Capital Relief

Share this article

Ian Mackie considers the capital tax reliefs on residential investments

The Government is under increasing pressure to improve the availability and quality of housing in the UK. Against this background, if you were to canvass opinion of property investors, or even tax professionals, most would probably say there is confusion surrounding the tax reliefs available to investors in residential property. This confusion arises from a combination of legislative complexity and the changing policy of successive governments.

This article looks at the different types of residential investment and the capital reliefs that may be available, SDLT, VAT and other taxes and reliefs associated with transactions are not discussed here.

What is residential for tax purposes?

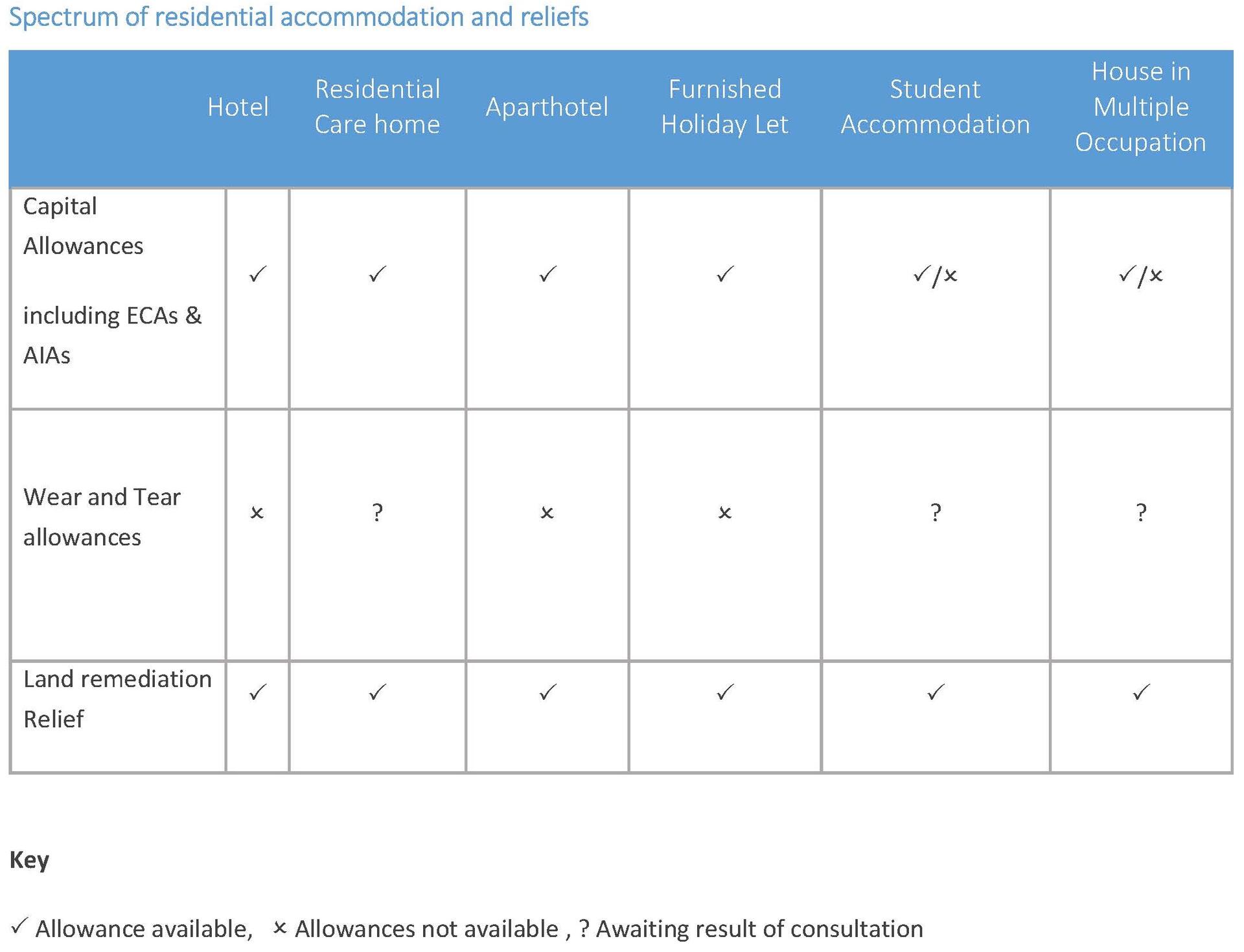

The table below summarises some of the incentives available for a range of property types, all of which could be described in one way or another as residential.

Capital Allowances - Residential accommodation

Plant and machinery allowances are not generally available on residential accommodation but what exactly is residential accommodation for capital allowances purposes? To help to understand this it is helpful to look at the legislation and HMRC’s manuals.

Legislation expressly prevents landlords from claiming capital allowances on expenditure on plant and machinery for use in a ‘dwelling –house’ as part of a UK property business .Specifically for CAA2001, Part 10 the term “dwelling-house” is given the same meaning as in the Rent Act 1977 (CAA2001 s531).

In 2001, Uratemp Ventures Ltd. V Collins [2001] UKHL 43, the court examined the Housing Act 1988 definition, found that a hotel room without cooking facilities comprised a dwelling house.

Some years later in 2008, because of the Uratemp Ventures ruling, HMRC changed their interpretation of the law to mean that in student accommodation, individual study bedrooms could comprise separate dwelling houses, leaving only the communal dining, kitchen and lounge areas not being part of the dwelling house.

The new guidance led to much confusion and as result, HMRC published further guidance in HMRC Brief 45/10 in 2010 which revised their definition and updated the Capital Allowances Manual at CAA11520 which now states that a ‘dwelling house is a building, or a part of a building; its distinctive characteristic is its ability to afford to those who use it the facilities required for day-to-day private domestic existence.’

It goes on to say that ‘….cluster flats or houses in multiple occupation that provide the facilities necessary for day-to-day domestic existence…..are dwelling houses. The common parts (for example stairs and lifts) of a building which contains two or more dwelling houses will not, however, comprise a dwelling house.’

Communal areas

Therefore Capital Allowances are available on plant and machinery and integral features in residential properties and including but not limited to:

- Lifts

- Heating and lighting in corridors and stairwells

- Fire alarms

- Access control

Currently, hotels, aparthotels and residential care homes are unaffected by the guidance in CA 11520 and capital allowances are available for qualifying expenditure on all parts of these properties.

Enhanced capital allowances (ECAs)

Where registered environmentally beneficial equipment is installed that qualifies for capital allowances a 100% first year allowance may be available through the enhanced capital allowances scheme.

Annual investment allowance (AIAs)

In addition to ECAs, investment is being encouraged by the recent changes to the Annual Investment Allowance. AIAs give businesses a 100% deduction from taxable profits for expenditure on machinery, equipment and plant.

The AIA limit has changed recently and has been announced as:

- 1 January 2013 to 31 March 2014 (*) – £250,000

- 1 April 2014 (*) to 31 December 2015 – £500,000

- 1 January 2016 onwards – £200,000

(*) For sole traders, partnerships and LLPs, the changeover dates are 5/6 April 2014.

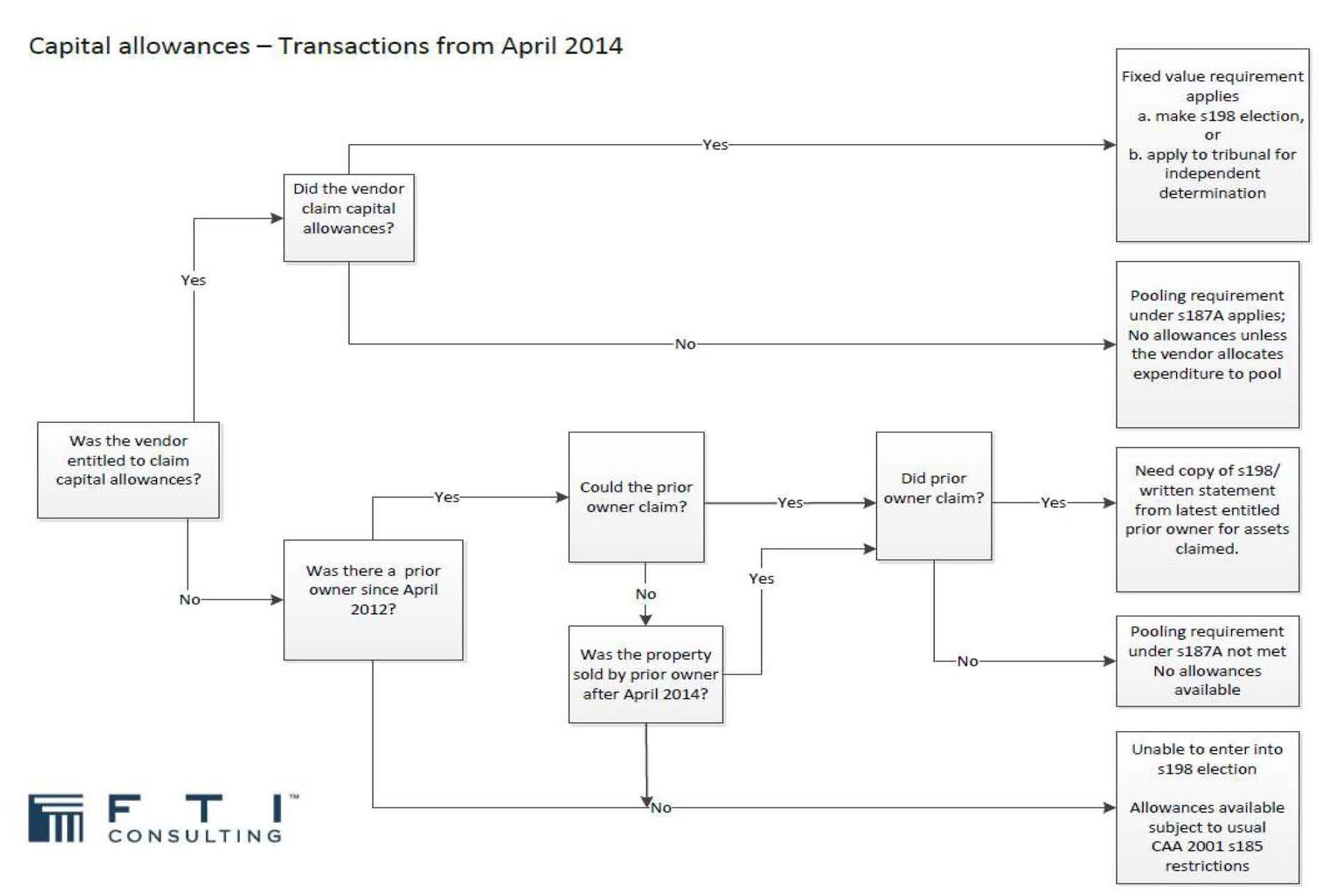

Capital allowances and fixtures - by way of a reminder

The Finance Act 2012 introduced major changes to the requirements for claiming capital allowances on fixtures when there is a sale and purchase of a property. The flowchart below highlights the key features of the regime from April 2014.

Wear and Tear allowances

Landlords of fully furnished residential properties can currently claim an allowance for notional wear and tear on furnishings equal to 10% of the net rent received. HMRC are currently consulting on the withdrawal of this allowance and are proposing a new relief on the actual cost of replacing furniture which will be available on unfurnished, part furnished and furnished properties, it is expected that this will apply from 2016 onwards. Under the new replacement furniture relief landlords of all residential dwelling houses, excluding Furnished Holiday Lettings (FHL), will be able to claim a deduction for items provided for the tenant’s use in the dwelling house. However there are concerns around transitional provisions and the narrow definitions proposed could exclude relief for anything that constitutes an improvement.

Land Remediation Relief (LRR)

Another often overlooked relief that is available is land remediation relief. In 2011 the Government decided not to withdraw this tax relief as it would risk "plans to support the housing and construction sectors through planning reforms and the release of large areas of publicly owned land for development".

Land Remediation Relief (“LRR”) is available as a 150% tax deduction in the period the expenditure is incurred for any costs in relation to the remediation of contaminated or derelict land.

Remediation of land in a contaminated state is defined as causing significant adverse impact on the health of humans or animals or damage to buildings and includes removal of asbestos and for derelict sites, the removal of building foundations.

Tax Credits

For loss-making companies the utilisation of capital allowances and land remediation relief to reduce tax paid is of no benefit. However these companies can claim a 19% or 16% cash tax credit respectively in return for surrendering any additional losses created by the relief, subject to certain conditions.

Summary

Residential development is a politically topical and an evolving area, with UK plc clearly committed to a significant expansion of the current housing stock. The difficulty for advisers lies in determining the true nature of any residential development and applying the correct tax treatment to maximise all reliefs.