Changing the scope

Share this article

Yvette Jacobs-Lee provides guidance on how the new interpretation of ‘ordinary shares’ and the Budget changes to the scope of entrepreneurs’ relief may affect your clients

Key Points

What is the issue?

In his October Budget, the Chancellor effectively narrowed the scope of entrepreneurs’ relief and its attractive 10% tax rate on eligible capital gains. This is coupled with a recent change in HMRC’s interpretation of the definition of ‘ordinary share capital’, which may bring some unexpected consequences.

What does it mean to me?

One thing is clear: these changes are both increasing the complexity around the availability of entrepreneurs’ relief, as well as calling into question if and when it will apply.

What can I take away?

Owner-managers of businesses and their advisers should be encouraged to consider the application of the rules sooner rather than later, particularly in light of the extension to the qualifying period from 12 months to two years for disposals on or after 6 April 2019.

In his October Budget, the Chancellor effectively narrowed the scope of entrepreneurs’ relief and its attractive 10% tax rate on eligible capital gains. This is coupled with a recent change in HMRC’s interpretation of the definition of ‘ordinary share capital’, which may bring some unexpected consequences.

The relief: a refresher

It’s one of the most talked about tax breaks for the business owner and is fraught with detail. Where it is available, entrepreneurs’ relief operates to reduce the rate of tax on up to £10 million (a lifetime limit) of gains on qualifying business disposals to 10% (rather than the standard 20%). Relief is available to individuals and trusts, but not companies. Eligible disposals comprise: a material disposal of business assets; a disposal associated with a relevant material disposal; and a disposal of trust business assets.

A disposal of shares or securities in a trading company will be considered a ‘material disposal of business assets’ where the shareholding meets the conditions to be treated as the investor’s ‘personal company’. The changes relate to the scope of the definition of a ‘personal company’.

What is a personal company? Up to 28 October 2018

The definition is set out at TCGA 1992 s 169S and refers to a company where:

- at least 5% of the ordinary share capital of which is held by the individual, and

- at least 5% of the voting rights in which are exercisable by the individual by virtue of that holding.

What is an ordinary share?

One of the problems that can arise is understanding what an ‘ordinary share’ is. This may seem obvious, but there is a legal definition for entrepreneurs’ relief purposes at ITA 2007 s 989:

‘Ordinary share capital’, in relation to a company, means all the company’s issued share capital (however described), other than capital the holders of which have a right to a dividend at a fixed rate but have no other right to share in the company’s profits.

So the name given to the share class is irrelevant; what is relevant is whether there is an entitlement to dividends at a ‘fixed rate’.

This leads to the next question as to what is a ‘fixed rate’. It has long been HMRC’s view that deferred shares with no right to a dividend are ordinary share capital. The rationale for this is that a right to nothing is not a fixed entitlement.

This view was confirmed by the Upper Tribunal in McQuillan v HMRC [2017] UKUT 344, where Mr and Mrs McQuillan were denied entrepreneurs’ relief on the sale of their sandwich shop business as a result of the large number of non-voting shares in issue with no right to dividends. In this case, the non-voting shares had arisen on capitalisation of an informal loan to the company, in respect of which it had always been understood by the parties that there was no right to dividends or ownership of the business.

HMRC has now agreed some further guidance as to what is and what is not ordinary share capital. The guidance has been published with permission by the CIOT and an updated version of the HMRC Company Taxation Manual is expected to follow shortly.

The guidance has thrown up some examples that may not be widely appreciated. For instance, it is HMRC’s view that a preference share with a fixed rate of dividend of say 10% that is cumulative is not ordinary share capital. This is not a particular surprise.

However, if a preference share has a fixed rate of dividend of 10% which is not cumulative, HMRC’s view is that this return is not fixed, as the dividend depends on the business’s results. Accordingly, preference shares in these circumstances are ordinary share capital.

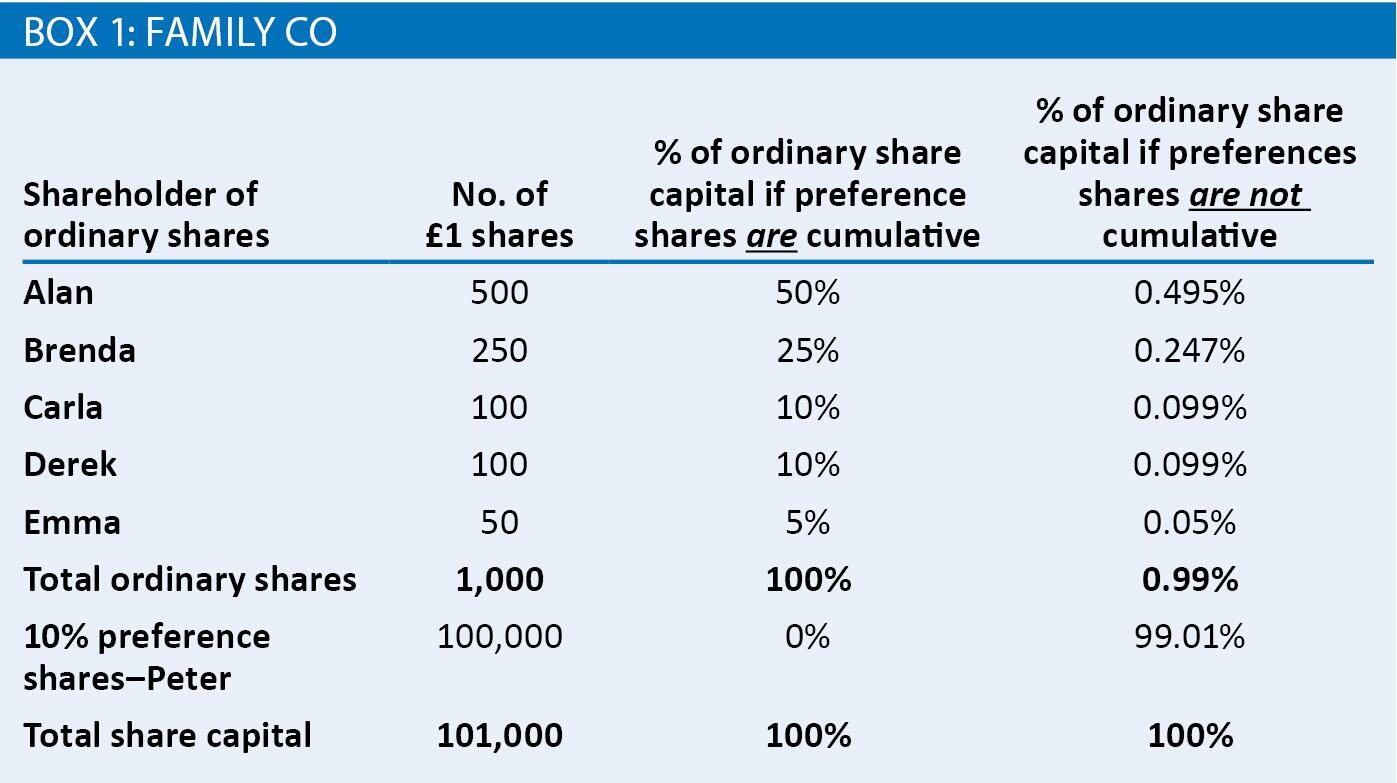

Example: Family Co

Preference shares in well-established owner-managed companies are common. Consider, for example, the generational family business where one side of the family takes a management backseat but takes a favoured investment return. Or the entrepreneur who has issued shares in exchange for external investment to take operations to the next level.

Depending on whether the preference shares are cumulative or non-cumulative, there could be drastically different results for the owner-manager, as shown in Box 1.

If the preference shares have cumulative dividend rights, shareholders A to E will qualify for entrepreneurs’ relief (assuming the other qualifying conditions are met), as they each own at least 5% of the ordinary share capital. If the dividend rights on the preference shares are not cumulative, they will be regarded as ordinary share capital and none of the shareholders A to E will qualify for entrepreneurs’ relief, as their interests are swamped by the preference shareholder and each of them owns less than 5% of the ordinary share capital.

The position could be improved by varying the rights attached to the preference shares, or perhaps repaying those shares, where the company funds allow. Certainly, shareholders in this situation need advice – and, following the Chancellor’s Budget announcements on 29 October 2018, they need it at least two years in advance of any planned sale or exit.

What is a personal company? From 29 October 2018

After continued speculation about whether entrepreneurs’ relief will be reduced or abolished, announced in the Budget was a change to the definition of a personal company in section 169S TCGA 1992. Legislation introduced by the Finance Bill 2018-19 will add two additional conditions to the definition, such that an individual must be beneficially entitled to:

‘(c) at least 5% of the company’s distributable profits, and

(d) at least 5% of its assets available to equity holders in a winding up.’ [To be calculated using balance sheet values].

The Budget briefing note states that this change is part of the government’s policy of supporting enterprise and that: ‘having such an interest is characteristic of true entrepreneurial activity (as distinct from simple investment or employment), so the measure ensures that allowable claims are limited to those which are within the spirit of the relief.’

Employee shareholders who have acquired their shares under an Enterprise Management Incentive can successfully side-step this new definition as they are not, by virtue of section 169I(7A) TCGA 1992, required to meet the definition of a personal company to benefit from entrepreneurs’ relief. But what of other routes to employee shareholdings? It is typical that shares in such circumstances will be awarded with restricted rights – and such restrictions may now mean a higher tax rate than intended on a future exit. Share awards that apply only to sale proceeds over a set ‘hurdle’ value could struggle to meet the 5% test.

For shares not acquired under EMI, it may be typical of a smaller owner-managed business that 5% of the share capital will naturally give corresponding rights to 5% of the voting rights, distributable profits and rights to assets on a winding up; but in more complex situations, this may not necessarily be the case. Typically, the holder of a preference share may only be entitled to redemption at par in the case of a sale or a winding up, for example. Such preference shares may now pass the first hurdle of the personal company definition with thanks to the new guidance discussed above, but would presumably fall foul of hurdle three or four.

Or perhaps not? Continuing the example above, it would follow that the availability of entrepreneurs’ relief will depend upon the eventual proportion assets available on a winding up represented by the preference shares throughout the qualifying period leading up to a sale. If the par value of the preference shares in issue is more than 5%, then entrepreneurs’ relief will be available; but if not, then the beneficial rate of capital gains tax will not apply. This unpredictable status is unlikely to be palatable to many shareholders in this position.

Conclusion

One thing is clear: these changes are both increasing the complexity around the availability of entrepreneurs’ relief, as well as calling into question if and when it will apply.

Owner-managers of businesses and their advisers should be encouraged to consider the application of the rules sooner rather than later, particularly in light of the extension to the qualifying period from 12 months to two years for disposals on or after 6 April 2019.