Collective gain

Share this article

Julie Butler explains the taxation considerations for investment clubs and other collective management schemes

Key Points

What is the issue?

With the rise in investment clubs and other collective management schemes, professional advisers are increasingly being approached to provide tax advice on these entities

What does it mean for me?

The approach required for investment clubs is often unique and requires attention to detail so that the correct gain is calculated

What can I take away?

A basic understanding of what investment clubs are, how they operate and what legal and taxation requirements a professional adviser may come into contact with when acting for such an entity

Collective investment schemes have operated in the UK since the early 1900s. The basic premise then remains true today: that a group of individuals pool resources to reduce risk, combine their knowledge and increase buying power. In an age of austerity, this pooling has become an attractive alternative to running an investment project single-handedly. This, coupled with the strong gains in the stock market since 2013, has attracted new investors wanting to share the responsibility of investment ownership. Professional advisers are often turned to for advice on issues from administrative and legal process to taxation implications.

Most investment clubs focus on the stock market, but others look to property, foreign exchange dealing and even rare artworks.

Similarly, other collective management schemes, such as racehorse share syndicates and flat management companies, are run on that premise of pooling resources and knowledge. However, many of these do without a profit-seeking motive and therefore, some may argue, generally fall outside the UK tax system. Stock market investment clubs, however, are different.

Day-to-day club operations and management

Club members vary significantly, with people taking part from all walks of life and being allocated roles depending on their personal strengths and weaknesses. Usually, the club will be managed by a constitution because a set of operational rules is vital for the entity’s long-term success. These rules will be used to allow members to join and leave, settle disputes, choose an investment strategy and set a stop-loss to ensure the club doesn’t lose large quantities of funds if an investment fails.

Members usually pay a regular ‘subscription’ into the entity, which may vary depending on individual circumstances, in return for ‘units’ issued by the investment club. This means that most clubs have bank and brokerage accounts through which to manage these funds. Members can also buy additional units or redeem present holdings while the club’s exists. Typically, clubs meet monthly to make investment decisions, review performance and perhaps trade club units.

Management roles involved within an investment club are likely to include:

- chair: coordinates the club members, and ensures the constitution is implemented fully;

- treasurer: manages monthly member subscriptions and withdrawals, manages unit valuations, is responsible for bookkeeping and submitting each year an accurate form 185 to HMRC and club members; and

- secretary: keeps a record of meeting minutes and general club administration.

General taxation implications:an overview

After an investment club has been formed, HMRC must be notified immediately. HMRC should invite all clubs to the standard terms of agreement and provide assistance in setting these up. From this point, all club undertakings are taxable. Subject to common misconception, investment clubs do not pay corporation tax because they are not normally an incorporated entity. Instead, at the end of the financial year, the club treasurer must issue each member with an investment club certificate, HMRC form 185, which details his or her proportion of the interest and dividend income earned over the previous 12 months, which will be added to the individual income tax computation, and any capital gain on loss on the shares. Sales and transfers of ownership ‘units’ will also fall within the scope of CGT, a feature often overlooked by club members.

If the total capital gain is more than £11,100, the current exemption limit, or if proceeds exceed four times the annual exemption, this figure too will have to be added to the individual tax return for that tax year, alongside the income tax entry for dividend income. Investment club capital gains on shares and units can be tricky to calculate given there could be hundreds of transactions in a tax year, and it is important to follow the correct processes to compute the right gain per club member, and therefore what to declare on form 185.

Capital gains and investment clubs: complicated apportion of gains

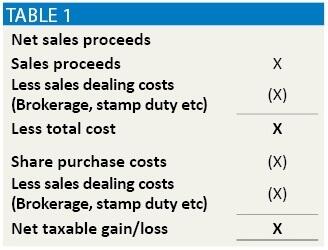

The capital gain on the sale of shares owned by an investment club is, in theory, easy to calculate because the computation is produced in the normal way in Table 1.

Each capital gain, once calculated, must then be apportioned to members depending on their unit holdings at that time. It is here that things become complicated. Members’ holdings vary depending on their current rate of subscriptions, any additional units that have been purchased or sold, and the current value of other unsold investments. It is therefore vital for the treasurer or management committee to keep on top of who owns what, when. This is the first issue that can make a straightforward gain more complicated, particularly when transactions of units are unrestricted.

Some clubs adopt the strategy of only counting subscriptions and allowing redemptions and purchases of club units at each meeting, so that any apportionment for share sales in the intervening period can be calculated on the basis of the holdings at the end of the previous meeting. In other clubs, the administrative burden is a lot higher because percentage allocations need to be calculated at the precise moment shares are sold if units in issue have altered between meetings. This can cause a major difficulty for the professional adviser because multiple capital gains in the same month may have to be divided according to two or more ownership structures. Advisers will, however, be thankful that indexation allowance and taper relief have long since been abolished, which removes the potential to have a different rate of taper relief applying to each shareholding.

Once the capital gains have been apportioned between each member, the treasurer will fill out form 185 on behalf of each individual unit holder and issue this for each tax year, ready to be included on their tax return.

Redemption of ownership units: another CGT headache

There are two options when calculating capital gains on redemption of shares. If a member is exiting the club entirely, the calculation is significantly different from redemption of one share.

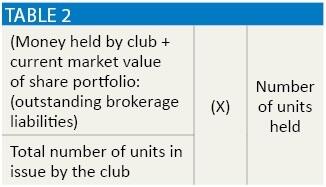

On leaving an investment club, it is necessary to calculate the gain or loss from the member’s overall holding. In most cases, the club will be continuing, and will therefore redeem the units at their individual value, multiplied by the number of units held. This is worked out using the formula in Table 2.

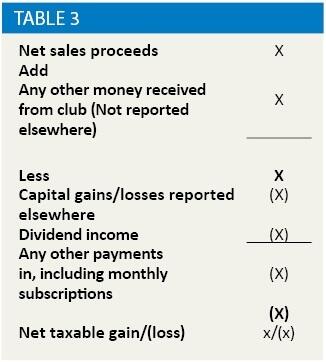

This gives a total value at which to redeem the units. On receiving the net proceeds from this transaction, the member can then calculate his capital gain on the transaction. This, of course, excludes any dividend or interest income, or any capital gains that have already been accounted for.

The computation is therefore as set out in Table 3.

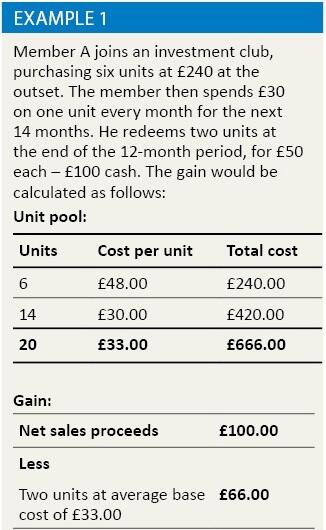

On transferring one unit to another member, or redeeming one unit within the club itself, HMRC deem an individual to have ‘sold’ their units. The tax inspectorate advises that individuals need to declare these unit gains alongside their form 185 certificate returns in the year in which they occur to avoid complications later. The unit value at the date of redemption will be calculated as before, which should then form the basis of the sales or the value of the transfer transaction. The base cost, for CGT purposes, will be computed using the pooling technique to value the member’s holdings against the total amount invested in the club as a whole – see Example 1.

Conclusion

Investment clubs are seemingly on the rise, with more individuals looking to spread financial risk and pool knowledge to create a new investment strategy to generate future returns. In some circles the sums invested in the clubs has increased significantly. Such clubs do not fall under the usual partnership or limited company trading vehicles, but are instead taxed on an individual member basis. So professional advisers engaging in work with these entities must be aware of what administration must be filed with HMRC each year, and also how to compute and proportion capital gains on share sales, and redemption values on unit trades within the club. Such calculations can be messy and complicated, and the investment club treasurer, be they experienced or amateur, may need significant help.