Into alignment

Share this article

Marian Drew and Angela Brown set out the OTS’s road map for bringing income tax and NICs closer together

Key Points

What is the issue?

The OTS has published reports on closer alignment of income tax and NICs and on Small Company taxation. Both reports can be found on the GOV.UK website.

What does it mean to me?

Bringing income tax and NICs together has been a constant call from tax advisers for many years; the OTS has set out a seven-stage plan for closer alignment. These would affect millions of people and most employers but would bring a simpler, better understood system

What can I take away?

The OTS will be doing further work on aspects on the alignment and indeed small companies so there is plenty of scope to contribute to the debate

A regular theme of reports by the Office of Tax Simplification (OTS) has been that life would be simpler if income tax/PAYE (IT) and national insurance contributions (NICs) were brought together. Not necessarily combined into one single levy – there are obvious problems with doing that, not least the prospect of a 32% basic tax rate.

But in a succession of reports – on small business, tax reliefs, competitiveness of the UK’s tax system and most recently on employment status – we have pointed to the simpler administration for employers and HMRC, with less scope for errors, that closer alignment of IT and NICs would bring. Add to that the way that a common system will be much easier for taxpayers to understand and there seems to be an irrefutable case for progressing the idea.

Aims of the project

After the 2015 election, Ministers were quickly convinced of the merits of really working at the IT/NICs project, and in his summer Budget 2015 the Chancellor of the Exchequer confirmed that the OTS would be conducting a review into the closer alignment of IT and NICs.

The Financial Secretary to the Treasury set out an ambition that the OTS would take a greater role in the public debate, and asked us to consider the impacts, costs and benefits and the steps necessary to achieve closer alignment. This was key: the OTS wouldn’t find it difficult to find people to support the idea of alignment (we have always found huge support for bringing the two taxes together) but what we were asked to do was to bring out the implications of so doing. Who would pay more – and would they gain? Who would pay less? What really would be the simplification gains? Was the gain worth the pain?

In setting the project rolling, John Whiting posed five broad questions:

- Can we move to a common definition for Income Tax and NICs for earnings?

- What about moving NICs to an annual, aggregate and cumulative basis?

- Should the self-employed pay (and benefit) in the same way as the employed?

- Is the contributory principle still worth it?

- What of employers’ NICs?

- As the work progressed, we added other questions such as:

- What lessons can we draw from other countries?

- Why are benefits in kind treated differently for NICs?

- Can we improve the system for employees coming to and leaving the UK?

- Why can’t NICs be changed in the Finance Bill?

Thus, like Bob Dylan in one of his greatest songs, we posed nine questions. As we went along we, unlike Dylan, added more questions but also, unlike Dylan, ended up with answers that we think are not just ‘Blowin in the wind’.

Gathering the evidence

Our project followed by now established OTS processes: assemble an excellent team, set up a Consultative Committee to guide us, gather evidence from all the interested parties we could identify (we held more than 70 meetings), do lots of research and work with HMRC and HMT (especially HMRC’s Knowledge Analysis and Intelligence team of economists and statisticians). We also put up two online surveys which attracted 650 responses, many from ordinary taxpayers.

Based on all this work, we have identified some overriding principles and a clear desire for change from stakeholders:

- The current NICs system no longer supports the UK’s flexible workforce model, diverse business structures and flexible reward.

- The inherent complexity of NICs means the regime is not well understood by employers or individuals, and is complex to administer.

- There is distortion built into the system – two individuals with the same gross income, constituted differently, may have very different NICs outcomes, and possibly be entitled to different benefits; some employers use the NICs structure to influence work patterns (part time/self-employed).

None of this will be news to readers of Tax Adviser, we suspect. Many will be silently (or loudly?) saying ‘just get on with it’. Indeed, one group of entrepreneurial businesses we met really didn’t see the need to discuss the project: to them it was a case of ‘just do it’. But as they conceded when we insisted on going through some of the issues, it isn’t as easy as that and it was clear from the outset that changes in the rules had the potential to affect many, many people.

Bringing them together

We developed a seven-stage plan for closer alignment. The steps are designed as a package and intended to be taken forward as such to achieve major reform. That will take time: ideally there would be a well-signposted path for such major changes. One reason for presenting these steps as a package is that many are interdependent or are facilitated by others. But we have also tried to indicate which steps can be done separately on a ‘standalone’ basis.

So what are the seven steps? What follows is a summary and there is a lot more analysis and detail in the report.

One: Move to annual assessment

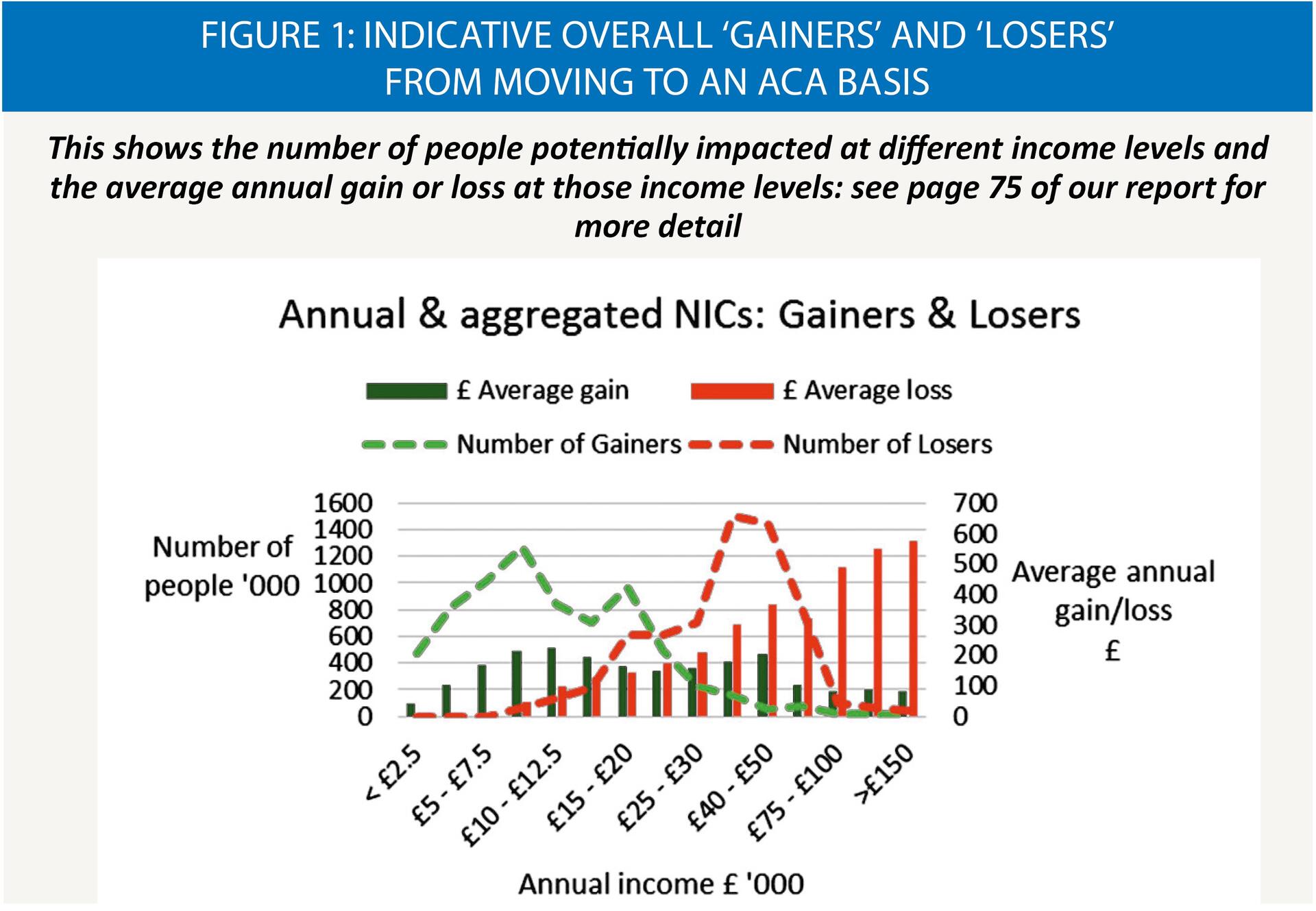

Move to an annual, cumulative and aggregated (ACA) assessment period for employees’ NICs on employment income, similar to PAYE IT. This is probably the key step and would address the headline finding that the current structure of NICs is no longer fit for purpose for a modern flexible workforce. It would necessitate a NICs code for individuals, similar to the PAYE code.

It would create a straightforward system that is clear, and simpler to understand and to administer (including for HMRC). As with many of our steps, taxpayers will need to have the implications clearly explained and phased in: the change would create ‘losers’ as well as ‘gainers’. It is estimated that 6.3 million would pay more NICs but 7.1 million would pay less (and these tend to be lower earners – see Figure 1). Some of those with more than one job below the NICs threshold would pay NICs but would get access to work related benefits for the first time. We did not find any policy rationale for the cash advantage received at present by those who would pay more under an ACA approach.

Two: Base NICs on whole payroll costs

Base employers’ NICs on whole payroll costs to make it easier to understand and reduce distortions created by the current system, such as any incentive for fragmented hours. Although this replaces an existing tax and so is not necessarily an obvious simplification, we found that, in principle, the change would be welcomed by employers, creating a system that is simpler to understand and a tax that is easier to calculate. In addition, the name should be changed to more closely reflect its role and purpose; in other words, there seems no justification for keeping the NICs part of the name, though the proceeds of the tax would continue to be accounted for in the National Insurance Fund.

We assume that the overall receipts raised from the payroll levy (our starter for the new name) would remain the same; the new tax could be set at a lower rate (perhaps 10%, or higher with an allowance per employer) than the existing 13.8% rate and still achieve this. The consequential impact on the labour market around part time employment (recognising that some employees choose to work part time) and sectoral impacts need to be understood.

Three: Align self-employed with employed

More closely aligning the NICs position for the UK’s 4.7 million, and rising, self-employed with that of employees would remove complexity and potentially converge benefits entitlements. This is increasingly necessary as more people have both earnings and self-employed income.

We found wide support for the premise that the self-employed would accept paying more NICs in return for more benefits (e.g. some form of sickness / unemployment benefit). But again there is a lot to test and make sure people understand.

Four: NICs need to be a more transparent system

To help make closer alignment possible, NICs needs to be a more transparent system. Confusion abounds about the contributory principle with much misunderstanding about its real impact. Many question its continuing relevance; but many others see it as a cornerstone of our tax and welfare system. On pure simplification grounds the OTS could argue for its abolition, with consequent administrative savings for HMRC.

We think the contributory principle should be critically examined and, as a first step, there should be a drive to improve understanding to inform a proper debate to enable the government in (say) five years’ time to take a decision on its future. Greater visibility can be achieved through HMRC’s personal tax accounts and a simple step to better understanding is to abolish the NIC ‘classes’ and instead label them what they are: Employee, Self-employed, Voluntary and Employer contributions.

Five: Align legislation for income tax and NICs

Align the legislation for IT (relating to employment income) and NICs so that the scopes of the charges are the same, and taxpayers benefit from identical reliefs for IT and NICs purposes. This would make it easier for individuals and employers to understand, and improve compliance. Aligning the reliefs available for IT and NICs would create a more equal system for employees and reduce the admin burden of managing the differences for employers. There would be savings (and fewer errors) from having rules and an administration that are more straightforward and understandable. It would probably result in more NIC expenses claims and some additional exchequer cost. The treatment of pensions was outside the scope of our report.

We think we have developed the definitive list of differences between IT and NICs (see Annex G of the report) but do let us know if you think we have missed any!

Six: Bring taxable benefits in kind (BIKs) into Class 1 NICs and abolish Class 1A NICs

This simplifies the administration and remove distortions in the NICs treatment of non-cash remuneration. It would be facilitated by the ACA change above or by payrolling, but neither are absolute pre-requisites.

It is noticeable that concerns in earlier OTS reviews about this leading to increased bills for employees have largely evaporated (though are still acknowledged), to be replaced by strong views that the current system is inequitable and creates unfairness.

Seven: Full alignment of legislation and procedures

A fully joined up approach to the two taxes across policy and administration requires the alignment of legislation and procedures, and where possible the matrix of rates and thresholds. HMRC guidance and support needs to be better linked and a legislative route found to ensure that changes to IT and NICs are simultaneous and equivalent.

We have considered whether NICs could be changed within a Finance Bill: this founders on Parliamentary procedure. But we set out how it can be managed with a change to NICs legislation, so that future relevant IT changes would automatically apply to NICs as well.

What next?

Readers will be aware that in the March Budget, The Chancellor didn’t immediately say he was going to embrace all our recommendations. We didn’t expect him to: indeed, we didn’t want him to. There is more work needed. HMT and HMRC are going to carefully consider our report but in parallel we are going to do more work on two key proposals to explore further the impact on individuals, businesses (and sectors), the exchequer and HMRC of:

- Moving to an annual, cumulative and aggregated assessment period for employees’ NICs on employment income.

- Changing from employers’ NICs to a payroll-based charge.

In both cases we need to set out options and choices for consideration prior to any implementation. We will be carrying out a lot more research and analysis rather than evidence-gathering visits but as always would welcome comments and input on these issues and indeed any aspects of our project. Please write to us at: [email protected].

Our target is to produce our further reports by the end of September so that Ministers can respond to our combined report in or before the Autumn Statement.

John Whiting outlines the OTS's small companies report

A few days before publishing the IT/NICs report, the OTS published a report on Small Company taxation. The report contained 13 main recommendations; far from being an unlucky number, the report attracted an immediate response in the Budget with a letter from the Financial Secretary (published on the OTS website) setting out that the Government would accept six of the recommendations, consider six more and reject only one (for a long-term study of a consolidated tax system). Indeed, there is already action, with the announcement of longer HMRC ‘opening hours’.

Two recommendations are for the OTS to do more work to develop and test outlines for concepts we know are controversial:

A ‘sole enterprise protected asset’ vehicle to test whether such a new entity could help enterprise by giving sole traders a system that would give them some asset protection without the need to form a company. But would this work in practice? Would it be accepted commercially? Would it need safeguards?

A ‘lookthrough’ basis of taxation to tax some small companies by ignoring the company and simply taxing the proprietors. In concept this would be simpler as it would eliminate the need for corporation tax computations and returns. But it wouldn’t suit a company that wanted to retain funds; so would it be possible to define a type of company that would find the route simpler?

In both cases we plan to publish an outline for comment with a view to concluding in September whether either or both routes can deliver simplification. We would welcome input: do read the analysis and conclusions in our report and let us know at [email protected].