The VAT treatment of private hire vehicles

Share this article

Is it time to rationalise the VAT treatment of private hire vehicles?

Very little happened on Tax Administration and Maintenance Day, with just two documents issued and two further topics mentioned (see tinyurl.com/2dyr4n87). Umbrellas remain a cause of concern to the government, which ‘is minded to introduce a due diligence requirement to drive out bad actors from labour supply chains’. This sounds like an additional responsibility for engagers. There may be a new VAT relief where VAT registered businesses give low value goods to charities. And… drumroll… the government will ‘mandate employers operating in a freeport or investment zone special tax site to provide their employee’s workplace postcode to HMRC’ where they are claiming National Insurance relief.

Private hire vehicles

The most interesting document concerns the VAT treatment of private hire vehicles (PHVs) (see tinyurl.com/5mrcwhxx). Most of us are aware of the transformation in the mini-cab market whereby, alongside traditional booking methods, platforms allow us to book journeys through an app.

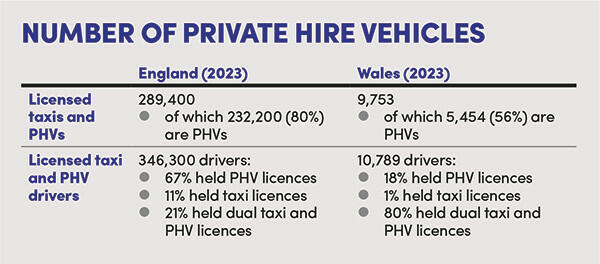

For some reason, there is a much higher proportion of PHVs in England, compared to Wales (see the box below).

PHV operators need to be licensed in order to be able to accept bookings and dispatch vehicles. In 2023, there were 15,000 licensed PHV operators in England (1,600 of which are licensed in London), and 738 in Wales.

Until the arrival of Uber on the scene, everyone merrily proceeded on the basis that the PHV operators acted as agents for the PHV drivers – almost all of whom are self-employed. This meant that the operators might have needed to charge VAT on their services, if their turnover exceeded the VAT registration limit, but very few drivers registered for VAT. Consequently, they absorbed the VAT on their purchases of vehicles, fuel and maintenance and the operator fee but did not charge VAT on their own labour.

Strangely, though, there is a category of VAT registered PHV operators, which act as principal – which meant they charged VAT to business customers, most of which recovered it as input tax, unless unlucky enough to be exempt. Many of us would have found it hard to discern the difference between operators acting as agents and those acting as principal.

Implications of Uber

In Uber’s case before the Supreme Court on employment rights for its drivers (Uber v Aslam [2018] EWCA Civ 2748), the court suggested that Uber might be acting as principal. Uber then asked the High Court whether their lordships had really meant that – and the High Court confirmed that in order to operate lawfully, a PHV operator licensed in London who accepts a booking from a passenger is required to enter as principal into a contractual obligation with the passenger to provide the journey.

Uber took a further case to the High Court to ask if this was the same outside London, where different licensing law applies. Again, the High Court confirmed that the PHV operator must act as principal. Thus everyone has been operating under a misconception for some 50 years.

This has VAT implications – and the reason for Uber’s forays before the High Court has become clear. Uber, supported by other platforms, sought a level playing field, where all PHV operators need to levy VAT on all private hire journeys. The judgments do not affect the licensed taxi market, where operators do act as agents for taxi drivers.

Following the original London judgment, Transport for London has required that all PHV operators act as principal, which has meant that VAT has been levied on fares. However, up to now, this has not applied outside London.

This has sparked the government into action – hence this consultation. Those who seek coherence in tax policy would probably wish to see all PHV journeys subject to VAT. There is equally no obvious reason why taxi journeys should be effectively outside VAT.

However, fares would need to rise as a result. The government estimates that the net effect could be that fares rise by 1.25% to 2.5%, or between £2.70 and £5.60 per year, per consumer. There would also be an increase in administration for drivers, who would need to register and account for VAT, possibly using a simplified flat rate scheme.

Australia has considered this challenge and decided that all taxi and private hire journeys should be subject to goods and services tax, without a de minimis threshold (see tinyurl.com/ra7kefd5). Surely it is time that we do the same?