Chaos to order

Share this article

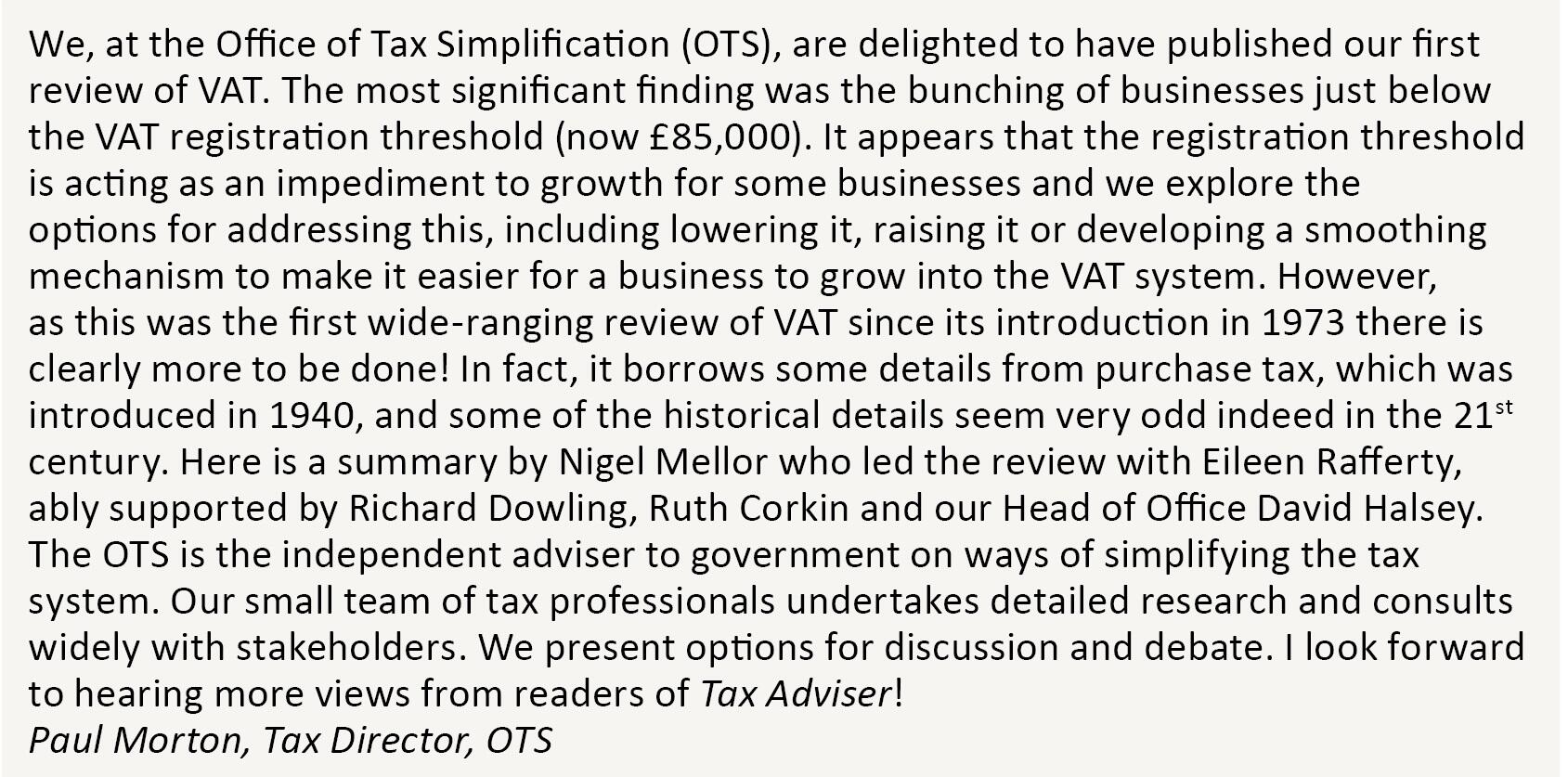

Nigel Mellor summarises the findings of the recent OTS report on VAT simplification

Key Points

What is the issue?

The OTS has published a report on the VAT system which makes 23 recommendations in relation to the VAT threshold, administration and technical issues

What does it mean for me?

If the Chancellor agrees with the recommendations, there are likely to be major changes to the VAT system in the future.

What can I take away?

It is commonly accepted that the VAT system is showing its age and simplifications are needed.

On 7 November 2107, the OTS laid before Parliament its final report on the UK VAT system. The report was the culmination of a review which has taken twelve months to research and is the product of over eighty meetings held with various parties throughout the UK. These included professional bodies (including the CIOT), trade associations and micro businesses through to global corporations. In addition, particularly towards the end of the review, the team worked closely with HM Treasury and HM Revenue and Customs.

The report contains 8 core recommendations and 15 additional ones, making 23 in all.

At the time of writing, we do not know whether the Chancellor will reply alongside the Budget, or shortly afterwards, but in any event his reply will be published on the OTS website as soon as we have it!

Broadly, the report (which runs to almost 80 pages) can be broken into three main areas; namely,

- The issues and impacts involved if the registration threshold were either higher or lower than it is at present;

- Administrative changes which could help businesses, advisers and HMRC better achieve their common aim of easing friction points in the system;

- The extent to which the definitions of the type of supply which are currently relieved from VAT create complexity for businesses and administration.

Core recommendations

Registration threshold

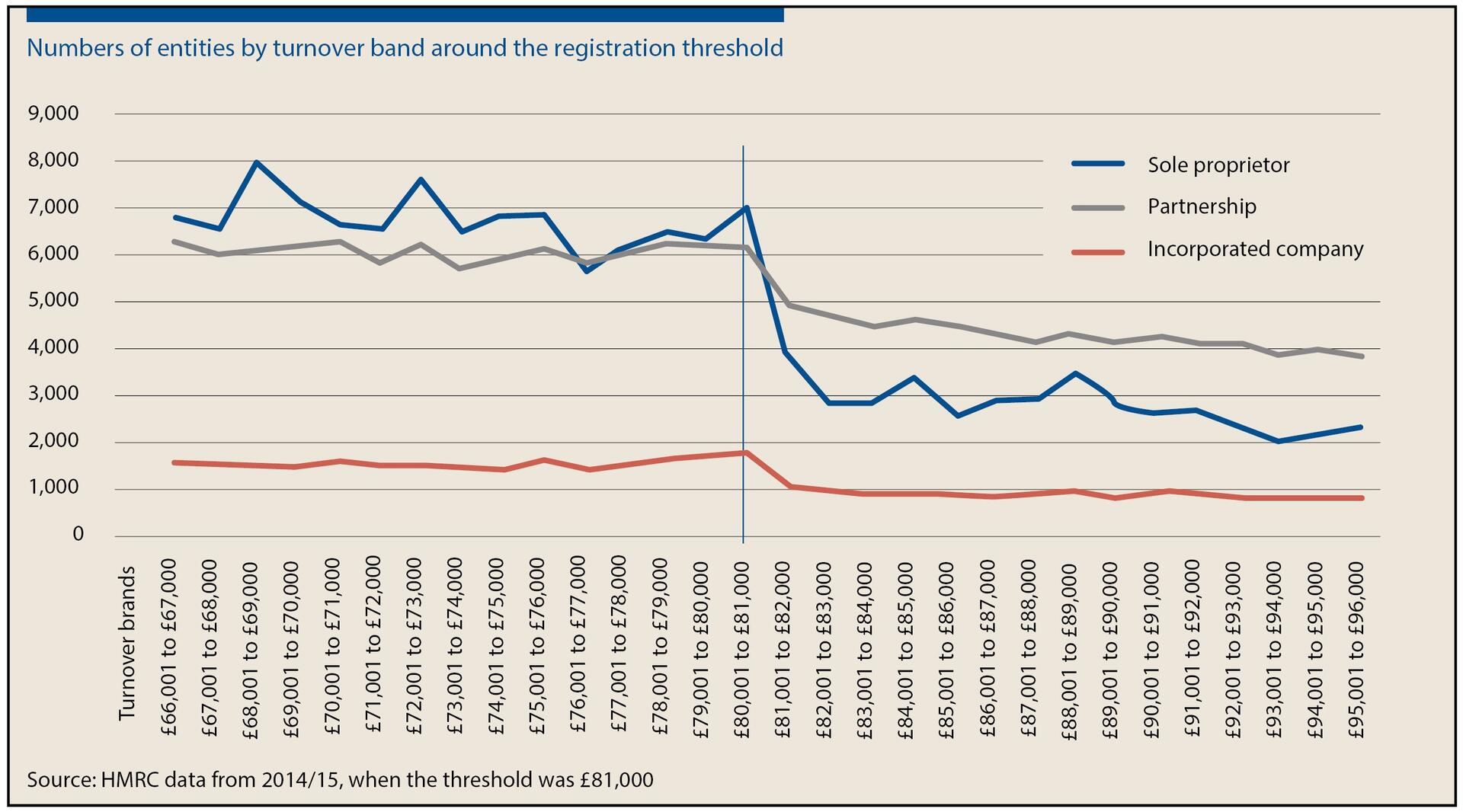

The report sets out in detail the issues which are likely to arise if the threshold were to be increased or lowered. The reason why this was considered in such detail is because there is clear evidence, from academic evidence and submissions made to the review, that the relatively high threshold is having a distortionary impact on business growth and activity. The graph below which was created using HMRC data clearly illustrates this issue.

Consequently, the first core recommendation is that the government should consider the level and design of the VAT registration threshold with a view to setting out a future direction of travel for the threshold, including consideration of the potential benefits of a smoothing mechanism. See figure 1.

Administrative changes

In our reviews of other taxes, practical administrative issues have frequently been identified as being one of the most important to users of the tax system and VAT is no different. Many contributors provided suggestions where improvements could make life easier for them.

The report includes extensive comment on the issues and as many of the submissions relate to guidance, the second core recommendation is that HMRC should improve the clarity of its guidance and its responsiveness to requests for rulings in areas of uncertainty.

A further core recommendation concerns the uncertainty and administrative costs for business relating to potential penalties when inaccuracies are voluntarily disclosed.

Technical issues

Multiple rates

Numerous articles have been written over the last 40 years on some of the absurdities which arise in the UK VAT system. The report identifies a few of them and comments that the boundaries between the current treatments standard rate, reduced rate, zero-rate or exempt are often a cause of complexity and represent an administrative burden.

The core recommendation here, unsurprisingly, is that HMRC and HMT should undertake a comprehensive review of the reduced rate, zero-rate and exemption schedules (working with the OTS).

Partial exemption

For many reasons, the partial exemption regime is now capturing many businesses that would not originally have been affected by it. This, partly because businesses are actively diversifying income streams which can frequently generate more exempt income but a major factor is the fact that the de minimis limits have not been increased for decades.

The core recommendation here is that the government should consider increasing the partial exemption de minimis limits in line with inflation, and explore alternative ways of removing the need for business incurring significant amounts of input tax to carry out partial exemption calculations.

Similarly, we received a great deal of feedback that businesses which need HMRC approval to operate a partial exemption special method expressed frustration that such approvals can take up to two years (or more).

Consequently, there is a core recommendation that HMRC should consider further ways to simplify partial exemption calculations and to improve the process of making and agreeing special method applications.

Capital goods scheme

There are numerous issues with the Capital Goods Scheme (CGS).

The primary one is that the threshold has not been raised since he scheme was introduced in 1990 so that consequently, many more transactions are now in the scheme than was originally intended.

In addition, the scheme also includes extensions and refurbishments of existing buildings so that businesses can have multiple CGS calculations running for varying amounts of time. This requires a lot of time and administration for what in practice seem to be relatively small adjustments. The same argument can also be made in relation to the threshold for computer equipment which now seems to be out dated because the price of technology has fallen so sharply since the threshold was originally set.

We have therefore recommended that the government should consider whether capital goods scheme categories other than for land and property are needed, and to review the land and property threshold.

Option to tax

One area of concern is that there is no universal record of who has opted in relation to interests in property and this can create uncertainty about whether a piece of land or a building has been opted and this frequently causes difficulties when a building is sold.

A core recommendation is that HMRC should review the current requirements for record keeping and the audit trail for options to tax, and the extent to which this might be handled on-line.

Additional recommendations

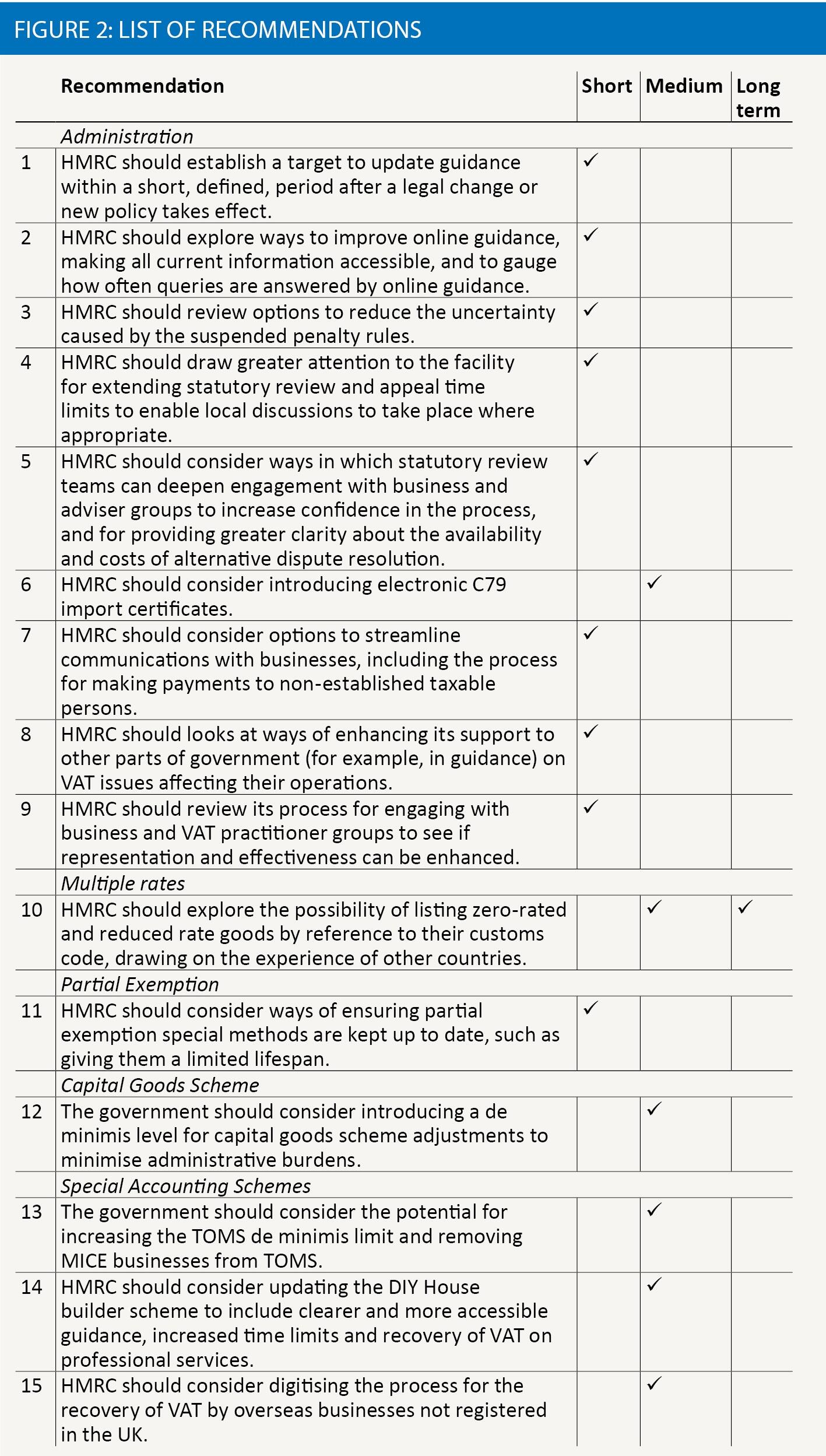

The report also sets out 15 other recommendations which are set out together with an indication as whether they should be short, medium or longer term objectives. See figure 2.

This article is a summary of the OTS’s report and was first published in Tax Journal. Reproduced with permission.