The Autumn Statement: the latest fiscal plan

Share this article

Approaching the end of 2022, we now have the chance to examine the repercussions of our fourth ‘budget’ this year.

After the wild exuberance of the 23 September Growth Plan, the Autumn Statement was a rather more sombre affair. The chancellor had been clear before the Statement that personal tax would rise, as would business tax. The Statement confirmed a series of tax increases, taking effect over the next two years.

Energy levies

The biggest tax increases come from the levies on oil and gas producers and on electricity generators. The rate of the Energy Profits Levy (on UK oil and gas production) increases from 25% to 35% from 1 January 2023; and the levy period will be extended from 31 December 2025 to March 2028. The investment allowance is reduced sharply from 80% to 29%, but there is a new decarbonisation allowance, set at 80% for upstream decarbonisation expenditure.

The Electricity Generator Levy applies from 1 January 2023 to March 2028 and will be a new 45% tax on revenues (before costs) above a pre-crisis price baseline of £75 per MWh made by certain renewable, nuclear and biomass electricity generators. Generation that falls under the Contracts for Difference regime is excluded, as are small generators.

The total forecast revenues are about £41.6 billion from oil and gas and £14.2 billion from electricity – almost exactly the cost of the consumer and business energy support schemes. The biggest uncertainty relates to energy prices and whether they stay high enough to pay the forecast levy but remain low enough not to necessitate further consumer and business support. An extension of the consumer support plan has been announced, to April 2024. However, there is no planned business support after the current plan runs out in April 2023.

Personal taxes

A much-trailed tax increase is the reduction of the additional rate threshold from £150,000 to £125,140. This odd number takes account of the tapered withdrawal of the personal allowance and so England and Northern Ireland will have income tax effective rates of 20%, 40%, 60% and 45%. Those liable to the high income child benefit charge also have a much higher effective rate on earnings between £50,000 and £60,000 (the exact rate depends on how much child benefit is paid and then withdrawn by the charge). Scotland will make its own choices in its December Budget. Theoretically, Wales also has choices over income tax rates, but its very limited devolved flexibility no doubt makes it likely that it will follow England.

The reduced threshold raises about £800 million annually. The number of individuals likely to be affected by reduction in threshold has not been released but HMRC’s latest data estimated that 678,000 taxpayers in 2022/23 will have income over £150,000, with a further 902,000 with income between £100,000 and £150,000 (see bit.ly/3i9BqyF).

The income tax and NI personal allowance and thresholds will be frozen at current levels for a further two years, to April 2028 – which is of course one of the biggest tax increases, albeit postponed.

The dividend allowance will be cut from its current £2,000 level to £1,000 for 2023/24 and thereafter to £500 annually. This initially brings in £450 million, rising to £900 million a couple of years later. The published documents do not indicate how many new taxpayers will be created by the reduced allowance. HMRC statistics estimate that about 4.2 million taxpayers currently have taxable dividend income, but we do not know how many additional people will need to file a self assessment tax return to report dividend income (see bit.ly/3GCNeDF). The reduced allowance affects owner-managed companies, which may be tempted to hold additional reserves to be realised as a capital gain when the business closes.

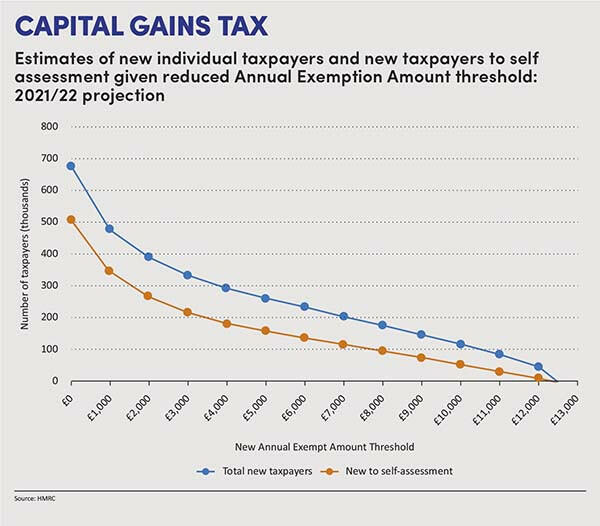

The capital gains tax annual exempt amount will be cut from £12,300 to £6,000 in 2023/24 and then to £3,000 for 2024/25 and subsequent years. This is estimated to bring in £275 million in the first year, rising to £425 million subsequently.

The allowance was covered in the first capital gains tax report from the Office of Tax Simplification (see bit.ly/3EW1TIN). The chart opposite shows that at a £6,000 level over 220,000 new taxpayers will pay capital gains tax and about 140,000 additional taxpayers will need to complete a self assessment tax return. Those numbers rise to about 340,000 new taxpayers and over 200,000 new tax returns in the following year. The report also suggested that HMRC should consider a standalone capital gains tax return to minimise burdens on taxpayers who need to report gains. Some individuals may be unaware that they need to report gains; HMRC will need to consider how to mount a publicity campaign. It would be helpful if they encouraged investment managers and platforms, as well as crypto exchanges, to publicise the capital gains requirements to their customers.

To counter possible remittance basis planning, the Spring Finance Bill 2023 will provide that shares and securities in a non-UK company acquired in exchange for securities in a UK close company will be deemed to be located in the UK. This will have effect where an individual has a material interest in both the UK and the non-UK company and where the share exchange is carried out on or after 17 November 2022.

Stamp duty land tax

One of the big measures in the September Growth Plan was an immediate £125,000 increase in the threshold at which stamp duty land tax applies to residential property, both for first-time buyers and everyone else. This was intended to be a permanent change, but the Autumn Statement will bring this to an end after 31 March 2025. No doubt this will aid those marketing properties in the preceding six months; the evidence of previous stamp duty land tax cuts shows that they benefit sellers more than buyers, by supporting higher house prices.

Business rates – and no online sales tax

The chancellor announced a significant business rates relief package, underpinned by adopting an April 2023 valuation, with transitional relief with ‘upward caps’ of 5%, 15% and 30% respectively, for small, medium and large properties in 2023/24. Downwards valuations receive full benefit immediately. The business rates multipliers will be frozen in 2023/24 at 49.9 pence and 51.2 pence, which is a 6% cut worth £9.3 billion over the next five years.

Support for eligible retail, hospitality and leisure businesses is being extended and increased from 50% to 75% business rates relief up to £110,000 per business in 2023/24. Around 230,000 properties will be eligible to receive this increased support at a cost of £2.1 billion. Rates increases for the smallest businesses losing eligibility or seeing reductions in small business rate relief or rural rate relief will be capped at £600 per year from 1 April 2023, costing over £500 million over the next three years and supporting over 80,000 small businesses.

R&D changes

The rates for R&D reliefs will change from 1 April 2023. The R&D Expenditure Credit will be increased from 13% to 20%, whilst the SME additional deduction is being reduced from 130% to 86% and the credit rate will be cut from 14.5% to 10%. This effectively equalises the value of the schemes and saves £1 billion per annum after two years.

The Financial Secretary to the Treasury, Victoria Atkins, told the House of Lords on 21 November that the government considers there is greater value from the RDEC scheme than from the SME scheme – and this was the driver of the changes, rather than the perception of possible SME scheme fraud (see

bit.ly/3GGeJfx).

Treasury officials told their lordships that the changes to the scheme were intended to maintain the overall value of R&D schemes at lower cost – and added that the government was likely to consult in 2023 on whether to merge the two R&D schemes. HMRC officials told the sub-committee that HMRC now receives 60,000 R&D claims worth less than £50,000 each, which puts a strain on compliance activities. The Department is also currently conducting eight criminal investigations.

Employer NIC

If the theme of the fiscal consolidation overall is freezing thresholds and allowances, no one can be surprised that the Employer NIC threshold will be frozen at the current level (£9,100) until April 2028, raising over £5 billion annually. The employment allowance remains unchanged at £5,000 annually.

Pillar II goes ahead

The government confirmed that it will go ahead with adopting the minimum tax on corporate profits measures in the G20/OECD-led Pillar II, with effect for accounting years starting on or after 31 December 2023. This will impose 15% minimum tax on the UK and overseas profits of large businesses and apparently raise £2 billion, based on HMRC estimates.

VAT frozen

The VAT registration threshold will be frozen at £85,000 at least until 31 March 2026. It is to be hoped that the government in future might consider some form of relief for businesses going just over the threshold – which currently acts as a limit on growth.

All in all, the Autumn Statement announced tax increases of over £88 billion over the next five years, on top of £21 billion announced after the Spring Statement.