Are you selling a business?

Share this article

Neil Warren considers some practical issues with the transfer of a going concern rules that can often produce difficult challenges for advisers

Key Points

What is the issue?

Many factors need to be considered to decide if a deal relates to the sale of a business. Important conditions must be met by buyers and sellers for a TOGC to apply for VAT purposes. There are extra requirements if property is involved in the deal.

What does it mean to me?

Buyers need to ensure they are not incorrectly charged VAT by a seller. Input tax cannot be claimed on incorrectly charged VAT. This could leave the buyer with a large irrecoverable VAT bill and problems with HMRC.

What can I take away?

A buyer must also obtain information from the seller about any outstanding capital goods scheme adjustments. The buyer will be responsible for carrying out the remaining annual adjustments after the deal has taken place.

There are probably few subjects in the world of VAT that cause as many headaches as the transfer of a going concern (TOGC) rules. Is a business being sold or just individual assets? And if a business is being sold, do the buyers and sellers both meet the necessary conditions to avoid a VAT charge; i.e. is the supply outside the scope of VAT as a supply of neither goods nor services?

In this article, I will share some practical quirks of the TOGC rules and highlight various pitfalls that it is important to consider.

Business or assets?

The starting point with any business sale is that there must be a flow of income or expected income that is being transferred from the seller to a buyer. Think about a long-established restaurant, which has built up a strong reputati on for serving high quality food. The deal to sell the business will usually mean that the buyer will purchase all stock and fixed assets, and retain existing employees, making an extra payment for goodwill.

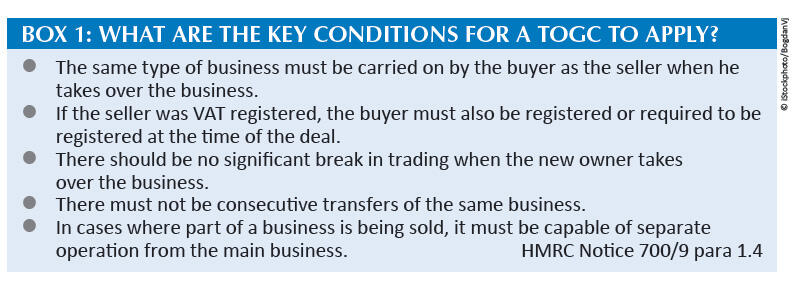

To qualify as a TOGC, with no VAT charged on the proceeds, there are important conditions that must be met. See Box 1: What are the key conditions for a TOGC to apply?

I am often asked whether a charge for goodwill is an essential feature of a TOGC. The answer is ‘no’: a goodwill payment is an indicator of a business sale but not conclusive. For example, a loss-making business is still a business but there will probably be no value or payment for goodwill.

VAT registration

Imagine the following situation: a business sale is imminent but the buyer’s VAT registration number has not been issued by HMRC. Does this mean that the TOGC will fail and VAT must be charged on the deal? This is where the phrase ‘registered or required to be registered’ becomes important.

A quirk with the VAT registration rules is that the buyer must treat the previous 12 month’s taxable turnover of the seller as if it were his own (Value Added Tax Act 1994 s 49(1)). This usually means that the buyer must register for VAT from the day he takes over the business if the seller’s taxable turnover exceeded the annual £85,000 registration threshold. The buyer is therefore liable to register for VAT and has passed the TOGC condition, despite the absence of a VAT number at the time of the deal. However, if the seller’s annual taxable turnover is less than £85,000, there is a problem (see HMRC Notice 700/9 para 2.2.4).

Input tax

What would be the situation if the buyer paid VAT to the seller when it should have been outside the scope of VAT as a TOGC and the buyer has claimed input tax on his VAT return? The answer is that HMRC would disallow the claim because input tax can only be claimed on correctly charged VAT. The buyer must revert to the seller for a VAT credit.

However, what happens if the seller cannot be found because he has left the UK and emigrated to Spain? There is a potential get-out-of-jail card: as long as HMRC is ‘wholly satisfied’ that the seller has declared and paid the output tax, it will exceptionally allow the buyer’s input tax claim under ‘care and management of the Revenue’ (see HMRC VAT Manual VTOGC4150).

Legal entity issues

Imagine the following scenario: Bill and Ben Ltd rents The White Hart pub from a brewery and the company has agreed to buy the freehold for £500,000. However, the brewery will charge 20% VAT because of an option to tax election it made on the building. Is this correct?

The TOGC rules fail here and VAT must be charged: this is because Bill and Ben Ltd will not be carrying on the same type of business as the brewery. The brewery’s income is from ‘rent’ that will cease when Bill and Ben Ltd buys the freehold. However, a potential solution is available which makes commercial sense because it keeps the property asset out of the trading business, as set out below:

- Directors Bill and Ben could buy the pub in a separate legal entity, say a partnership.

- The partnership must register for VAT and also opt to tax the property before it is transferred. This is an extra condition of the TOGC rules: if the seller has opted to tax a property, the buyer must also opt as well before the deal takes place. The buyers must also confirm to the seller that the option to tax election will not be disapplied. (See below for information on anti -avoidance legislation.)

- The partnership will rent the building to Bill and Ben Ltd at a market rate, so it will have the same income flow as the brewery. It therefore meets the ‘same type of business’ condition of a TOGC.

- The TOGC conditions have been fully met, so the sale will be for £500,000 and no VAT. This produces an important saving of stamp duty land tax, which is charged on the VAT inclusive price of a property sale.

New building is sold

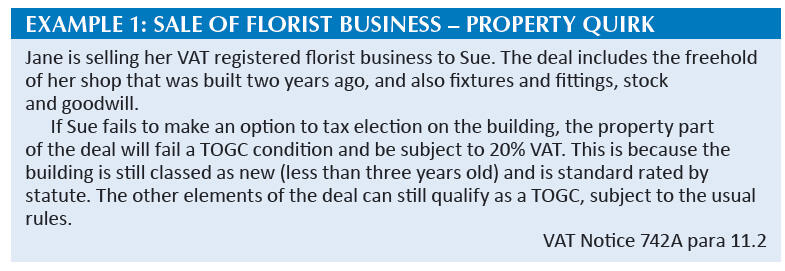

There is one other situation when a buyer must make an option to tax election on a property, even if it has not been made by a seller. This is where a TOGC involves a freehold property which is less than three years old; i.e. it is still classed as new for VAT purposes. See Example 1: Sale of florist business – property quirk.

Anti-avoidance legislation

The reason that the Bill and Ben Ltd arrangement is acceptable VAT planning is because a pub trades as a fully taxable business with no input tax restriction. However, anti-avoidance legislation (VAT Notice 742A s 13) would prevent this route if three conditions apply:

- The landlord buying the property and tenant renting it are connected to each other (Corporation Tax Act 2010 s 1122).

- The tenant has less than 80% taxable supplies; i.e. where an input tax block would apply.

- The property would come within the capital goods scheme; i.e. the selling price is more than £250,000 excluding VAT.

If the above conditions apply, the buyer’s option to tax election with HMRC is disapplied, so the rental income will still be exempt from VAT; i.e. preventing an input tax claim on the purchase of the building and other costs.

The reason for the anti-avoidance rules is very logical: it prevents an exempt business from buying a property in a connected business and claiming a lot of input tax on the purchase of the building, only drip-feeding output tax to the tenant when rent is charged in the future.

Capital goods scheme

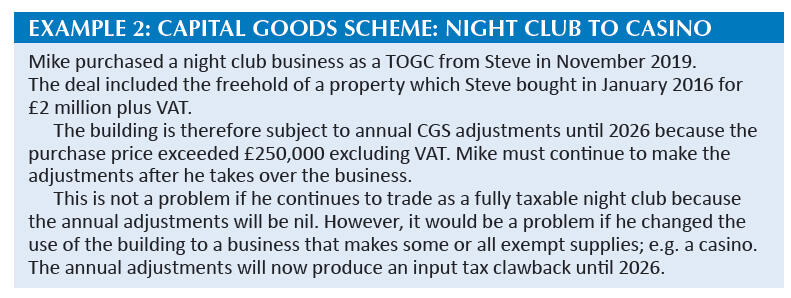

Never underestimate the power of the nation’s favourite tax to produce an unexpected quirk – in footballing terms, the last-minute winning goal against the run of play. A quirk of the TOGC rules, often forgotten, is that the buyer of a business takes over any remaining capital goods scheme (CGS) intervals of the seller. See Example 2: Capital goods scheme: Night club to casino.

The quirk with the CGS is that a business might have to repay input tax that it has not claimed in the first place. This is an unusual outcome. However, the commercial reality is that the rules will only be relevant if exempt supplies are involved in the equation.

Final tips

Here are two final tips:

- Buyers should not be tempted to keep the seller’s VAT number. This route, often known as a VAT68 procedure, means that the buyer is liable for any errors made by the seller on their VAT returns for the previous four years.

- When considering whether a TOGC applies, always look at the bigger picture of the deal to decide if a business is being sold rather than individual assets. Most importantly, don’t waste time writing to HMRC for a ruling if you’re unsure. It will refuse the request and instead refer you to its extensive published guidance.