Corporate acquisitions: the 100 day plan to deal with common tax problems

Share this article

Whilst it may be a milestone event, the completion of a corporate acquisition should trigger the consideration of a range of common tax issues.

Key Points

What is the issue?

When companies are acquired, the transaction can give rise to a wide range of additional UK tax issues, across a variety of taxes, all of which must be considered by the company and its advisers.

What does it mean for me?

There are common issues that companies which are the subject of a change of ownership should be planning to deal with.

What can I take away?

Consider a wide range of tax issues across corporation tax, VAT, employment-related securities and employment tax and, in conjunction with available due diligence reports and structure papers, form a 100 day post-completion tax plan for addressing the issues.

© Getty images/iStockphoto

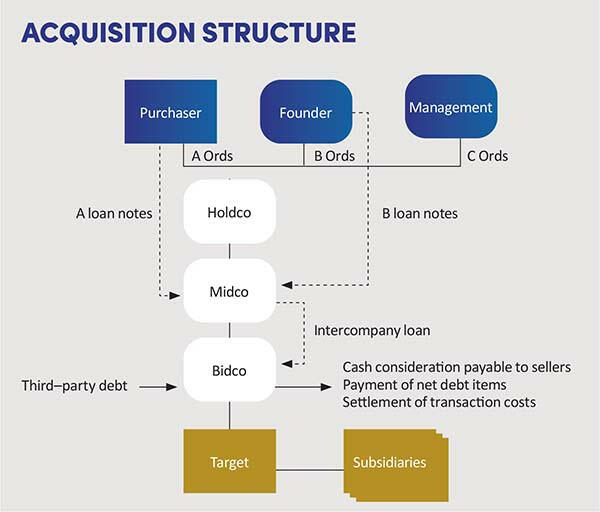

This is the first in a series of articles exploring the common UK tax issues which can arise for a company or group following the completion of an acquisition by a third-party purchaser. Specifically, we will look at these issues in the context of a leveraged buy-out using a familar acquisition structure (see Acquisition structure).

Whilst some tax issues may have been identified as part of any pre-transaction due diligence undertaken, this article will review some of the more common UK tax issues which may specifically arise post-completion. These fall into a variety of areas.

Corporation tax

The first basic job will likely be to register Holdco, Midco and Bidco for corporation tax. HMRC must be notified within three months of a company becoming active.

Transaction costs

Commonly incurred transaction costs relate to the raising of debt, project management, corporate finance, due diligence, legal work and tax advice. These costs are normally incurred by Bidco, a newly created company which will often act only as an intermediate holding company in the new structure.

Any deductible costs will therefore be either management expenses or non-trade loan relationship debits of Bidco. Group relief may be available to give relief for any losses incurred by Bidco as a result. A more detailed look at the technical position in relation to transaction costs will be the subject of a future article.

Restructuring the group

Whilst the newly created corporate structure has been designed for the current transaction, it is often the case that Target will be the ‘Holdco’ from a previous transaction. This can result in a large and unnecessary corporate chain with a number of redundant intermediate holding companies. Such a group structure could be rationalised post-completion, typically using ‘no gain, no loss’ transfers (under the Taxation of Chargeable Gains Act 1992 s 171) of subsidiaries between the members of the group. This can mean the removal of the entity in which the acquisition base cost arises; it is worth confirming that this does not matter, for example due to the availability of the substantial shareholding exemption.

Loan financing

As part of the financing of the transaction, funds will have been lent between the companies in the group, particularly by Midco to Bidco, so that it can settle the transaction consideration and costs. However, as Midco and Bidco are not normally active companies, they often require funding from other parts of the group for payments of interest or repayments on loan notes, or payment of deferred consideration.

If these funds are lent by Target or its subsidiaries and a payment is made to a participator which is not charged to income tax (such as to the seller in respect of deferred consideration), Corporation Tax Act 2010 s 459 – loans to participators – would apply to the loan balance (see ‘Disguised distributions: private equity considerations’, Tax Adviser, October 2022). These loans should be cleared within nine months of the year end to avoid the need to make payment to HMRC.

Interest deductibility

Consideration will need to be given as to how much of the interest on the acquisition and refinancing of loans is deductible for the paying company and the group as a whole.

Where the newly enlarged group is of such a size that it must operate transfer pricing, appropriate work must be undertaken to determine the appropriate arm’s length price, not just for goods and services but also for interest on the debt. The transfer pricing rules will operate to disallow the interest on the part of any loan that an independent third party would not have been willing to lend, or to the extent that the interest rate is deemed to be excessive.

The rules will also operate to impute an arm’s length interest charge where the actual rate is lower. Where the level of debt far exceeds the company’s equity, it will be considered to be thinly capitalised.

Once an arm’s length interest charge has been computed, other aspects of the tax legislation may restrict the amount of deductible interest: the anti-hybrid legislation and the unallowable purpose rules (see the recent decision in JTI Acquisition Company (2011) Ltd v HMRC [2022] UKFTT 166). Any interest payable to a participator which remains unpaid 12 months after the accounting period end is deductible only when paid. The corporate interest restriction rules potentially further restrict deductible group interest and finance costs where these exceed £2 million per year.

The complex and varied nature of interest deductibility in a transactional context will be explored in greater detail in a future article.

Loss utilisation

There are a number of anti-avoidance rules which prevent or restrict a company utilising its trading losses where there has been a change in ownership. A company may not surrender its pre-acquisition losses as group relief for five years from the date of the change in ownership.

If there is a major change in the nature or conduct of the trade in the period beginning three years before and ending five years after the change, losses arising after the change in ownership cannot be used in periods prior to the change, and vice versa. If the change is to a trade other than the one in which the losses arose – for example, the creation of an additional trade – the use of pre-change losses against these ‘affected profits’ is restricted for five years after the change in ownership.

Change in size

Following completion, if Target has joined an enlarged group, it may now fall into a different size classification for the purposes of tax relief for qualifying research and development expenditure and for the requirement to apply transfer pricing.

Where the company falls into the R&D Expenditure Credit scheme because of the acquisition, the ‘year of grace’ is ignored and the company is treated as being large in the year of acquisition. This also applies for the entire period and not just from the date of acquisition.

VAT

Substantial amounts of VAT are often incurred on the transaction costs, which are normally incurred by Bidco. In order to maximise the VAT recoverability, it is recommended that Bidco (as a minimum, and potentially Holdco and Midco) is registered for VAT with effect from the date of completion and may either form, or be included within, a VAT group with Target any any of its subsidiaries.

Advisor engagement letters should be addressed to Bidco and, where this is not the case, should be novated to Bidco at the earliest opportunity. Simply holding shares to receive dividends or for future disposal is not an activity for VAT purposes, so would not create a right to VAT recovery. Effective from completion, Bidco should therefore provide management services to Target under a Management Services Agreement, regardless of whether or not it forms part of a VAT group. It is important that Bidco has sufficient substance to do so, such as having directors with sufficient knowledge and expertise to provide these services, and that the services being provided are clearly evidenced. The management fee being charged should not be contingent; for example, by being based on the future profitability of Target. The receipt of dividends by Bidco does not affect the recoverability of the input VAT.

Employment-related securities

All shares and securities acquired by employees or directors, including prospective employees, of the group will be deemed to be employment-related securities. In a transactional context, a number of shares or securities will normally have been acquired.

Management sellers may have ‘rolled over’ some of their sales proceeds into new shares in the acquisition vehicle. This is normally structured as the issue by Bidco of loan notes to the relevant sellers, which are then exchanged for loan notes in Midco and those, to the extent agreed, exchanged for equity in Holdco. New management may also have been offered the opportunity to subscribe for sweet equity in Holdco directly.

As each of these loan notes and shares will have been issued or made available by a company connected with the person’s employer, they will be deemed to be employment-related securities. It is likely that these shares will also be restricted securities, as there is likely to be a ‘lock in’ period for the shareholders.

On the basis that the unrestricted market value (i.e. the market value ignoring any restriction for UK tax purposes) of each new share or security acquired in exchange for their original shares held in Target is no more than the unrestricted market value of the original shares, it should not be a disposal for employment tax purposes by virtue of Income Tax (Earnings and Pensions) Act (ITEPA) 2003 s 430A and there should therefore be no PAYE/NIC issues.

Elections under ITEPA 2003 s 431 cannot be made when s 430A applies, but it is generally recommended that each rolling shareholder makes a protective election in respect of all securities acquired as part of the process in case of any issue with the application of s 430A.

Where new management subscribe for sweet equity (either at completion or subsequently) and the unrestricted market value exceeds the price paid, protective elections under ITEPA 2003 s 425 or s 431 should be considered to reduce the potential total tax charge in relation to the shares.

Elections under ITEPA 2003 s 425 or s 431 must be signed within 14 days of the shares being acquired, and do not need to be sent to HMRC. If sweet equity issued to management does not fall within the safe harbour provisions of the Memorandum of Understanding agreed between HMRC and the British Private Equity and Venture Capital Association (BVCA), then a valuation may be required to support the price paid by management not being less than the unrestricted market value.

The acquisition of all shares and securities (including those issued as part of the rollover process) are reportable events and the employing entity must file an annual share plan report (formerly known as Form 42) by 6 July following the tax year of acquisition.

Employment tax

Post-acquisition work in respect of employment tax generally comprises remedying any issues which have been identified in the due diligence work. There may be completion bonuses to be paid to employees or directors and these will need to be reported to HMRC on or before the date of payment, with PAYE and NIC withheld and paid on the normal date.

Where any of the sellers has received a disproportionate amount of consideration per share, the excess above capital gains tax market value will generally be taxable as employment income, following the decision in Grays Timber Products Ltd v HMRC (Scotland) [2010] UKSC 4. This will therefore give rise to PAYE and NIC.

Where the disposal of the shares gives rise to an earn out payment to the sellers, and that seller was or will be an officer or employee of Target (or any of its group companies) or the buyer’s group post-completion, there is a risk that all or part of the earn out may be treated as employment income. If any part of the deferred cash consideration is, in reality, remuneration arising from employment, the employing company must withhold PAYE and NIC from those payments when they are paid. Provided that the relevant director or employee is remunerated at a commercial rate post-completion, and the earn out is not linked to future employment or personal performance targets, this risk can normally be managed. The full list of indicators which HMRC use in determining whether an earn out is further sale consideration can be found in the Employment Related Securities Manual at ERSM110940.

Other issues

Finally, there are a number of other tax and non-tax considerations in the period following an acquisition. Where there has been any pre-transaction restructuring involving the transfer of shares between group companies for consideration, relief from stamp duty under Finance Act 1930 s 42 must be claimed in writing. Claims should be submitted to HMRC for adjudication within 30 days of the share transfer.

When interest is eventually to be paid on the loan notes issued by Midco, which generally last more than 12 months, consideration should be given to the withholding tax position. Interest is treated as paid when paid in cash, by book entry (assuming sufficient funds are available) and by the issue of payment-in-kind notes.

If the loan notes are listed on a recognised stock exchange, then payments can be made gross. If not, then only payments made to UK companies will be able to be paid gross. Interest must be withheld on the full payment to a partnership unless all of the partners are UK companies. Where the payment must be made net, basic rate tax of 20% must be withheld and paid over to HMRC quarterly using the CT61 regime. Forms CT61 are only available on paper and the company must apply to HMRC. This application should therefore be completed well ahead of the first interest payment date.

Summary

Transactions can give rise to myriad tax issues, depending on the identity and structure of the purchaser and the structure of the purchase itself – more than could be covered in this article. A clear plan is needed to cover all of the issues. Copies of the transaction documentation and due diligence reports are vital.