Adapting to new realities

Share this article

Claudio Fischer considers four trends that are shaping the global indirect tax landscape

Key Points

What is the issue?

The indirect tax world is in constant motion. What was true yesterday or even today may prove to be wrong tomorrow

What does it mean for me?

Ignoring recent developments in indirect taxes or non compliance with indirect tax obligations can become an expensive oversight for companies of all sizes, whether they are active in the local market or the global one

What can I take away?

Only those who pinpoint which changes are most relevant to their business and where to take action can prepare effectively

This article discusses the latest trends and developments in indirect tax around the world and what business leaders should watch out for in 2015

and beyond.

Indirect taxes continue to grow

Whether the need is to finance targeted stimulation programmes for a local economy or to make up for the gaps left behind by a shrinking economy, indirect taxes have become pre-eminent revenue generators for governments in many countries. This trend shows particularly well when looking at the development of the tax rates in the 28 European Union (EU) members see Table 1. In practice, there are three main ways that contribute to the constant growth of indirect taxes:

- New VAT/GST systems are spreading. Limited to fewer than 10 countries in the late 1960s, today 164 nations levy a general tax on consumption such as value added tax (VAT) or goods and services tax (GST): 46 in Africa, one in North America, 18 in Central America and the Caribbean, 12 in South America, 28 in Asia, 51 in Europe and eight in Oceania (OECD, Consumption Tax Trends 2014, p171). Other countries such as the US apply retail sales taxes. Only a minority of countries has no general consumption tax in place.

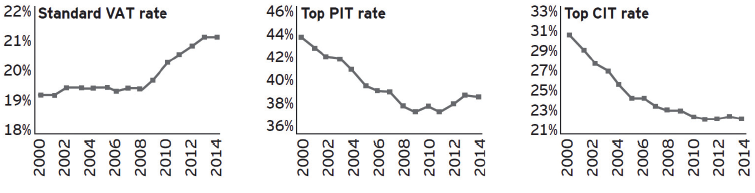

- VAT/GST rates are rising. In countries where there is already a sales tax, average rates have increased in recent years and these seem set to continue their upward trend. This is particularly true for Europe, where the average standard VAT rate has reached 21.6%, and the OECD countries, where it is now running at 19.2%. These compare with 19.5% and 17.5% respectively before the start of the global economic crisis in 2008.

- Excise taxes are spreading and increasing. Classic excise taxes on alcohol, tobacco or mineral oil have been a solid source of revenue in most countries for years. The general direction of the rates of these taxes is clearly upwards rather than down. In addition, new taxes are introduced, such as the sugar taxes on ‘unhealthy’ food. In many countries, these taxes may be linked to spending on health and welfare. As populations age and the pressures on government spending in these areas increase, these taxes may become more widespread. A popular target for new taxes is the financial sector, where many countries have increased supervision of the banking industry and tightened regulations. In Europe, the preferred approach has been to levy taxes on financial transactions. France introduced a financial transactions tax in August 2012; and on 1 January 2013, Hungary introduced a tax on payment services. Italy followed with a tax on the transfer of shares and derivatives and high-frequency trading in March 2013.

Table 1

| Evolution of standard VAT, and top CIT and PIT rates, EU-28 (simple arithmetic averages) | ||

Image

|

||

|

European Commission, TAXATION PAPERS, WORKING PAPER N. 49 – 2014, A wind of change? Reforms of Tax Systems since the launch of Europe 2020, 2014, p6 |

Indirect taxes are adapting to new economic realities

Indirect taxes are strongly intertwined with the economy given the fact that the tax is on an economic transaction, such as the sale of a good or the provision of a service. If the nature of these transactions or the way that such transactions are handled change, this would have a strong impact on indirect taxation. E-commerce and virtual currencies are two examples of developments that are on the radar of more governments. Current rules of taxation tend not to capture electronic cross-border transactions as well as they could. This oversight in their design can lead to a distortion of competition between local and foreign vendors and has a significant impact on VAT revenues, particularly in relation to scenarios involving sales to final consumers (B2C transactions). Australia, for example, expects additional revenue of A$350 million over four years by levelling the playing field for the suppliers of digital products and services in Australia in relation to their GST (media release by the Treasurer of the Commonwealth of Australia, 11 May 2015).

Recent examples of how the digital economy is influencing VAT law include the new EU rules for the place of supply of B2C electronic services. Since 1 January these services have been subject to tax where the customer is established or resident (instead of where the supplier is established). This requires foreign service providers to register and pay VAT in the EU member state of the consumer. Similar rules have been or are about to be introduced in Albania, Angola, Japan, South Africa and South Korea.

Another interesting development in the digital age which is yet to be captured by VAT law is the use of virtual currencies such as bitcoin. The tax authorities of only a few countries, including Australia, Singapore and the UK, have issued guidelines on the VAT treatment of these crypto-currencies. However, each country is adopting a different position, a pattern that may be expected to continue. Some countries have banned bitcoins outright, Russia and Vietnam among them. In other countries the revenue authorities are assessing the tax treatment, and additional country-specific guidance is expected – from both an indirect and direct tax perspective. This lack of global consistency may lead to a number of challenges for businesses operating in this market.

The global trade landscape is changing fast

While governments are counting on exports for growth, they are at the same time restricting imports. On the positive side, it should be mentioned that countries are negotiating measures to facilitate trade. The World Trade Organization (WTO) reports 604 active and pending reciprocal regional trade agreements among its members. The WTO continues to foster the lowering of trade barriers and the streamlining of the rules governing them. However, the situation is complex. In many cases, duty rates are high and as, unlike VAT/GST, duties charged at one stage in the supply chain are not offset against taxes due at later stages, they form part of the cost base of goods affected. In addition, customs clearance procedures can add to the time and related costs of moving goods cross-border. In many cases, businesses are not obtaining the potential benefits offered by trade agreements because they cannot or do not meet the qualifying conditions. Experience shows that only a minority of businesses is up to date with the customs procedures and applies the correct customs classifications and tariffs on products. In addition, in their constant search for revenue, jurisdictions are increasingly focusing on the customs tax base. There are attempts to increase the base, such as eliminating the first-sale concept and tightening the definition of dutiable royalties. This is reflecting a global trend. The result could be that royalties and service fees will have to be added to the value of imported goods to properly reflect their value, thus enlarging the customs tax base.

Tax authorities are focusing on enforcement of indirect taxes

Tax audits are changing. Tax and customs inspectors are increasingly using modern technology tools to access real-time comparative figures and data when auditing businesses. They are sharing more information, and tax administrations around the world are implementing electronic auditing of businesses’ financial records and systems. In many cases, taxpayers’ information is under scrutiny even without an on-site audit taking place.

New developments in technology and e-auditing are also paving the way for mandatory electronic invoicing and electronic filing of tax returns, which are fast becoming the global norm.

More jurisdictions require taxpayers to provide their financial data in a specific format, such as standard audit file, SAF-T, which often means that businesses have to adapt their reporting systems and make costly investments.

The benefits for tax administrations are clear: the more efficient use of technology lowers costs of collection and compliance and increases the number of errors detected. In addition, tax and post-importation audits are becoming more difficult to deal with for poorly prepared companies. On the flipside, knowledgeable and prepared taxpayers may find it easier to deal with more professional tax and customs administrations.

Conclusion

Our experience shows that many companies still pay too much indirect tax, often because they do not identify and manage these duties and their associated costs effectively. For example, many companies are not aware of exemptions or refund schemes for which they may qualify, such as energy taxes.

Many global companies could save millions of dollars in customs duty costs by making small changes in their supply chains to meet the qualifying conditions of free trade agreements. Similarly, small changes to how or where you do business may reduce your number of VAT/GST registrations and the related compliance risks.

More than ever, it pays out to proactively manage indirect taxes. Establishing a clear indirect tax strategy will help keep a business up to date with the rapidly changing tax environment.