A complex solution

Share this article

Harriet Brown examines the underlying principles to the main residence nil rate band, and the issues which may arise when a main residence is inherited

Key Points

What is the issue?

The new provisions added to Inheritance Tax Act 1984 introduces the main residence nil rate band.

What does it mean to me?

Understanding the new nil rate band is essential for advising all clients that have real property.

What can I take away?

An overview of the principles of the main residence nil rate band and the issues which may arise when a claim is made.

The inheritance tax main residence nil rate band (RNRB) is a complex solution to what was a relatively straightforward problem. For some time, there had been calls to increase the threshold from £325,000. Instead of increasing it for everybody the RNRB gives an additional nil rate amount when an individual’s main residence is passed to their direct descendants on death. This has given rise to some complex provisions and, unfortunately, a complex calculation.

However, the underlying principles are straightforward. The RNRB was introduced by the Finance Act 2015 (FA 2015) – which adds new provisions to the Inheritance Tax Act 1984 (IHTA), but will apply to deaths on or after 6 April 2017.

The basics

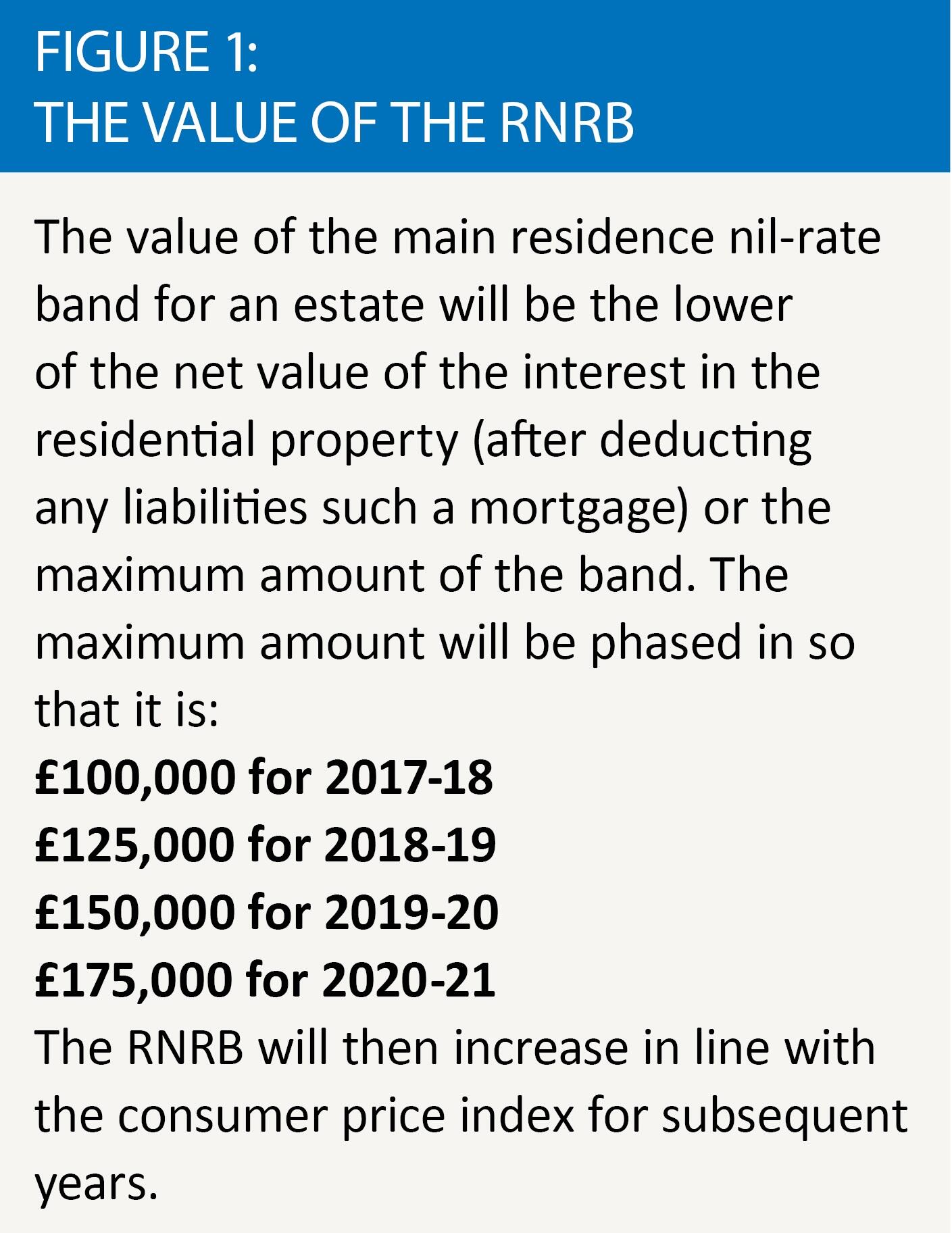

The RNRB provides for an additional main residence nil rate band for an estate if the deceased’s interest in a property, which has been their residence and is included in their estate, is left to one or more direct descendants. The RNRB is being phased in as set out in figure 1.

The qualifying residential interest will be limited to one property but personal representatives will be able to nominate which should qualify if there is more than one in the estate. A property that was never a residence of the deceased, such as a buy-to-let, will not qualify.

A direct descendant will be a child (including a stepchild, adopted child or foster child) of the deceased and their lineal descendants.

A claim will have to be made on the death of a person’s surviving spouse or civil partner to transfer any unused proportion of the additional nil rate band unused by the person on their death in the same way that the existing nil rate band can be transferred.

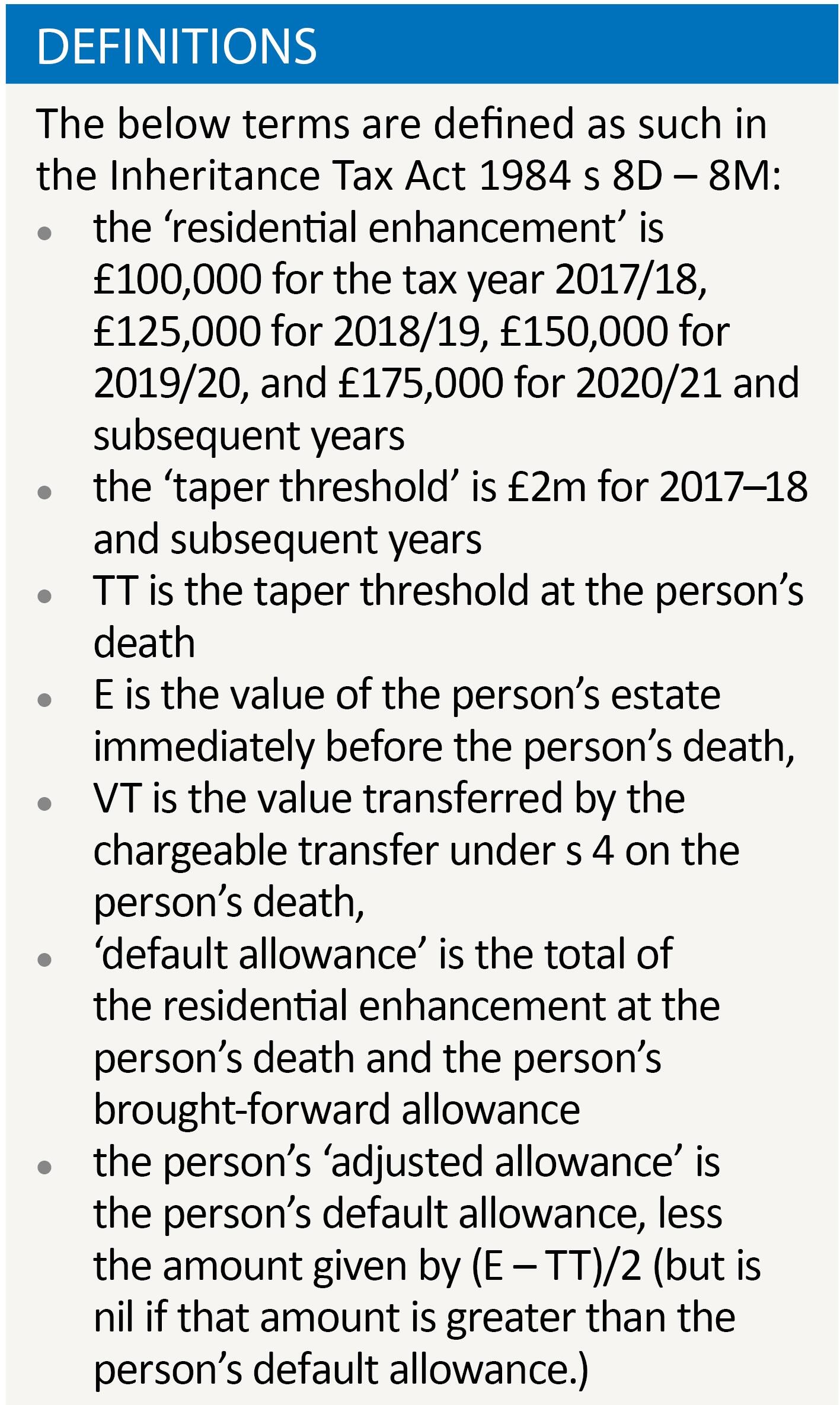

If the net value of the estate (after deducting any liabilities but before reliefs and exemptions) is above £2m, the additional nil rate band will be tapered away by £1 for every £2 by which the net value exceeds that amount. The taper threshold at which the additional nil rate band is gradually withdrawn will also rise in line with the consumer price index from 2021-22. Therefore, estates over a particular value will derive no benefit from the RNRB.

As well as introducing the RNRB, FA 2015 extended the current freeze of the nil rate band at £325,000 until the end of 2020/21.

The relief

IHTA s 8D provides that the (1) Subsections (2) and (3) apply for the purpose of calculating the charge to tax under s 4 if the person dies on or after 6 April 2017. It should be remembered that the relief applies only on death, not to failed potentially exempt lifetime transfers.

The actual relief is also found in IHTA 1984 s 8D. This provides that, if the person’s residence nil rate amount is greater than nil, the portion of VT that does not exceed the person’s residence nil rate amount is charged at 0%. In relation to the interaction between the normal NRB and the RNRB, the latter will be used first.

RNRBs are transferable between spouses, although a claim must be made within two years of the death. So, for spouses, the effective maximum reliefs are: 2017/18: £200k (£80k IHT saving); 2018/19: £250k (£100k IHT saving); 2019/20: £300k (£120k IHT saving); and 2020/21: £350k (£140k IHT saving).

The residence nil rate amount

The provisions for these in IHTA are complex. In short they boil down to the following:

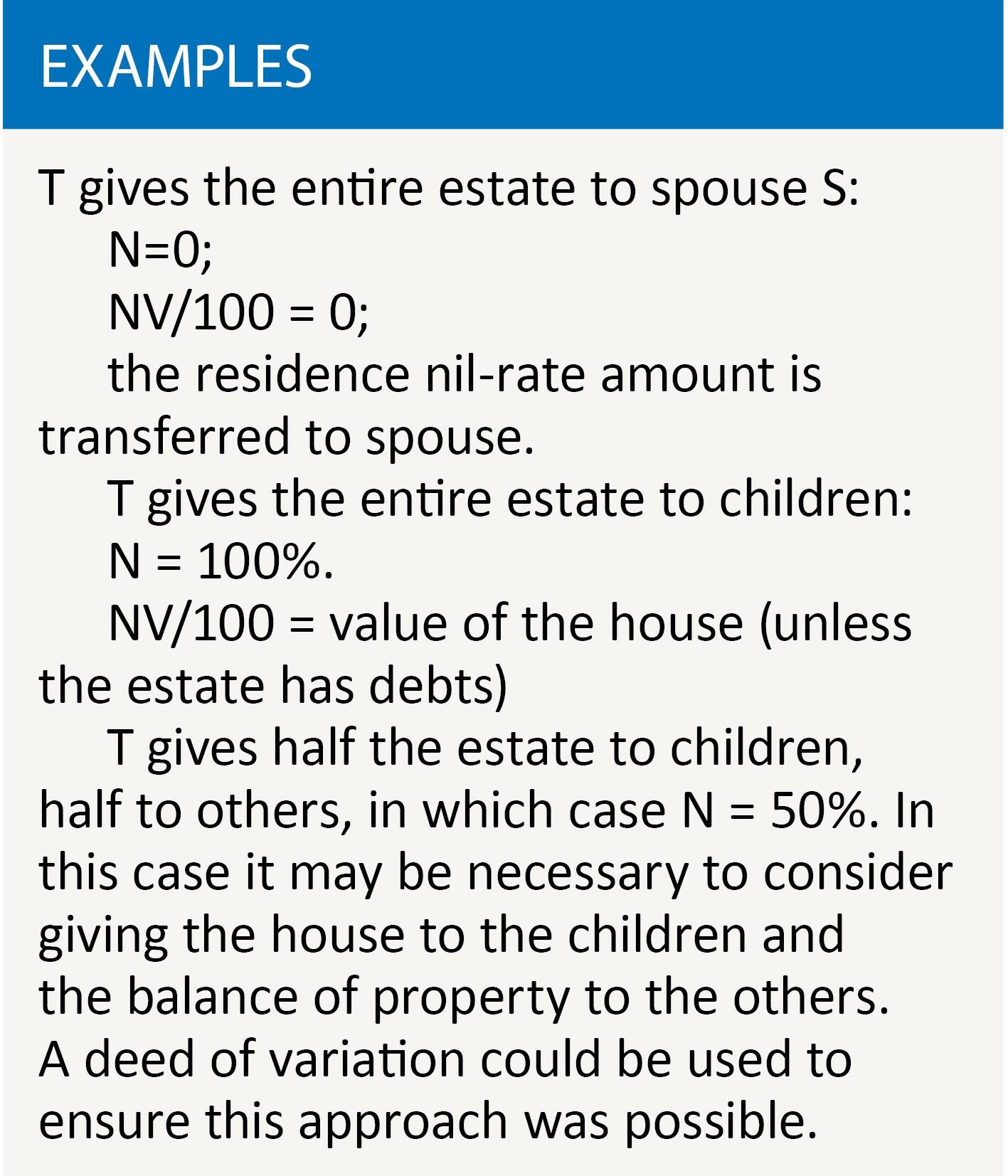

- ascertain N% (where N% is the percentage of the interest closely inherited – N is a number between 0 and 100;

- ascertain the value transferred;

- ascertain the value of residential interest; and

- ascertain the value transferred attributable to the interest. See the examples.

Qualifying residential interest

This is defined as interest in a dwelling house that has been the person’s residence at a time when the person’s estate included that, or any other, interest in it. If two properties meet the requirements, an election may be made.

On whether something is inherited IHTA 1984 s 8J provides that, if there is a disposition of property to a person, they inherit it. There are additional provisions that deal with property subject to settlement. Something is closely inherited if it is inherited by one of the following:

- a lineal descendant of D;

- a person who, at the time of D’s death, is the spouse or civil partner of a lineal descendant of D; or

- a person who at the time of the death of a lineal descendant of D who died no later than D was the spouse or civil partner of the lineal descendant, and has not, in the period beginning with the lineal descendant’s death and ending with D’s death, become anyone’s spouse or civil partner.

For these purposes stepchildren are treated as children.

Downsizing relief

FB 2016 provides a downsizing relief. This is the mechanism for ensuring that, when part of the RNRB is lost because the deceased had downsized to a less valuable residence or had ceased to own a residence on or after 8 July 2015, that part may still be available. This is on the proviso that the deceased left that smaller residence, or assets of equivalent value, to direct descendants.

FB 2016 will add new sections to IHTA 1984 most importantly ss 8FA-8FE. Much of the content of the provisions is in order to calculate the ‘right’ proportion of NRNB that is assigned in relation to the downsized property.

IHTA 1984 s 8FA will apply if a person has downsized from a more valuable residence and there is a less valuable one left in the estate on death. It gives the conditions that have to be met for an estate to be entitled to the increased amount of the residence nil rate band (downsizing addition) in these circumstances and how that amount is calculated. Subsection (1) provides that the downsizing addition will be taken into account when calculating the amount of the residence nil rate band if all the conditions in this section are met, giving the entitlement to the downsizing addition.

The provisos are:

- Condition A: there is a residence in the estate on death which qualifies for the residence nil rate band (a qualifying residential interest) but the full amount is not due because the value of the residence, or the proportion inherited by direct descendants (i.e. closely inherited), is below the maximum residence nil rate band available for that person, or there is a residence in the estate on death but none of it is closely inherited and the value of the residence is less than the maximum residence nil rate band available for that person.

- Condition B: the value transferred by the chargeable transfer on death (VT) is more than the value of the residence (the person’s qualifying residential interest).

- Condition C: the person previously had a residence that could have qualified for the residence nil rate band (the qualifying former residential interest).

- Condition D: the value of the former residence has to be more than the chargeable value of the residence in the estate at death.

- Condition E: at least some of the other assets in the estate (the remainder) must be inherited by direct descendants (closely inherited).

- Condition F: a claim is made for the downsizing addition.

The value of the downsizing addition is equal to the lost residence nil rate band (the lost relievable amount) as a result of the downsizing move. However, the amount is limited to the value of other assets, or proportion of that value, which is closely inherited.

Section 8FB will apply when a person no longer owns a residence so that there is no residence in the estate on death. It sets out the qualifying conditions for an estate to be entitled to the downsizing addition in these circumstances and how that amount is calculated. If there is no residence in the estate the conditions for the downsizing relief are:

- Condition G: there is no residence in a person’s estate at the date of death.

- Condition H: the value transferred by the chargeable transfer on death (VT) has to be greater than nil.

- Condition I: the person previously had a residence that could have qualified for the residence nil rate band (the qualifying former residential interest).

- Condition J: at least some of the other assets in the estate are inherited by direct descendants (closely inherited).

- Condition K: a claim has to be made for the downsizing addition.

The amount of the downsizing relief is equal to the lost residence nil rate band (the lost relievable amount) as a result of disposing of the residence, which is calculated in accordance with IHTA 1984 s 8FE. The amount is limited to the value of other assets, or proportion of that value, which is closely inherited.

Conclusions

The RNRB can be seen as a welcome addition for inheritance tax relief. It is, however, complex and will involve more difficult calculations and further claims.