Competitive advantage

Share this article

Stephen Hemmings and Will Sweeney consider how competitive the UK’s tax system really is, compared to others

Key Points

What is the issue?

With tax becoming ever more global under the auspices of initiatives such as the Base Erosion and Profit Shifting project adopted by 124 countries, what advantages does the UK offer the multinational business?

What does it mean to me?

The UK, however, has so far managed to maintain a competitive position, with a low tax rate, generous, well-targeted reliefs and a stable system.

What can I take away?

Post Brexit, the challenge for the Government will be to see if it can sustain this delicate balance, between the need to prevent tax avoidance while continuing to build on the attractiveness of the UK as a destination for investment.

The Government makes much of the UK having the most competitive tax system in the G20, but how does that really stack up? With tax becoming ever more global under the auspices of initiatives such as the Base Erosion and Profit Shifting (BEPS) project adopted by 124 countries, what advantages does the UK offer the multinational business?

Well firstly, we should look at the impact that internationally agreed frameworks have had on UK law. A key consideration has been the UK’s membership of the EU. Direct taxation is generally a matter for Member States. However, the EU has unanimously agreed a number of tax Directives, which apply in all Member States. Additionally, domestic law must not infringe the fundamental freedoms set out in the European treaties. For Indirect taxes, such as VAT, the link is even clearer, as it is agreed on an EU wide basis, with EU directives implemented through UK VAT law.

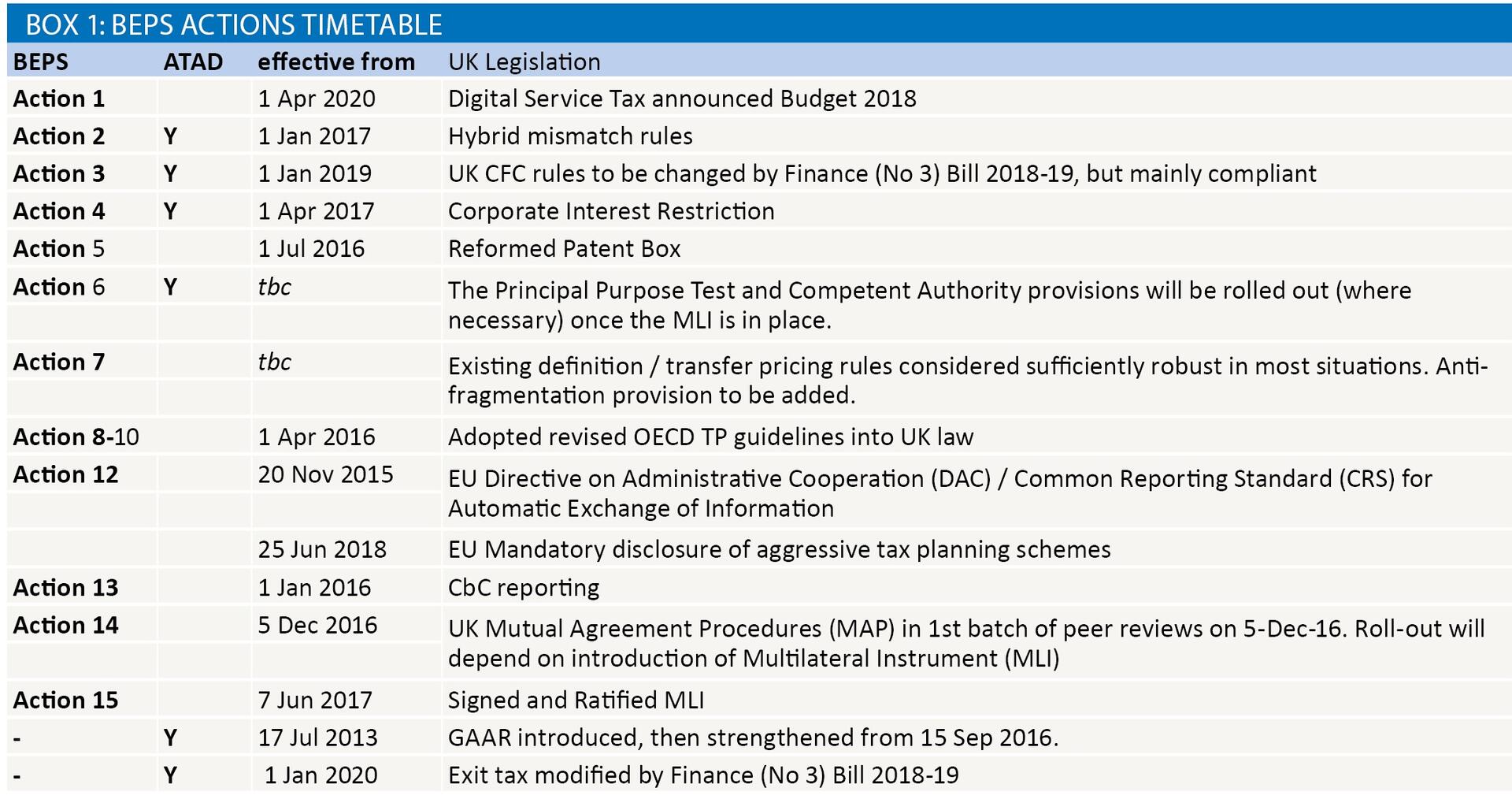

Since its inception, the UK has been an active supporter of the BEPS project and among the first to implement many measures highlighted by each of the 15 BEPS actions. Since 2016, this has been reinforced by the BEPS project’s related offshoot, the EU’s Anti-Tax Avoidance Directives (ATAD), which have implemented Actions 2 (hybrid mismatches), 4 (interest restrictions) and 3 (controlled foreign companies or CFCs), as well as requiring further action in relation to a general anti-avoidance rule (GAAR) and Exit Taxation. Box 1 shows the impact that these projects have had on the UK tax landscape over the last four years.

The UK will not be alone in experiencing this impact as all EU states had to implement the ATADs requirements by 31 December 2018, ensuring a prompt and consistent approach by members against tax avoidance. The exception to this is for exit taxes, where members are allowed an extra year, and for interest restrictions, where states that have domestic, targeted rules that have equal effect are permitted a transitional period up to 1 January 2024.

For many of the leading EU countries, the recent legislative effort has therefore focussed on the implementation of ATAD measures. The main drive of these actions is to ensure that business profits cannot avoid being taxed somewhere in the value chain.

However, as noted above, provided the profits that fall to be taxed in each state are calculated in accordance with the underlying framework and treaties, the UK is free to set its own domestic tax laws, and this does present an opportunity to claim a comparative advantage over other states.

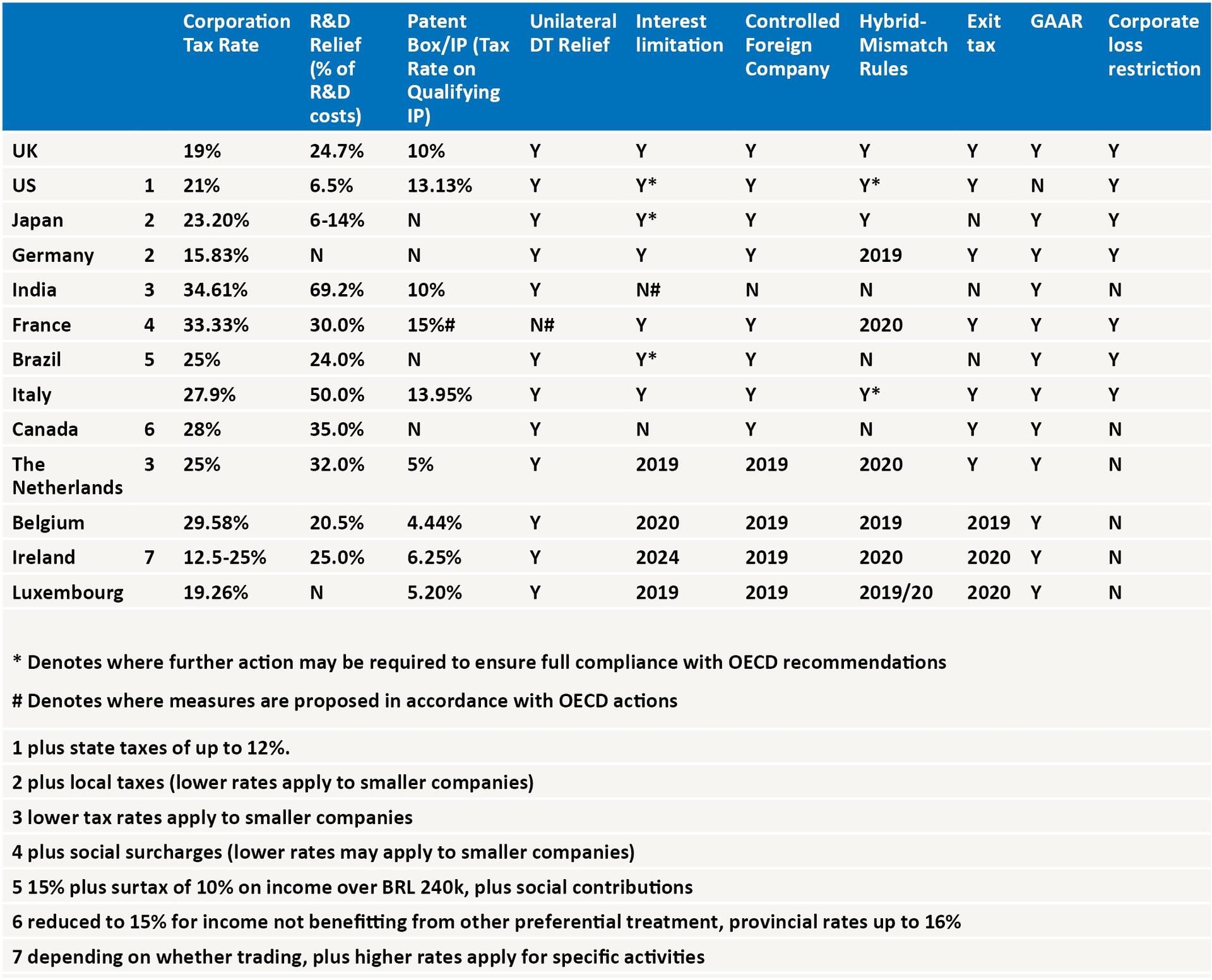

Table 2 shows that the UK baseline corporate tax rate is lower than many of its competitors and, when account is taken of state taxes, is the lowest in the G20. Being competitive is not solely the preserve of a low tax rate, though, and the UK benefits hugely from its open economy, skilled labour force and connected infrastructure. This article is about tax however, and even here there are many other factors that will influence multinational companies.

Individual states are not precluded from offering specific tax reliefs providing they comply with the rules of the BEPS Inclusive Framework, EU harmful tax competition rules and EU competition law. This is particularly useful to innovative firms in the UK, where R&D relief and Patent Box incentivise the development and monetisation of intellectual property and a range of investment and venture capital reliefs favour knowledge intensive businesses.

Other countries, such as the US, or the Netherlands also have such rules so how do the headline rates for R&D relief and patent box compare? Table 2 illustrates rates across several of the UK’s competitors, although should be viewed carefully, as with all tax law, as variations in the qualifying criteria and design of the scheme (for example, whether a tax credit or super-deduction is available) make it hard to directly compare schemes.

Tax reliefs do not tell the whole story of course, with numerous surveys in recent years reinforcing the value companies place on stability and predictability in tax systems. This has made the last few years challenging as the BEPS action plans are complex and interdependent and, in many cases, have led to significant changes in domestic tax systems. However now that both the BEPS proposals, and individual EU countries proposals for implementing the enhanced ATAD requirements are largely finalised, we are starting to gain a clearer picture of how countries will apply them. The early adoption and clear statements of intent issued by the UK government have been helpful to UK-based companies in determining exactly how their tax position will be affected. Now that the majority of measures have been implemented, the UK does not expect to make any further significant changes.

Although few major legislative changes are expected, the BEPS Multilateral Convention is key to implementing the tax-treaty related measures developed through the BEPS Project in current bilateral treaties in an efficient manner. The UK already has Principal Purpose Test clauses in some treaties (which limit unintended treaty benefits). However, the broader scope of the BEPS measures to counter treaty shopping and add much better dispute resolution procedures will have an important impact. The Multilateral Convention has a range of options in it, and applies only when both parties to a treaty have ratified the Convention. Taxpayers and advisers should therefore take care to ensure that they are considering the latest version of a relevant treaty before determining the tax treatment of a transaction.

It can be seen from Table 2 that recommendations such as Controlled Foreign Company provisions, that seek to impute a tax charge on profits artificially diverted to low tax jurisdictions, have been widely implemented as such measures were widely in evidence prior to BEPS. Adoption of the corporate interest limitation (action 4) has been more mixed, reflecting the wider range of interest tax treatment prior to BEPS. The UK is perhaps unusual in this respect, in being an early adopter of these rules despite having had generous rules in relation to tax relief on corporate interest until 1 April 2017.

Progress among EU countries in adopting the BEPS recommendations has been accelerated by ATAD, but there is an increasing appetite for international cooperation in confronting tax avoidance . This saw the US strengthen its anti-hybrid rules to counter potential tax avoidance in relation to intragroup interest and royalty payments as part of US tax reform and France’s 2019 Finance Bill has set out long awaited proposals to modify its patent box regime to ensure compliance with Action 5.

As we are all too well aware at present, the fly in the ointment for the UK is the uncertainty over Brexit. While many areas of EU law have been written into UK law and so would not be expected to change immediately, others rely on EU Directives. For example, if we were to leave the EU under a ‘no-deal’ arrangement, the EU Parent-Subsidiary Directive and Interest-Royalty Directive would cease to apply to the UK from 11pm on 29 March 2019. Any European groups relying on these would then need to consider withholding taxes, and whether they can be mitigated through bilateral tax treaties.

A further issue for the UK, as it is for all major countries, is the taxation of the Digital Economy, and this will remain a challenge to resolve in coming years. In the recent Budget, the Chancellor announced that the UK would go it alone with a revenue based Digital Services Tax on companies with relevant turnover over £500m on its UK revenues above £25m from 1 April 2020 unless a multilateral solution can be agreed. Similar proposals have been tabled by the EU, and unilaterally by several governments, including Italy, India and Australia, to the displeasure of the US which regards the digital economy as indivisible from the wider economy. The EU has also suggested a Significant Digital Presence tax, which mirrors OECD thinking on the concept of a digital permanent establishment, however this would require significant renegotiation of tax treaties and so we are unlikely to see it soon.

Overall then, we can see that the tax systems of the world’s major economies are more similar than they are different, and are only likely to grow more similar as they work together to eliminate tax avoidance, and compete to attract investors and multinational businesses. There are outliers within this framework, such as the Irish tax system with its corporate tax rate of 12.5% and generous IP rules that have attracted considerable external investment – along with high levels of consternation from the European Commission – but these are an exception.

The UK, however, has so far managed to maintain a competitive position, with a low tax rate, generous, well-targeted reliefs and a stable system. Post Brexit, the challenge for the Government will be to see if it can sustain this delicate balance, between the need to prevent tax avoidance while continuing to build on the attractiveness of the UK as a destination for investment.