Group financing arrangements: tackling hybrid mismatches

Share this article

Two recent cases show why the UK and the BEPS Inclusive Framework are tackling hybrid mismatch arrangements.

One of the key targets of the G20 led Base Erosion and Profit Shifting project was multinational groups that exploited domestic rules on financing arrangements. The basic idea was to lend money within an international group in such a way that either two tax deductions were generated in different countries, or that a single deduction was claimed without there being equivalently taxed income in another country. In theory, the arrangements satisfied the domestic requirements in the different countries involved; the ‘magic’ happened because of different approaches to classification of income or entities.

The BEPS project (see tinyurl.com/5n7jvf7a) included two actions specifically relevant to debt financing:

- Action 2: Neutralising the effects of hybrid mismatch arrangements; and

- Action 4: Limiting base erosion involving interest deductions and other financial payments.

Financing was also covered in Actions 8-10, on transfer pricing.

The UK was one of the first countries to adopt these measures, from 2017. Interest restrictions were thought in 2016 to bring in about £1 billion annually, with a further £200 million from the anti-hybrid rules – both figures are based on a 19% corporation tax rate.

Two recent cases illustrate why the UK – and the BEPS Inclusive Framework – have taken action against hybrid entities and hybrid instruments.

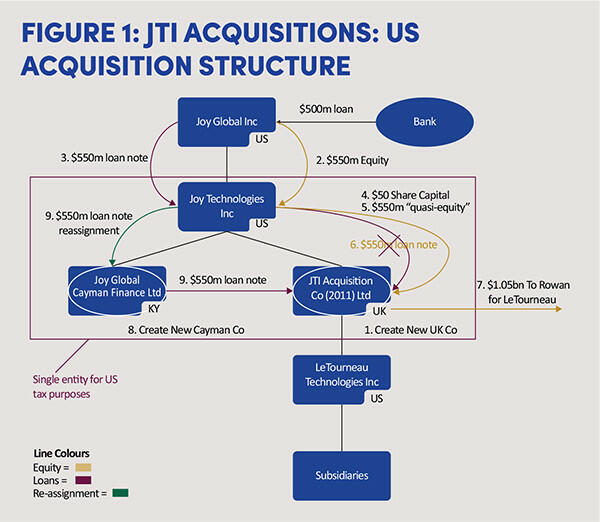

JTI Acquisitions

The Upper Tribunal has just dismissed an appeal by JTI Acquisitions (2011) Ltd v HMRC [2023] UKUT 194 in respect of a US acquisition financing structure. The decision attached the structure (see Figure 1: JTI Acquisitions: US acquisition structure).

The judgment noted: ‘In 2011, Joy Global acquired another US-headed equipment group for $1.1 billion using the appellant, a newly incorporated [UK] company, as the acquisition vehicle. The acquisition was part funded by an intra-group $550 million borrowing by the appellant on which it paid arm’s length interest.’

The key part of the structure is the purple box – three companies in the US, Grand Cayman and the UK, which were effectively treated as a single entity for US tax purposes. This meant that there was no net income for US tax purposes, as the finance costs in the UK appellant company equalled the finance income in the US lender. This is an example of a one-sided deduction, which could only work thanks to the US entity classification rules.

The intended aim was that the UK acquisition company would receive a UK tax deduction for loan interest, which it would surrender as group relief to other UK companies in the group. Since the UK company was buying a US trading group, there would be no taxable income on any dividends, and it is likely that any future sale of the US sub-group would qualify for the substantial shareholdings’ exemption.

The First-tier and Upper Tribunals both decided that the loan interest was not deductible due to the ‘unallowable purpose’ rule, based on the acquisition having already been decided in the US and no obvious reason why a UK acquisition company was used. However, the structure probably could have worked with a UK target – which is why the anti-hybrid rules were needed to prevent this arrangement from working.

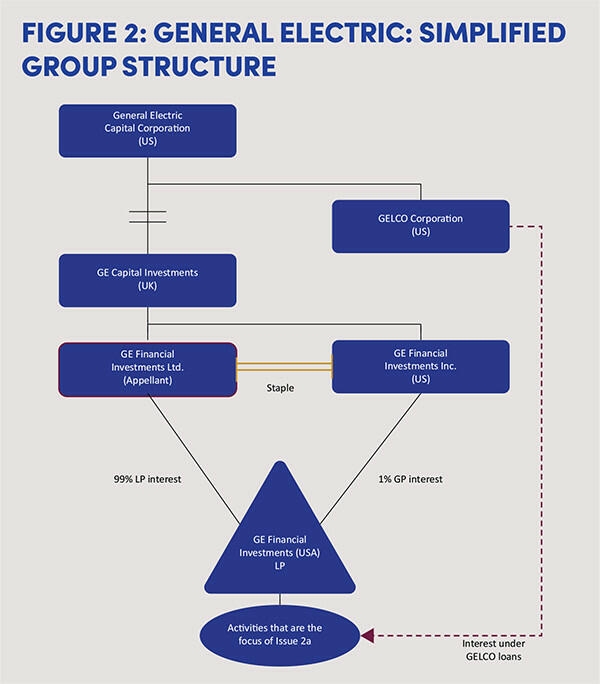

GE Financial Investments Ltd

The second case is GE Financial Investments Ltd [2023] UKUT 146 and there’s another flow chart, taken from the Upper Tribunal judgment (see Figure 2: General Electric: simplified group structure). In this case, the judgment notes that:

‘[The] structure was originally set up to obtain a US tax advantage. In the event, a change in US federal tax law meant that this advantage never materialised.

‘But the existence of the limited partnership also had a potential UK tax advantage in relation to the UK’s so-called “thin capitalisation” rules. A company whose equity capital is low compared to the amount of its debt is “thinly capitalised” and UK tax rules restrict the amount of interest deductions in those circumstances. The additional income arising to GE Financial Investments Ltd through the limited partnership structure was beneficial for the operation of those rules through an increased capacity to deduct interest. As it turned out, that extra capacity was not in fact needed.’

The ‘magic’ here was that the UK company changed its Articles of Association to provide that its shares were ‘stapled’ to the stock of a US company, requiring that both shares be transferred at the same time. The purpose of this was to treat the UK company as a US resident company under US domestic law. As a deemed US company, it was subject to US tax on its share of profits from the Delaware limited partnership – and US tax was paid on those profits.

The case was about whether the UK company could claim double tax relief for that US tax. This required that it be treated as a US resident for the purposes of the UK-US Double Tax Treaty. The Upper Tribunal reversed the decision at the First-tier Tribunal and decided that the company did qualify as a US resident under the treaty.

In conclusion

As the BEPS report on Action 2 said: ‘These types of arrangements are widespread and result in a substantial erosion of the taxable bases of the countries concerned. They have an overall negative impact on competition, efficiency, transparency and fairness.’

No doubt tax authorities hope that these types of diagram have been consigned to history.