Crunch time

Share this article

Robert Salter and Yvanna Pert consider the compliance challenges that a hard Brexit may involve for employers with employees subject to international social security

Key Points

What is the issue?

The EU Social Security Coordination Regulations currently ensure that employers and employees with international duties only pay social security contributions (such as NIC in the UK) in one country at a time. However, if the UK leaves the EU without a deal (‘hard’ Brexit), the coordination rules in place between the UK and the EU may end.

What does it mean for me?

Employers need to understand the potential consequences of a no-deal Brexit and identify key compliance requirements, in order to deal effectively with any changes. This article looks at the implications of a no-deal scenario for employees and employers with international duties.

What can I take away?

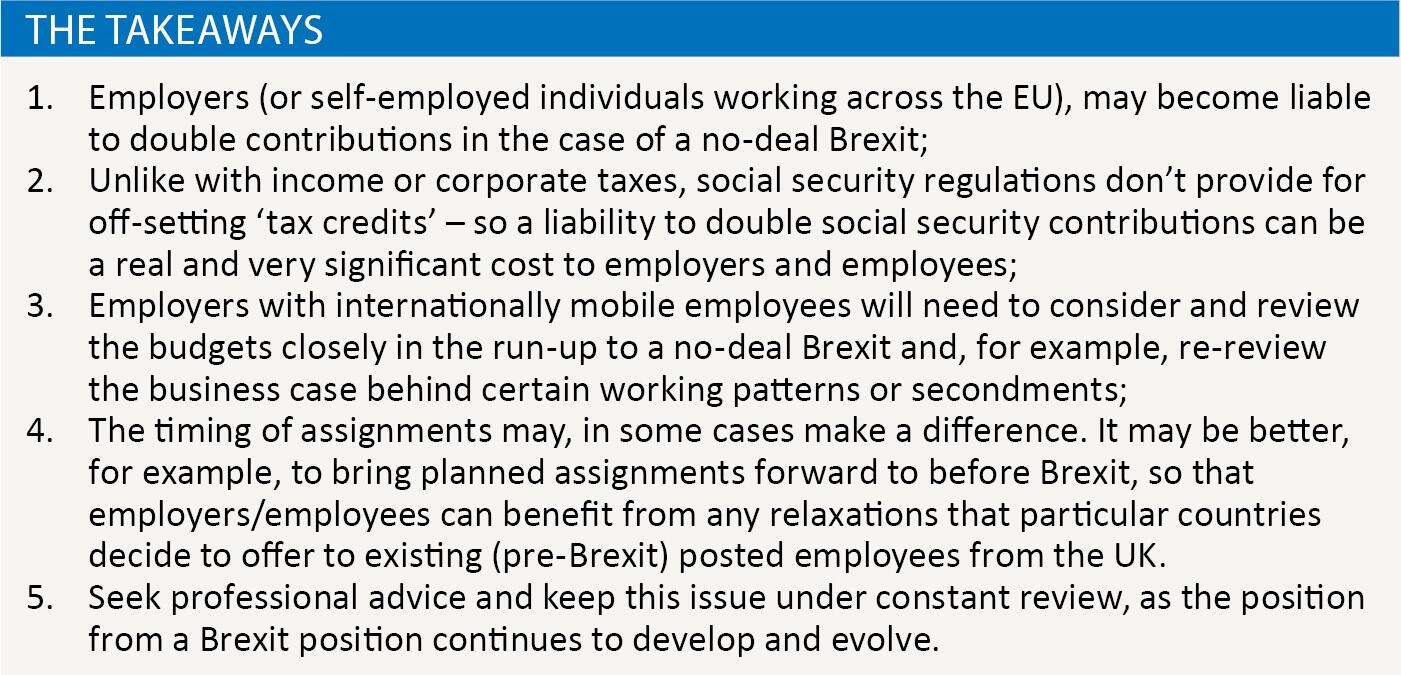

With the uncertainty around Brexit, it is important for employers to have a contingency plan in place in the event of a no-deal. Getting finance, tax and HR departments to work closely together to address the issues that arise is an important step but understanding the potential impact of such a scenario (for example a possible double social security charge) and the risk from a cost and people’s perspective, is crucial.

Social Security, the EU and Brexit

Although advisers will be aware that social security is a tax (and in many respects one of the biggest revenue streams for the UK and EU countries generally), it is often forgotten that in comparison to most ‘taxes’, it is heavily regulated by the EU, specifically when people are moving ‘internationally’ (e.g. on formal secondments or as regular business travellers), or have worked in other countries within the EU (including EEA and Switzerland), as local employees over their working lifetime. So with the possibility of a no-deal Brexit still a consideration, this article looks to highlight the implications of such a scenario for employees and employers, who are presently on or could in future have international duties.

The position today

At the present time, whilst the UK is a member of the EU, we have the following arrangements for employees (and the self-employed):

- All workers are only liable to Social Security in one EU member state.

- This is usually the state in which they work, but they can remain in their home system in some situations – e.g. if they are posted overseas for up to five years, if they obtain an A1 Certificate.

- Workers with separate jobs in more than one member state, for example, would usually pay Social Security in their ‘home location’ (subject to some conditions being met).

More information is provided in the article ‘European delights’ in the April 2018 issue of Tax Adviser. The EU-wide arrangements outlined would continue to apply in the UK for an interim period, if the UK Parliament accepts the Withdrawal Agreement that had been provisionally agreed between the EU and the UK.

The advice from HMRC

HMRC has published advice on the implications of a no-deal Brexit (e.g. in December 2018 and April 2019) and the Government has also made various regulations (e.g. SI 2019/ 722), allowing for changes to the Social Security Regulations in the case of a no-deal Brexit. Whilst there are some uncertainties in the publications from December 2018 and April 2019, one would suggest that in the case of a no-deal Brexit, you could have the following position:

- The UK continues to accept (at least for an ‘interim period’), that EU-based employees and self-employed individuals working in the UK remain subject to the EU regulations and not liable to National Insurance Contributions (NICs);

- UK-based employees working in the EU on assignment after a hard Brexit could become liable to double contributions–i.e. both UK NICs and overseas Social Security contributions;

- In some cases, other EU countries may not impose host country Social Security on secondees from the UK because:

- there is a historical Social Security Agreement between the UK and the country concerned which in effect becomes ‘re-activated’ in the case of Brexit; or

- the other jurisdiction may relax its domestic Social Security regulations for an interim period (e.g. for secondees from the UK who are already in the other jurisdiction on assignment (and covered by an A1) prior to the date of any hard Brexit). The EU has ‘recommended’ that the member states should show some flexibility in this regard, although if/when the UK becomes a 3rd country (i.e. it has left the EU or the EEA), international social security arrangements are not an area that the EU has any direct or formal involvement and oversight over.

Social Security Totalisation Agreements

Whilst the UK has a reasonably extensive network of Totalisation Agreements, we would suggest that for mobile EU employees, these do not, from an overall perspective, represent a ‘fair replacement’ for the existing coverage provided by the EU Social Security regulations. Employers and advisors in particular need to note the following challenges:

- The UK does not presently hold Totalisation Agreements with a number of EU member states (e.g. Poland, Romania, Czech Republic);

- The agreements that the UK has with EU member states are typically ‘out-of-date’ – i.e. they often are from the 1950s or 1960s, and may provide:

- For coverage for only the shortest assignments (e.g. the French/UK agreement only covers assignments of up to 6 months); and

- They don’t typically address modern working patterns and issues such as cross-border employees, home office tele-workers based for part of their time in other jurisdictions, short-term business travellers or international, non-executive directors who are non-resident in the country where they are a director.

Though it is possible (indeed hopefully probable) that some of these issues will be addressed as we progress, realistically this will be quite a long-term process. For example, it may not be politically possible to update the French/UK Totalisation Agreement at the present time, so that it covers longer-term assignments (and does the French Government even wish to update the Treaty?), or to agree new agreements with countries with whom we presently have no agreement.

Ireland and Switzerland

On a more positive note, the Government has, however, been able to reach new agreements with both Ireland and Switzerland from a Social Security perspective. Both of these new agreements only come into effect in the case of Brexit.

The Irish agreement is a ‘full agreement’ and, in very simple terms, is designed to mirror the existing EU Social Security regulations. As such, it would, for example, cover both existing and future assignments between the UK and Ireland and also covers home workers, business travellers and the other issues associated with the modern working world.

The agreement with Switzerland is, in contrast, much more restrictive. Whilst it ensures that the EU Regulations will continue between the UK and Switzerland, this coverage only applies for individuals who are working internationally between these two jurisdictions prior to Brexit. Any international employees seconded to Switzerland after Brexit, for example, would only be covered by the terms of the historical Swiss/UK Totalisation Agreement with the pitfalls that this could bring in certain situations. As such, it may, for example, in some cases be beneficial to bring forward a planned secondment to Switzerland from the UK, so that it commences before 31 October (the present Brexit date).

The options for employers/employees

So, is it possible for employers/employees to avoid double social security contributions arising in the case of a hard Brexit? The answer is ‘it depends’.

For example, in some cases, companies may choose to send people to other EU countries as local transferees (i.e. so that they give up the home country employment contract and accept a local employment contract for the period overseas). This would usually ensure that both the employee and the employer are only liable to social security in the one location on their regular salary and allowances. However, this is not just a question of tax planning. Employers will also need to consider a wide range of other factors including:

- HR and employment rights;

- Pension entitlement;

- The family position of the employee; and

- Employee preferences (in many countries – e.g. France, Italy), employees are very attached to their social security rights and entitlements and would not necessarily be willing to give these up willingly.

From a more strategic perspective, employers may also need to review the over-arching structure of their business – specifically with regard to where international, pan-European roles are based, but also with regard to their HR philospohy and approach.

For example, if individuals going on international transfer and having their employment contract transferred to the host entity to avoid the risk of double contributions arising because of a no-deal Brexit lose home country social security rights, how should employers address these concerns? Is it simply a question of offering more money – e.g. extra allowances as ‘compensation’ (and would the budget allow this)? Or does the home country scheme provide for voluntary contributions as an alternative? And how do the voluntary costs and benefits compare to the core, regular state rights? Or might it be appropriate to try and provide additional ‘private insurance provision’ in some cases? As there is not likely to be any ‘one size fits all’ solution in this regard, companies will need to ensure that they pro-actively address the issues and communicate effectively and clearly with their employees, if they want them to work internationally and fulfill the roles that are required in this regard.

Conclusion

Though much remains uncertain about Brexit and the impact that this will have on the EU (and wider European economy), any no-deal Brexit will have significant consequences on those companies with internationally, mobile employees who ‘touch’ the UK in some way. This is particularly the case, for those employees who are legally employed in the UK and active in other countries.

The changes will require finance, tax and HR departments to work closely together and address the issues that arise pro-actively. Given the uncertainties with Brexit and the exact ‘nature’ of how this will look and develop, some companies may want to adopt a ‘wait and see’ approach before making any lasting decisions. However, the complex nature of the issue and the potentially far-reaching impact that this area could have on both costs and people (in many cases the absolute critical factor for a company’s ongoing success), mean that companies should be developing their ideas and proposals in this area now rather than simply hoping for the best.