COP 9 investigations: suspected tax fraud

Share this article

As HMRC opened 417 COP 9 investigations in the year to March 2023, we examine what is involved for taxpayers suspected of committing tax fraud.

Key Points

What is the issue?

A COP 9 investigation is opened where HMRC suspects taxpayers of committing tax fraud.

What does it mean for me?

Following the receipt of the detailed disclosure, there are usually further discussions and negotiations with HMRC to finalise the technical detail and agree the amount of tax due, which will go back up to 20 years where there has been deliberate behaviour.

What can I take away?

An attitude of collaboration and co-operation is the best way to ensure the maximum reduction in penalties.

The latest figures for serious civil tax investigations show HMRC’s continued action against potential tax fraud. In the year to 31 March 2023, HMRC opened a total of 1,091 Code of Practice (COP) investigations, split between 674 COP 8 and 417 COP 9 investigations. As at the same date, HMRC had a total of 3,300 of these COP 8 and COP 9 investigations under way. For the investigations that closed during the same year, COP 9 investigations generated £89 million for HMRC and COP 8 investigations generated £72.4 million.

A COP 8 investigation is launched where HMRC suspects a taxpayer of artificially lowering their tax bills through the use of tax avoidance schemes; whereas a COP 9 investigation is opened for taxpayers suspected of committing tax fraud.

Contractual Disclosure Facility

Where HMRC launches a COP 9 investigation, it will send the taxpayer an offer to participate in the Contractual Disclosure Facility. If the taxpayer accepts this offer, they must make an admission of all losses of tax and duty brought about by their deliberate conduct and provide an outline disclosure.

This outline must give details of the fraud, the period over which it took place and an estimate of the amounts involved, alongside all other irregularities in their tax affairs, including those that are not deliberate.

Where the taxpayer meets all the terms of the Contractual Disclosure Facility, HMRC commits not to pursue a criminal investigation against the taxpayer. In order to maintain this protection from prosecution, the taxpayer is expected to be open and honest and make a full disclosure. Where HMRC finds that there has not been absolute candour, a criminal investigation becomes much more likely.

When HMRC receives the outline disclosure, the relevant officer will then proceed to investigate the information provided, comparing it against the records it already holds (which will usually be the records that triggered the suspicion in the first place). The taxpayer is also usually interviewed face to face. Finally, the taxpayer produces a detailed disclosure report, usually with the support of professional advisers, to a timetable that must be agreed with HMRC.

Penalties

Following the receipt of the detailed disclosure, there are usually further discussions and negotiations with HMRC to finalise the technical detail and agree the amount of tax due, which will go back up to 20 years where there has been deliberate behaviour. Once the amount of tax has been settled, the penalties will also need to be agreed.

The taxpayer will be expected to sign a contract settlement called a Certificate of Full Disclosure and agree to pay the tax, interest and penalty due to conclude the investigation.

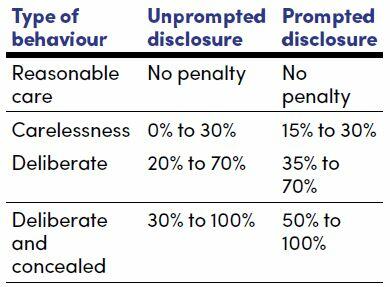

Penalties for inaccuracy are based on the behaviour of the taxpayer and whether the disclosure is prompted or unprompted. A disclosure will be unprompted where the taxpayer tells HMRC about an inaccuracy before they have any reason to believe that HMRC has or is about to discover the inaccuracy.

The following table shows the penalty ranges:

If the matter involves offshore liabilities, the penalty can be as high as 200%. This percentage is applied to the lost revenue that has arisen from the inaccuracy.

Taxpayers can seek to obtain penalties at the lower end of these ranges through the timing and quality of their disclosure. The lowest end of the range is available to taxpayers who make an unprompted full disclosure and then co‑operate fully with HMRC’s investigation. In a COP 9 investigation, this is only likely where the taxpayer has voluntarily made a disclosure before any involvement from HMRC. However, taxpayers that are brought into the investigation by HMRC can still secure lower penalties by ensuring that their disclosure is complete and they assist HMRC to quantify the under-assessment and provide access to their records.

Assisting in the investigation

Tax advisers who are supporting taxpayers with a COP 9 investigation should ensure that their client understands the importance of absolute candour, both to their adviser and to HMRC. Keeping information back or assuming that something isn’t relevant can lead to a flawed disclosure, which in turn could result in criminal investigation, which no client wants.

Similarly, an attitude of collaboration and co-operation is the best way to ensure the maximum reduction in penalties. However, a note of caution should be observed here that the taxpayer does not end up giving what amounts to an informal witness statement at an early stage without getting appropriate advice.

An investigation that goes back a possible 20 years can create problems when trying to retrieve documents for the early periods and where taxpayer recollection of the purpose and nature of certain transactions is less clear. Often discussions and negotiations are needed with HMRC to reach a reasonable solution on how to proceed with the absence of information and an adviser can help ensure that the taxpayer’s position isn’t jeopardised.

Some investigations can be incredibly complex with a significant number of documents and thousands of transactions to review. This can take a lot of time to work through and HMRC needs to be regularly informed of progress, or it may decide to take over the investigation.