Around the world in 13 reports

Share this article

Joy Svasti-Salee contemplates a period of unprecedented change for international corporate tax law

Key Points

What is the issue?

Recommendations made in the G20/OECD BEPS project have been ratified, approved and adopted. The project is now moving to the implementation phase and to a period of unprecedented change for corporates

What does it mean to me?

Most changes will apply regardless of a group’s size, although the focus (and debate) so far has been on the larger multinationals

What can I take away?

An awareness of the key issues to consider and monitor

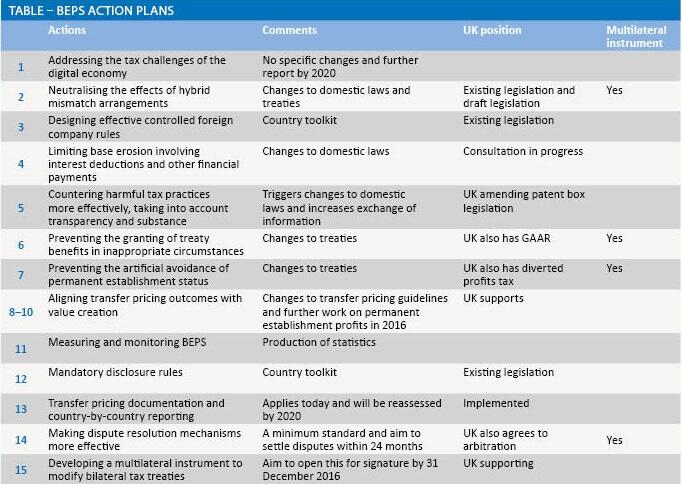

In November 2015 the G20 ratified, approved and adopted recommendations made in 13 reports produced by the OECD to counter Base Erosion and Profit Shifting (BEPS) – summarised in the Table. The recommendations take the form of new minimum standards, common approaches and guidance.

The original tax policy concerns were that ‘due to gaps in the interaction of different tax systems, and in some cases because of the application of bilateral tax treaties, income from cross-border activities may go untaxed anywhere, or be only unduly lowly taxed’. The OECD estimates the global revenue loss at $100bn–240bn (action 11 report) and will be monitoring the success of the project.

Initially, a significant focus was on the digital economy, and this generated the longest report. This sensibly concluded that ‘it would be difficult, if not impossible, to ring-fence the digital economy from the rest of the economy’, but developments would be monitored and a further report produced by 2020.

Two reports have been the subject of much discussion and, while important, are mentioned only briefly given that groups should know whether they are affected and should be considering their position.

- The report on ‘transfer pricing documentation and country-by-country reporting’ (CBCR), action 13, introduces a new filing requirement for multinational enterprises with annual consolidated group revenue of more than €750m for fiscal years beginning on, or after, 1 January 2016. This requires information on income, taxes paid, and economic activity by country, and will generally be filed in the parent company jurisdiction and made available to other jurisdictions under exchange of information procedures.

- The report on ‘neutralising the effects of hybrid mismatch arrangements’, action 2, which recommends that countries introduce primary and defensive rules to target arrangements that exploit differences in the tax treatment of an entity (one country regards it as ‘opaque’, the other as ‘see through’), or an instrument (one country regards a payment as interest, the other as a dividend).

Actions requiring implementation in domestic law

It is unsurprising that several countries agreed that BEPS counter measures require countries to make changes to their domestic tax laws because it is these differences that give rise to planning opportunities. Two significant recommendations fall into this category.

Limiting base erosion involving interest deductions (action 4)

The G20/OECD recommends that an entity’s net deduction for interest (and economically equivalent payments) should be limited to a percentage of its earnings before interest, taxes, depreciation and amortisation (EBITDA) within a corridor of possible ratios of 10%–30%. An optional group ratio rule, enabling an entity to deduct additional interest up to the level of the net interest/EBITDA ratio of its worldwide group, or by reference to the equity and assets of an entity or a group, is also proposed. This could be accompanied by an uplift of up to 10% in the group’s net third party interest expense.

Reliefs are accepted if there is less risk of BEPS and include:

- a de minimis threshold;

- an exclusion for interest on third-party loans used to fund public-benefit projects; and

- the carry forward of disallowed interest expense or unused interest capacity for use in future years. This is intended to reduce the impact of earnings volatility and assist long-term investments that generate income in later years.

In addition, the position of the financial sector will be considered this year.

This is an important issue for most taxpayers. Some groups will not obtain a tax deduction for all their third-party interest expense. It is particularly important in the UK, which has relatively generous rules, albeit with a worldwide debt cap provision. A consultation is under way. It can only be hoped that countries implement these recommendations so that domestic groups can obtain full deduction for their third-party interest expense.

All groups claiming a deduction for interest expense ought to assess their global positions and track domestic changes in this area.

Countering harmful tax practices more effectively (action 5)

All countries compete to attract investment and the topic of harmful tax competition has been on the OECD’s agenda for years. The current focus is on preferential regimes, with the initial spotlight on 16 intellectual property regimes, including the UK’s patent box arrangement, and on substantial activities (the 12th factor in the OECD’s 1998 report has become the key factor today), riding on the back of work done by the EU. The recommendation is that there should be a nexus between the income-receiving benefits and the expenditure contributing to that income, with the spend on developing or improving intellectual property being a proxy for substantial activities. Other preferential regimes will be revisited in the light of this focus on substantial activities.

The UK is amending its patent box regime and groups benefiting from this will be aware of the position. More generally, groups benefiting from other preferential arrangements must consider the new focus on substantial activities and consider their future position.

The recommendations also focus on the lack of transparency in relation to largely unilateral rulings given to taxpayers on:

- preferential regimes;

- cross-border pricing arrangements;

- downwards adjustment to profits;

- permanent establishments; and

- conduit arrangements.

Exchange of information of such rulings will take place from 1 April, with some past rulings being exchanged by 31 December. Taxpayers need to take this into account in requesting unilateral rulings.

Actions to help countries introduce domestic laws

Two reports provide guidance to countries seeking to introduce domestic laws that have already been adopted by some other states, including the UK:

- The first relates to controlled foreign company (CFC) rules, action 3, that the OECD continues to recommend because they respond to the risk that income can be shifted to another country or by engaging a third country. The report suggests that credit countries give relief for CFC tax paid, but there is no discussion on how such double (or multiple) taxation could be resolved under treaties themselves.

- The second relates to mandatory tax disclosure rules, action 12, that is intended to provide early information about tax avoidance schemes and to act as a deterrent. It suggests that these rules are also designed to capture international tax schemes.

Actions changing the transfer pricing guidelines

Work in this area heralds a significant change in emphasis in the OECD transfer pricing guidelines and will be adopted quickly. This is because changes to the guidelines do not necessarily require amending either domestic law or tax treaties.

The report brings together work on intangibles, the contractual allocation of risks and other high-risk areas, actions 8–10. It expresses concern that the current transfer pricing emphasis on the contractual allocation of functions, assets and risks is vulnerable to manipulation and can lead to outcomes not aligned with value creation.

The revised guidance requires careful ‘delineation’ of actual transactions between associated enterprises by considering both the contractual position and the conduct of the parties. If contracts are incomplete or not supported by the conduct of the parties, the conduct will supplement or replace the contractual arrangements. In essence, this is about arriving at what is considered to be the ‘real deal’ and not the ‘paper deal’ which is then priced. If an arrangement lacks commercial rationale it can be disregarded. Examples include:

- risks contractually assumed by a party that neither exercises control over them nor has the financial capacity to assume them should be allocated to the party that does;

- legal ownership of intangibles alone does not necessarily generate a right to all, or indeed any, of the return that is generated by their exploitation;

- discounts generated by the volume of goods ordered by several group companies should be allocated to those group companies, not to the purchasing company; and

- profits of a cash box should be equivalent to no more than a risk-free return.

Further work will be undertaken on profit splits and financial transactions.

Transfer pricing is a difficult science because it requires connected parties to transact in a similar manner to third parties in circumstances where those parties do not transact with each other consistently. A significant concern with these recommendations is the move away from the legal position, which is often the only constant factor in an arrangement that continues over several years, towards conduct that can change over time. It remains to be seen how this materialises in practice and when interest rates eventually rise.

Actions requiring treaty change

Two significant reports require changes to be made to tax treaties.

Preventing the artificial avoidance of permanent establishment status (action 7)

This report recommends the lowering of the threshold at which a company is regarded as having a taxable presence or permanent establishment (PE) in another territory and will need to be considered carefully by all taxpayers doing business abroad. A PE is likely to exist in future when:

- sales contracts are substantially negotiated in one country and finalised or authorised in another, or where ‘commissionaire arrangements’ exist;

- a ‘closely related’ enterprise acts as a sales agent for the taxpayer in another country;

- the taxpayer carries on specified activities, which have been regarded historically as preparatory or auxiliary and not giving rise to a PE, but which are his core business activities;

- a group fragments a cohesive operating business into several small operations, each of which is engaged in preparatory or auxiliary activities; and

- a group splits up contracts between closely related enterprises to benefit from the minimum period exception for construction sites.

This is bound to lead to more groups having more PEs and ‘accidental PEs’. Groups will need to monitor the position of each entity yearly. Follow-up work on the attribution of profits to PEs is planned with a view to providing guidance before the end of 2016. It must be hoped that this will reconsider the position that a PE may be treated as making a taxable profit when the entity of which it is a part makes a loss.

Preventing the granting of treaty benefits in inappropriate circumstances (action 6)

This report relates to treaty abuse and treaty shopping, which is identified as one of the most important sources of BEPS concerns. Countries have agreed to:

- change the treaty title and preamble to clarify that states entering into tax treaties intend to avoid creating opportunities for non-taxation or reduced taxation through evasion or avoidance (including treaty shopping); and

- include in their treaties:

- a limitation-on-benefits (LOB) rule – a US approach that limits the availability of treaty benefits to entities that meet particular conditions – and a principal purposes test (PPT) – a UK approach under which treaty benefits are denied if one of the principal purposes of the arrangements was to obtain them,

- the PPT alone, or

- the LOB rule supplemented by an anti-conduit financing rule.

This is about helping countries to introduce provisions in their treaties which the US and the UK already have.

- Include targeted rules to address specific situations where:

- dividends are transferred to reduce withholding taxes,

- a source state cannot tax a gain on disposal of shares in a company deriving its value from immovable property due to ‘aggressive planning’,

- an entity is resident in two states, and

- assets are transferred to a PE in a country that does not tax the income arising (or offers preferential treatment) by a company that exempts PE income.

We will have to wait to see what this means in practice and how the term ‘avoidance’ (rather than ‘abuse’) is interpreted. Groups that rely on treaty provisions, perhaps to benefit from reductions in the often high rates of withholding tax on the payment of interest, dividends and royalties, will need to consider whether they qualify for treaty benefits and whether the transaction itself qualifies.

Making dispute resolutions mechanisms more effective (action 14)

This is a welcome recommendation given that disputes are likely to increase as a result of BEPS counter-measures. The mutual agreement procedure (MAP) already provides a mechanism for doing this and countries have now agreed to a minimum standard, complemented by a set of best practices, to ensure that:

- treaty MAP obligations are fully implemented in good faith and disputes are resolved within 24 months;

- administrative processes are implemented to promote this; and

- eligible taxpayers can access MAP.

Several countries, including the UK, have also committed to provide mandatory binding MAP arbitration. Although a major step forward, taxpayers can only hope the list of countries signing up will increase.

A multilateral instrument

The challenge for governments is to amend the existing 3,000-plus bilateral tax treaties in a synchronised way, quickly. Agreement has been reached that a multilateral instrument is a desirable and feasible means of achieving this. It is expected that it would coexist with bilateral tax treaties and be negotiated through an international conference (chaired by a UK official). The aim is to open this instrument for signature by 31 December 2016.

For taxpayers, a multilateral instrument should allow treaty changes to be made quickly and with an element of consistency. In the long term, a coexisting multilateral treaty, with its proposed explanatory report and examples to provide guidance, will add a layer of complexity to bilateral tax treaties while not dealing with the underlying issue that business operates globally, not bilaterally.

Looking forward

The impact of the G20/OECD project will depend on whether, when and to what extent countries implement the recommendations and indeed what happens if some do not.

Taxpayers are faced with a period of unprecedented change in domestic laws and bilateral tax treaties and will need to monitor global changes carefully.