, which rises to 63% where there are two children; the rate for three children is 71%. If the parent is also liable for student loan repayments, an extra 9% boosts the effective rate to 63%, 72% and 80%. The charge does raise some £3 billion to £4 billion annually, though, so it is understandable that the government has chosen to retain it for over a decade.

Having a variable taper rate which increases with the number of children does not help individuals to understand how they are affected by earnings over £50,000. A very high taper rate is more likely to discourage some individuals from working. However, we do not have any useful data on the actual impact. Do some people reduce their work, or do they simply accept a low return on income in the £50,000 to £60,000 band as part of building a career? How well do individuals understand the position? Anecdotes are naturally about individuals reducing their work and may not be helpful in understanding the full picture.

The paper recommends that a standard taper be used, both to get away from very high taper rates but also to be much clearer to affected parents. This would initially cost the exchequer tax money but could potentially boost the economy (and thus tax receipts) through more parents working.

An even more challenging threshold applies in respect of publicly funded nursery places, as well as tax-free childcare. Analysis by the Institute for Fiscal Studies (tinyurl.com/5t4mvjck), which includes the effect of income tax and national insurance, as well as the withdrawal of tax-free childcare and funded childcare hours, finds that:

‘A parent with two children under three whose childcare provider charges England’s average hourly rate for 40 hours per week would, after these reforms, find that their disposable income (i.e. earnings net of tax and childcare outgoings) falls by £14,500 if their pre-tax pay crosses £100,000. Disposable income would not recover its previous level until pre-tax pay reached £134,500, meaning a parent earning £130,000 would be worse off than one earning £99,000.’

There is no easy answer to this threshold, other than to consider making publicly funded nursery places a universal benefit. It would be administratively impossible to introduce a tax charge based on the value of nursery places; there is no mechanism to provide that data to HMRC (unlike child benefit where HMRC does at least know how much has been paid, since it is paid by HMRC). It would help to understand the scale of the issue if data were available on the numbers of affected parents.

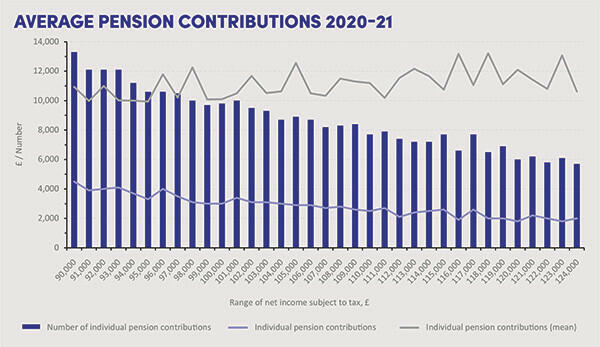

Pension contributions

One of the suggestions routinely put forward by tax advisers is for an individual affected by these charges to consider making pension contributions, as a relatively small outlay at these marginal rates.

Yet the evidence to date suggests that few people are taking that advice. Data provided by HMRC under a Freedom of Information request shows no significant increase in pension contributions by those with income just below £100,000. See Average pension contributions 2020-21.

Savings income

The savings allowance for basic and higher rate taxpayers was introduced in 2016, when interest rates were low. It saved significant administration, since banks and building societies no longer needed to deduct tax from interest payments. Savers benefited by up to £200 annually. HMRC estimates that in 2022-23, 12 million individuals benefited from the personal savings allowance, at a cost of £590 million. However, interest rates have risen, such that HMRC estimated in July 2023 that there would be an additional 1 million taxpayers liable to income tax on their savings in 2023-24 – a total of 2.7 million.

The design of the allowance is sub-optimal; it is in reality a zero rate but is expressed as an allowance. Some individuals with total income slightly above the higher rate threshold can face a very high marginal rate on their interest income, as the notional allowance is reduced to £500.

The starting (nil) rate on savings income up to £5,000 seems a completely untargeted relief. HMRC statistics show that in 2020-21, 635,000 taxpayers (out of 31.7 million) benefited from the savings rate. 538,000 of them had income from property and savings; there were 78,000 employees; 3,000 self-employed individuals; and 16,000 pensioners (out of about 7 million tax paying pensioners). Nowhere else is there a relief mainly benefiting those who are neither pensioners nor working. The paper recommends that the starting rate be abolished.

Pensions

The fundamentals of our current system for taxing pensions were introduced in 2006, with the aim of having a single tax regime for all pensions. It has not lasted well. The initial offering of a very high annual limit on contributions (£225,000, rising to £250,000) simply meant that very high earners (whose contributions had been limited under previous regimes) saved huge amounts of tax.

The lifetime allowance started at £1.5 million and rose to £1.8 million. The subsequent picture was then one of significantly reduced annual and lifetime allowances, as chancellors tried to keep the annual costs of pensions under control. This has resulted in much greater complexity for higher earners.

Those in defined benefit schemes started to be hit by unknowable tax charges and those in defined contribution schemes started to cap their contributions (risking a lower pension fund) lest investment growth exposed them to an excessive 55% tax charge.

At the same time, there has always been an anomaly on death benefits, made much more obvious by the 2015 pension freedoms, which removed the requirement to buy an annuity. Where the pension holder died under 75, beneficiaries can inherit the fund (up to the lifetime limit) without a tax charge. This cannot be justified. About 30% of men and 18% of women die below 75. The 2023 and 2024 reforms certainly help higher earners by introducing much higher annual allowances, whilst still preventing those earning more than £360,000 from being able to participate (with a tapered reduction from £260,000).

Abolishing the lifetime allowance has still preserved the death benefit anomaly, subject to a new limit equivalent to the former lifetime allowance. A cap on the tax-free lump sum has been introduced for those with various forms of protection when the lifetime limit was cut. The complexity of the annual allowance for defined benefit schemes remains, albeit affecting fewer people.

At the same time, lower-paid individuals do not have sufficient pension savings, despite the very successful introduction of automatic enrolment.

The paper recommends that a broad review of pension tax relief is needed to end up with a system that is easier to understand and to administer. The Labour party has said that if elected to government it would reintroduce the lifetime allowance. Let us hope that any reintroduction takes place as part of a wider review.

Administration

There are a whole range of administrative thresholds, which typically exempt taxpayers from needing to supply information to HMRC or filing a return. These limits need to be kept under review, just as for substantive limits.

However, care needs to be taken not to set filing thresholds too high, as this could be counter-productive, in that HMRC might need to find less convenient ways to obtain information. A particular example is the planned removal of the requirement for individuals with PAYE income of any level to file Self Assessment income tax returns. This is not thought to be a very large number – probably less than 500,000 people in the context of 12.5 million currently filing Self Assessment returns. Many of those affected will still need to provide information to HMRC or make claims. The tax return system is well-known; finding different ways to exchange information with HMRC could well be less convenient and more prone to error.

In conclusion

Designing effective thresholds in the tax system will never be easy; there will always be trade-offs between exchequer costs, complexity and work incentives. The authors and the Tax Law Review Committee hope that these general principles will help future policymakers.